Illustration showing how life insurance premiums rise from age 30 to 45.

When to Buy Life Insurance?

Content

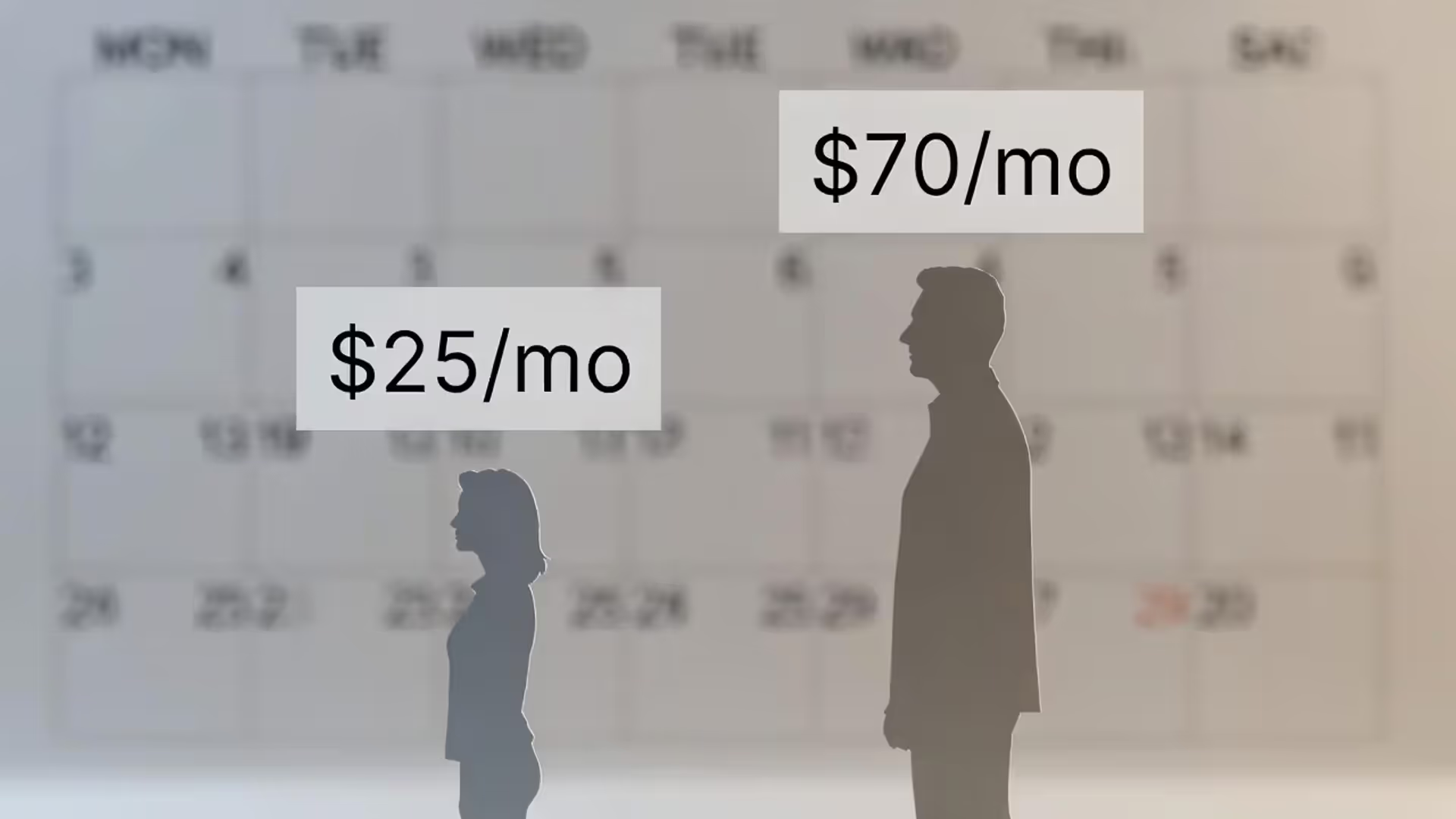

The question of when to purchase life insurance doesn't have a one-size-fits-all answer, but the financial consequences of your timing decision can follow you for decades. A 30-year-old who buys a $500,000 policy might pay $25 monthly, while a 45-year-old purchasing identical coverage could face $70 monthly premiums—a difference of over $10,000 across a 20-year term.

Most Americans delay this purchase until a major life disruption forces their hand, often after their premiums have already doubled or tripled. Understanding the relationship between timing, cost, and coverage options helps you make a decision that protects your family without overpaying or leaving gaps in protection.

How Age Affects Your Life Insurance Costs and Options

Insurance companies calculate your premiums based on statistical mortality risk, and that risk increases predictably with each passing year. The financial impact of waiting even five years can be substantial enough to affect your household budget for the entire policy term.

Premium differences by decade (20s through 60s)

Your twenties represent the absolute lowest premiums you'll ever qualify for, assuming you're in good health. A healthy 25-year-old non-smoker typically pays between $15 and $25 monthly for a $500,000 20-year term policy. That same person at 35 might pay $20 to $35 monthly, while waiting until 45 pushes costs to $60-$90 monthly.

The steepest premium increases occur after age 50. A 55-year-old purchasing that same $500,000 policy often faces $150-$250 monthly premiums—ten times what they would have paid at 25. By age 60, many term policies become prohibitively expensive for average households, with premiums frequently exceeding $300 monthly.

Here's what you can expect to pay across different ages:

| Age | 10-Year Term (Male) | 10-Year Term (Female) | 20-Year Term (Male) | 20-Year Term (Female) |

| 25 | $12-$18/month | $11-$15/month | $18-$25/month | $15-$22/month |

| 35 | $15-$22/month | $13-$19/month | $25-$35/month | $22-$30/month |

| 45 | $32-$48/month | $27-$40/month | $65-$90/month | $55-$75/month |

| 55 | $85-$125/month | $65-$95/month | $180-$250/month | $140-$190/month |

Rates shown for healthy, non-smoking applicants purchasing $500,000 in coverage. Actual premiums vary by insurer, health status, and state.

Health underwriting considerations at different ages

Author: Christopher Baldwin;

Source: everymuslim.net

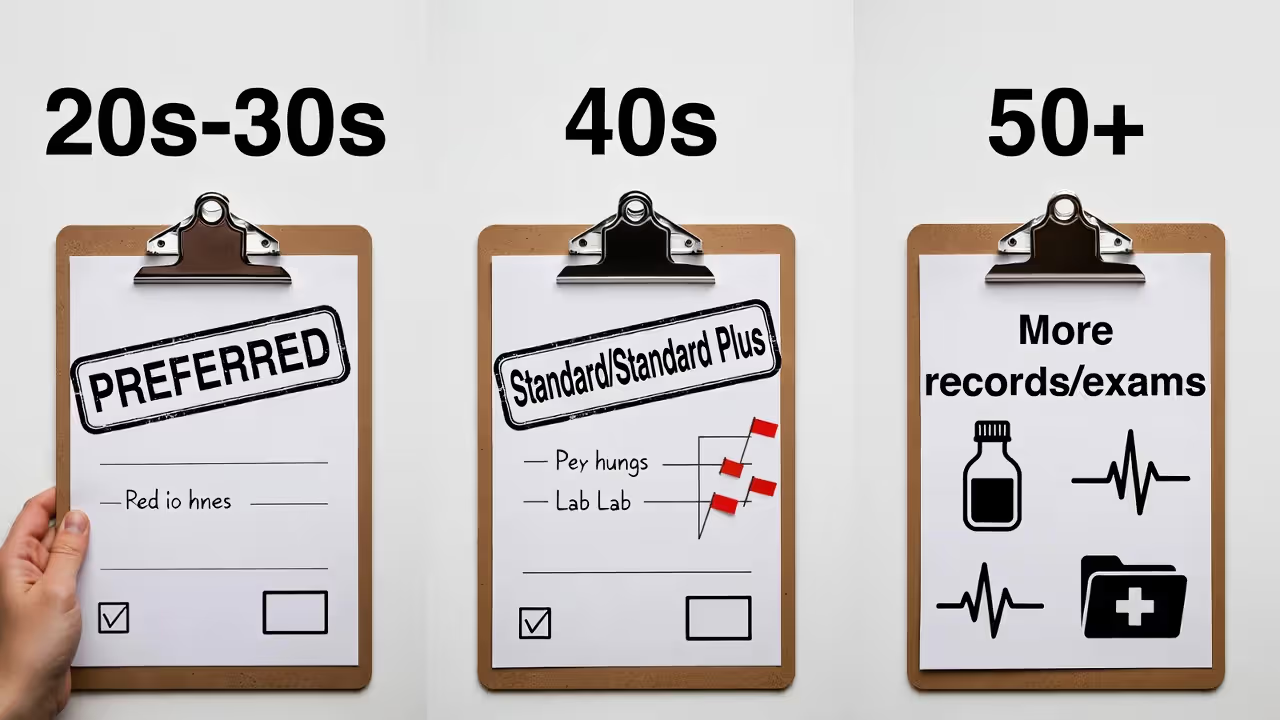

Insurance companies don't just care about your age—they examine your complete health profile, and that profile typically deteriorates as you get older. In your twenties and early thirties, most applicants sail through underwriting with "Preferred Plus" or "Preferred" ratings, securing the lowest available premiums.

By your forties, minor health issues start appearing. Slightly elevated cholesterol, borderline blood pressure, or a few extra pounds can bump you into "Standard Plus" or "Standard" rating classes, increasing premiums by 25-50% compared to preferred rates. These aren't disqualifying conditions, but they cost you money.

After 50, the underwriting process becomes significantly more rigorous. Insurers often require stress tests, comprehensive blood panels, and detailed medical records. Common age-related conditions—prediabetes, treated hypertension, or a history of minor cardiac issues—can result in table ratings that double or triple standard premiums. Some applicants face declination altogether.

The age considerations insurance companies use aren't arbitrary. Actuarial tables show that a 55-year-old with controlled high blood pressure has measurably higher mortality risk than a healthy 35-year-old, and premiums reflect that mathematical reality.

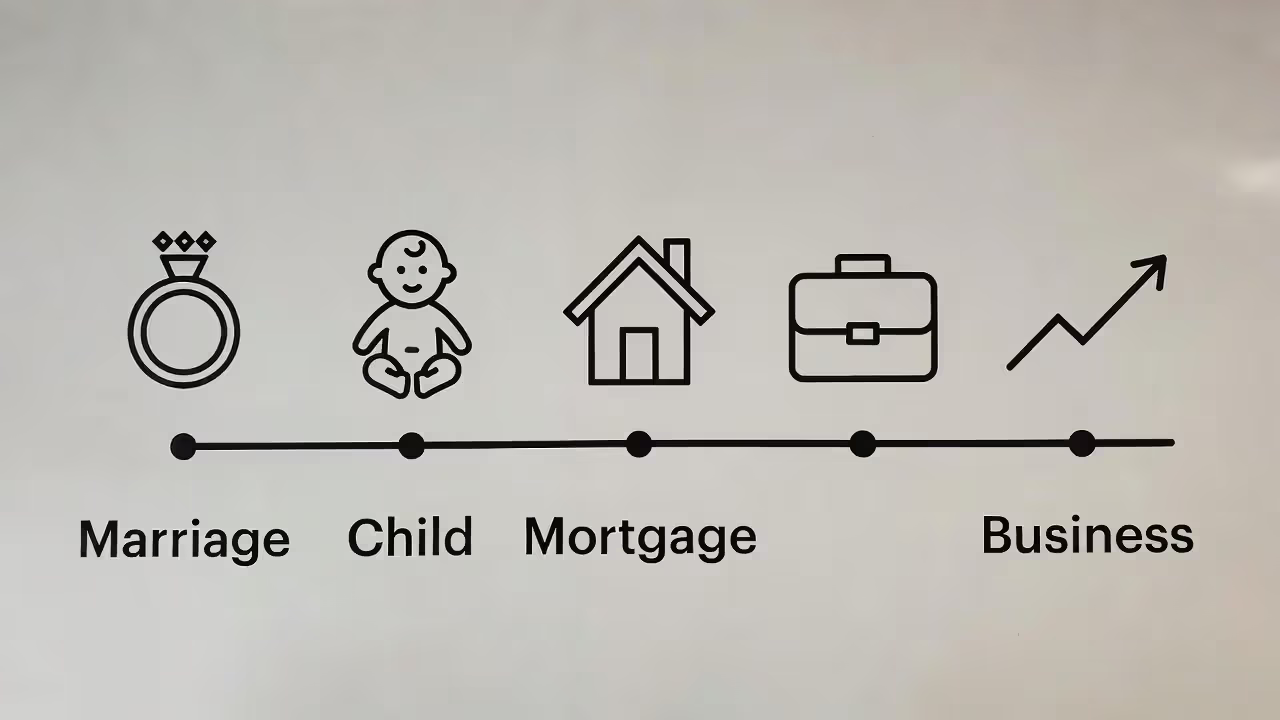

Life Events That Signal It's Time to Buy Coverage

Author: Christopher Baldwin;

Source: everymuslim.net

Certain life transitions create financial dependencies that didn't exist before. These moments represent clear signals that you need coverage, regardless of your age.

Marriage and partnership

When you legally bind your financial life to another person, you create mutual dependency. If you die unexpectedly, your spouse faces immediate financial consequences: funeral costs averaging $7,000-$12,000, potential loss of your income, and possibly the inability to maintain your shared standard of living.

Even dual-income couples without children need coverage. If one partner earns significantly more, the lower-earning spouse may struggle to cover the mortgage, car payments, and other fixed expenses alone. Life events insurance planning should begin as soon as you're engaged or have made a long-term commitment.

One practical approach: each partner should carry enough coverage to pay off shared debts and replace 5-10 years of their income contribution. This gives the surviving spouse time to adjust financially without immediate crisis.

Becoming a parent or expanding your family

Children create the most obvious need for life insurance. You're now responsible for 18+ years of expenses: housing, food, education, healthcare, and countless other costs. If you die, someone must still provide those resources.

Calculate the total cost of raising your child to independence—often $250,000 or more per child—then add funds for college education. Many parents purchase $500,000 to $1 million in coverage when their first child is born, ensuring their family maintains financial stability even in worst-case scenarios.

Adoptive parents and stepparents face identical considerations. The legal and financial responsibility is the same, and coverage planning stages should align with when you officially assume parental duties.

Buying a home or taking on major debt

A mortgage represents the largest debt most Americans ever carry. If you die with $350,000 remaining on your home loan, your family faces an impossible choice: continue making payments they may not afford, or sell the home during an emotionally devastating time.

Life insurance can cover your entire mortgage balance, ensuring your family keeps the home regardless of what happens to you. The same logic applies to business loans, co-signed student debt, or any other obligation that would burden your family after your death.

Consider purchasing coverage equal to your total debt load plus 3-5 years of income replacement. This combination pays off obligations and provides breathing room for your dependents to stabilize.

Starting a business or career advancement

Business owners face unique timing considerations. If you've taken loans to fund your startup, those debts don't disappear when you die. If you have business partners, they need funds to buy out your ownership stake from your estate. If your business depends on your personal expertise, your family needs resources to wind down operations without financial catastrophe.

Key person insurance protects businesses from the financial shock of losing essential personnel. Buy-sell agreements funded by life insurance ensure smooth ownership transitions. Both strategies require purchasing coverage before health issues make it expensive or impossible.

Career advancement that significantly increases your income also signals it's time to review coverage. If your family has adjusted to a $150,000 annual lifestyle, they can't easily downshift to $50,000 if you die. Your coverage should scale with your income and your family's dependency on that income.

Why Buying Life Insurance Early Pays Off

Author: Christopher Baldwin;

Source: everymuslim.net

The financial advantages of early purchase extend far beyond simple premium savings, though those savings alone can be substantial.

Locking in lower premiums

Term life insurance premiums remain fixed for the entire policy duration. If you buy a 20-year term policy at age 30, you pay the same monthly amount until age 50—even though your mortality risk increases every year during that period.

This creates significant early purchase benefits. The 30-year-old paying $30 monthly will spend $7,200 total over 20 years. If they wait until 40 to buy the same coverage, they might pay $55 monthly—$13,200 over the remaining term. That $6,000 difference could fund a year of college expenses or contribute substantially to retirement savings.

The best time to buy coverage is when premiums are lowest relative to the protection period you need. For most people, that means purchasing in your twenties or early thirties, even if your immediate financial dependents are limited.

Securing coverage before health issues arise

You cannot predict when health problems will emerge, but you can guarantee they'll make insurance more expensive or unavailable. A cancer diagnosis, heart attack, or diabetes development can instantly render you uninsurable at standard rates—or uninsurable at any price.

Buying coverage while you're healthy ensures you're protected regardless of what your medical future holds. If you develop a serious condition five years into a 20-year term policy, your coverage continues at the original premium. Had you waited, that same condition might have resulted in declination or premiums three times higher.

This represents a form of health arbitrage. You're essentially betting that your health will worsen over time (a safe bet for everyone), and you're locking in prices based on your current good health before that inevitable decline occurs.

Building cash value sooner (for permanent policies)

Permanent life insurance—whole life or universal life—includes a cash value component that grows over time. The earlier you start, the more time your cash value has to compound.

A 25-year-old purchasing a $250,000 whole life policy might pay $200 monthly, with a portion building cash value that could reach $100,000 or more by retirement. Starting the same policy at 40 means higher premiums and 15 fewer years of cash value growth, significantly reducing the policy's investment component.

Permanent insurance costs substantially more than term coverage, and it's not appropriate for everyone. But if permanent coverage fits your financial strategy, starting early maximizes the cash value benefit while minimizing the premium burden.

Common Mistakes People Make When Timing Their Life Insurance Purchase

Author: Christopher Baldwin;

Source: everymuslim.net

Even people who understand they need coverage often sabotage themselves through poor timing decisions.

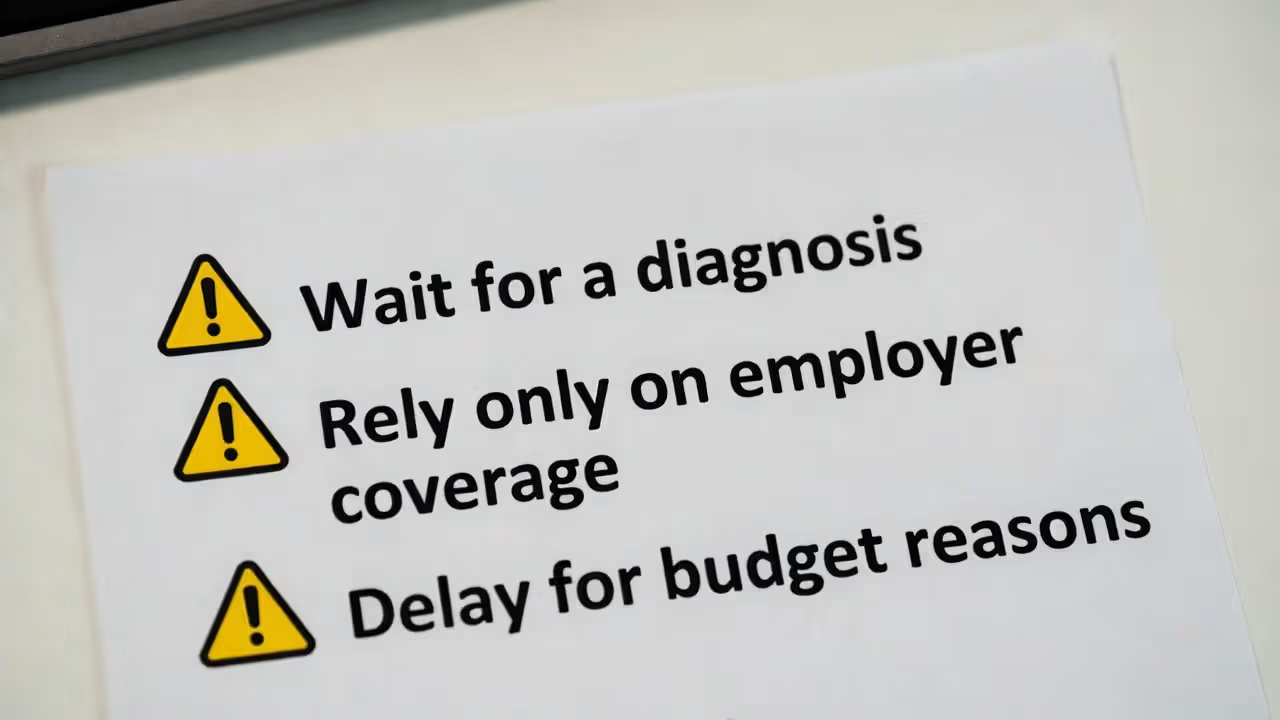

Waiting until health problems develop: The single most expensive mistake is delaying until after a diagnosis. A 45-year-old who buys coverage before discovering they have diabetes might pay $80 monthly. The same person applying after diagnosis could face $150-$200 monthly premiums or be declined entirely. You cannot time the market on your own health.

Assuming employer coverage is sufficient: Many employers provide group life insurance equal to one or two times your annual salary. If you earn $75,000, that's $75,000-$150,000 in coverage—likely inadequate for a family with children, mortgage, and long-term expenses. Employer coverage also disappears if you change jobs or are laid off, often at precisely the wrong moment. Relying exclusively on workplace policies leaves dangerous gaps in your timing strategy insurance approach.

Delaying because of budget concerns: Young professionals often postpone coverage because they're managing student loans, building emergency funds, or simply living paycheck to paycheck. The irony is that delaying makes coverage more expensive later, when budgets are often even tighter due to mortgages, childcare, and other family expenses. A $20 monthly policy purchased at 28 is more affordable than a $60 policy purchased at 42, even if your income has doubled.

Buying too early without assessing actual needs: Some people purchase large permanent policies in their early twenties when term coverage would be more appropriate and affordable. Others buy minimal coverage that becomes inadequate within a few years. Coverage planning stages should align with your actual financial situation, not theoretical future needs or aggressive sales pitches.

The right approach: buy adequate term coverage as soon as you have any financial dependents or debts, then review and adjust as your life circumstances change.

How to Determine Your Personal Best Time to Buy

Author: Christopher Baldwin;

Source: everymuslim.net

Generic timing advice only goes so far. Your optimal purchase timing depends on your specific circumstances, financial obligations, and dependents.

Assessing your financial dependents

List everyone who depends on your income: spouse, children, aging parents you support, disabled siblings, anyone else relying on your financial contribution. For each dependent, estimate how long they'll need support and what annual amount would maintain their standard of living.

A stay-at-home spouse with three young children might need income replacement for 20+ years. An employed spouse with one teenager might need just 5-10 years of support. Aging parents you're helping might need assistance for an uncertain duration.

This assessment reveals your coverage timeline. If your youngest child is two, you need coverage lasting at least 16 years (until they're 18), and preferably 20-25 years (through college). That suggests a 20 or 30-year term policy purchased now.

Calculating your coverage needs by life stage

A rough formula: multiply your annual income by 10-15, then add your total debts. A person earning $80,000 with a $250,000 mortgage and $30,000 in other debts needs roughly $1-1.5 million in coverage.

This formula adjusts by life stage: - Single, no dependents: 5-10x income (enough to cover debts and final expenses) - Married, no children: 10x income plus shared debts - Young children: 15-20x income plus all debts and education costs - Teenagers/college-age children: 10-15x income plus remaining debt and education costs - Empty nesters: Reduce to debt coverage plus 3-5x income - Retirement: Many people drop term coverage entirely or maintain small permanent policies for estate planning

Your best time to buy coverage is when you first enter a new life stage with increased financial dependents, not after you've been in that stage for years.

The best time to buy life insurance was ten years ago. The second-best time is today. I've never had a client tell me they regretted buying coverage too early, but I've had many who deeply regretted waiting too long—especially after a health diagnosis made coverage unaffordable or unavailable.

— Jennifer Martinez

Evaluating your current health status

Be honest about your health trajectory. If you're currently healthy but have a family history of early heart disease, diabetes, or cancer, buying coverage now—before you potentially develop these conditions—is critical.

If you're overweight, have borderline blood pressure, or other controllable risk factors, you face a choice: buy coverage now at slightly elevated rates, or spend 6-12 months improving your health metrics and then apply for better rates. For minor issues, the improvement strategy can save money. For more serious concerns, locking in coverage immediately is usually wiser.

Anyone with existing health conditions should buy whatever coverage they can qualify for immediately. Your health is more likely to worsen than improve, and waiting typically results in higher costs or declination.

Frequently Asked Questions About Life Insurance Timing

Timing your life insurance purchase strategically can save you thousands of dollars while ensuring your family has protection when they need it most. The data clearly shows that earlier purchases result in lower lifetime costs, and waiting for the "perfect" moment often means missing the window of optimal affordability.

Your personal best time to buy depends on your specific financial dependents, health status, and life stage—but for most people, that time is now or in the very near future. Evaluate your current situation honestly, calculate your coverage needs, and secure protection while you're healthy and premiums are manageable. The peace of mind that comes from knowing your family is protected is worth far more than the monthly premium, and that premium only increases the longer you wait.