Life Insurance Application Process

Life Insurance Application Process Guide

Content

Getting life insurance isn't like buying auto coverage online in ten minutes. You're looking at medical questionnaires, nurse visits to your house, blood tests, background checks, and a whole lot of waiting. The insurance company wants to know exactly how risky you are to insure—and they'll dig deep to find out. If you walk into this unprepared, you'll face delays, higher premiums, or outright rejection.

Here's what surprises most people: insurers don't just take your word for it. Tell them you're healthy? They'll order your prescription records. Say you don't smoke? They'll test your blood for nicotine. Forgot to mention that speeding ticket from two years ago? It's sitting right there in your motor vehicle report. The companies cross-check everything you tell them against multiple databases. Coming prepared makes all the difference between smooth sailing and a months-long headache.

What Happens During a Life Insurance Application?

Think of applying for life insurance as moving through five checkpoints. You start by filling out an application—maybe on a website, maybe over the phone with an agent, maybe sitting across from someone at their office. You'll answer questions about your medical history, how much you make, what you do for work, whether you skydive on weekends, and who gets the money when you die. The company looks at these answers and decides if you're worth their time and which review process you'll go through.

Next up, the background investigation starts rolling. The insurer contacts the Medical Information Bureau—a shared database where insurance companies report findings from past applications. They pull your prescription drug history to see what medications you've taken over the past several years. Your driving record gets reviewed for DUIs, accidents, and speeding violations. Depending on your state and the policy size, they might even check your credit report. All of this happens behind the scenes while you're waiting to hear back.

Then comes the medical evaluation. For most traditional policies, a paramedical examiner schedules a visit to your home or workplace. They show up with needles, sample cups, a blood pressure cuff, and a tape measure. You'll give blood and urine samples, step on a scale, answer more health questions, and get your vitals recorded. Some newer policies skip this entirely using what's called accelerated underwriting—they just analyze your prescription data and other records using algorithms.

After that, a human underwriter reviews everything. This person's job is to determine how likely you are to die in the next 10, 20, or 30 years. They examine your lab work, read through any medical records your doctors sent over, study your family health history, and evaluate your occupation and hobbies. Based on this analysis, they slot you into a risk category that determines your premium. Are you "preferred plus" material? Standard risk? High risk requiring extra charges?

Finally, you get their verdict. Maybe you're approved at the rate you expected. Maybe they counteroffer with a higher premium because your cholesterol came back elevated. Maybe they want additional records from that cardiologist you saw five years ago. Or maybe—worst case—they deny you coverage altogether. If approved, you'll sign paperwork, pay your first premium, and your coverage kicks in.

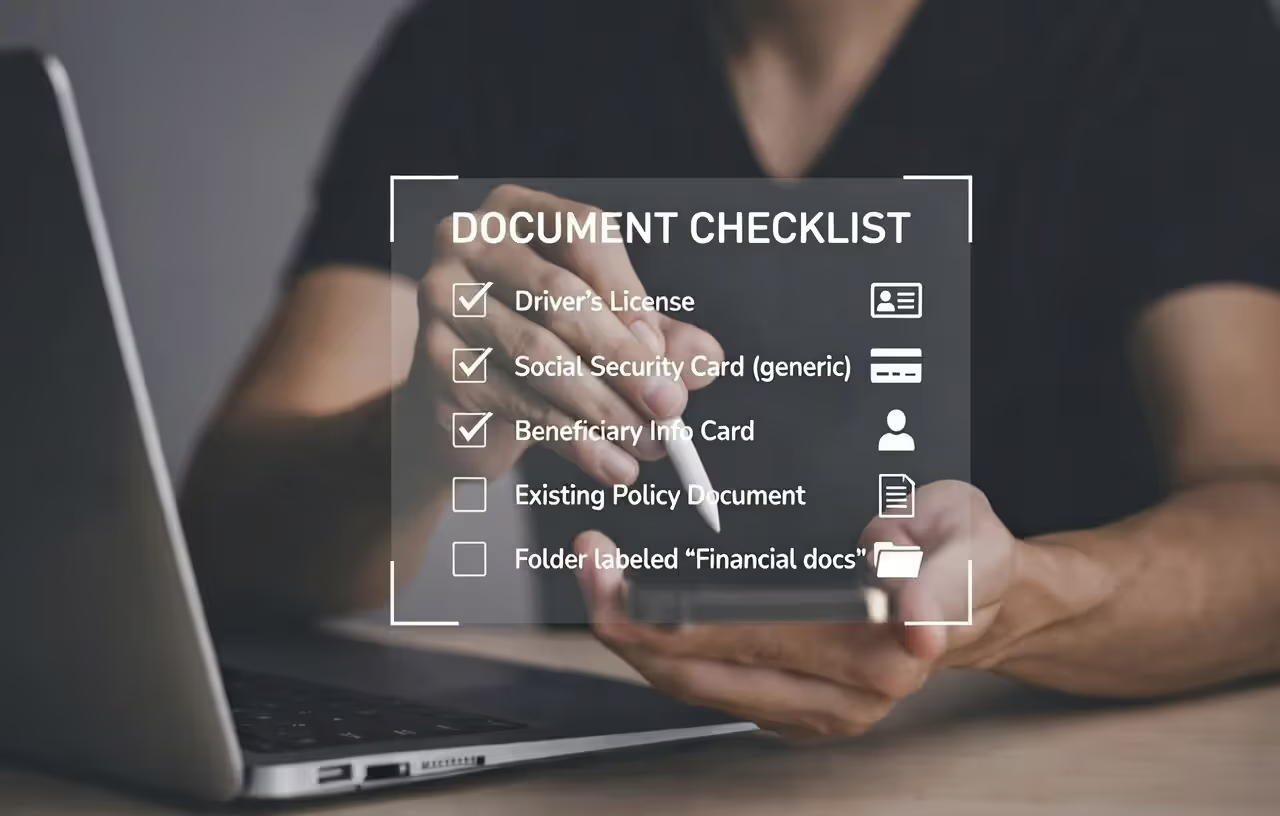

Documents You'll Need Before You Apply

Author: Christopher Baldwin;

Source: everymuslim.net

Round up your identification first—driver's license, passport, or state ID. You'll need your Social Security number for the background checks. Write down complete details for everyone you want as a beneficiary: their full legal names, birth dates, Social Security numbers, addresses, and phone numbers. If you're naming a trust or charity, get that documentation ready too.

Already have life insurance you're replacing? Bring those policy documents. Companies scrutinize replacement situations carefully because some unethical agents push unnecessary policy changes just to pocket a commission. The new insurer needs to verify that switching policies actually benefits you, not just your agent's wallet.

Medical History Documentation

You won't submit medical records with your application, but knowing where to get them saves weeks later. Make a list: your primary care doctor's office name and contact info, any specialists you've seen in the past decade, hospitals where you've stayed, and approximate dates. When the underwriter requests records, your doctor's office can take anywhere from three days to three weeks to respond. Having this information organized lets you follow up if things stall.

Write down every medication you currently take—prescription name, dosage, frequency, and which doctor prescribed it. Don't skip the over-the-counter stuff you take daily either. The insurer's prescription database will show nearly everything anyway, so leaving items off your list just makes you look dishonest or forgetful. Neither impression helps you.

Create a timeline of your surgical history, hospital stays, and emergency room visits over the past ten years. Include dates (even if approximate), what happened, and how it resolved. An underwriter pays extra attention to anything heart-related, cancer diagnoses, mental health crises requiring hospitalization, or chronic diseases like diabetes and autoimmune conditions. The more detail you provide upfront, the fewer follow-up questions you'll face.

Financial Verification Materials

Want a policy with a million-dollar death benefit or higher? Expect financial scrutiny. The company needs proof that you actually need that much coverage—they're watching for fraud schemes where people over-insure themselves. Gather your last two years of tax returns, recent pay stubs, W-2 forms, or 1099s if you freelance or run a business.

Business owners face more paperwork: profit and loss statements, balance sheets, perhaps even a formal business valuation. If you're justifying a large policy based on net worth rather than income, document your assets. Investment account statements, property deeds, retirement account balances—anything that demonstrates your financial picture. The insurer isn't judging whether you're rich enough; they're confirming the death benefit amount makes sense for someone in your financial position.

How to Prepare for Your Life Insurance Application

Author: Christopher Baldwin;

Source: everymuslim.net

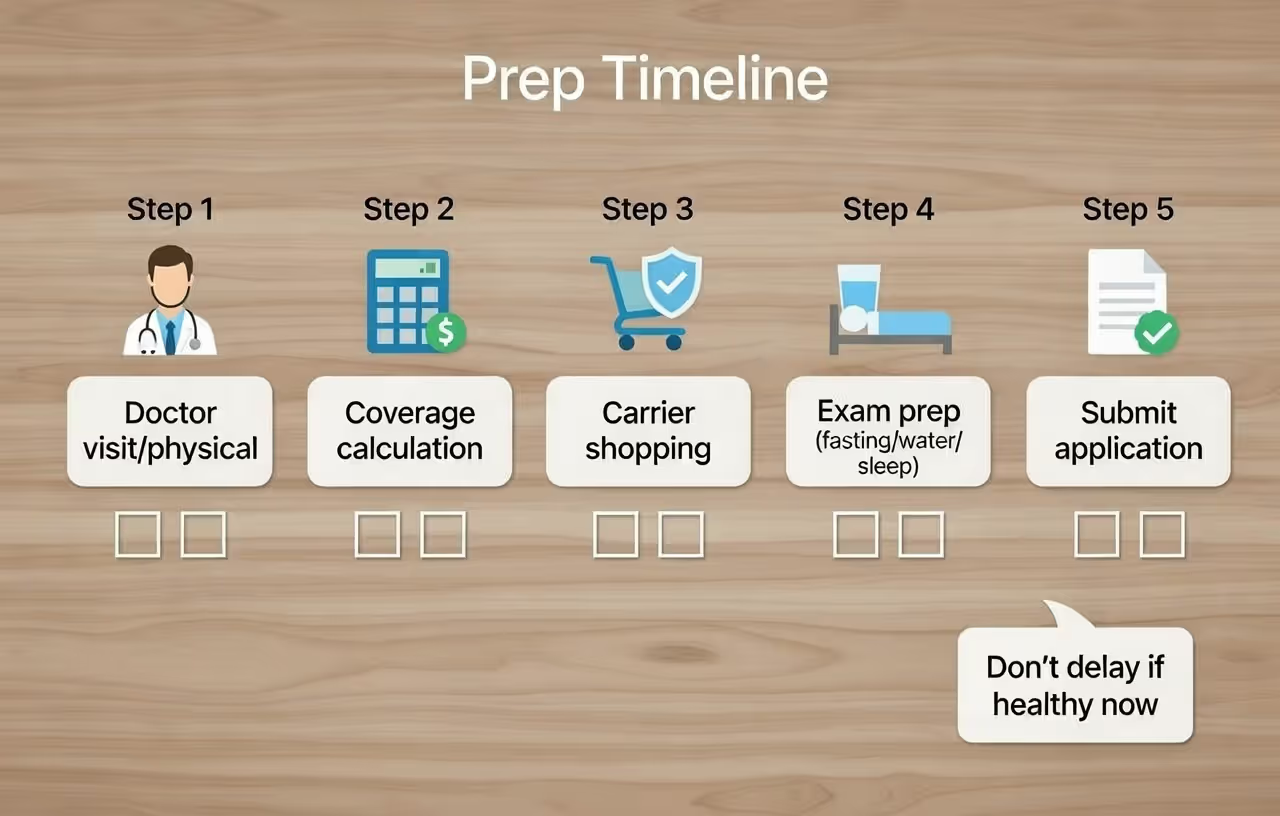

Start with a brutally honest health assessment. When did you last see your doctor? If it's been over a year, schedule a physical before applying. Use that visit to address anything you can control—lose 15 pounds if you're borderline obese, get on blood pressure medication if your readings run high, stabilize that irregular thyroid with proper treatment. Underwriters look more favorably at managed conditions than ignored ones. A diabetic who monitors blood sugar and takes medication as prescribed gets better rates than someone with untreated prediabetes who's heading toward a full diagnosis.

Calculate how much coverage you actually need—not what sounds like a nice round number. Financial planners often suggest ten times your annual income, but your situation might call for more or less. Carrying a mortgage? Add that balance. Have three kids heading to college? Factor in those costs. Want to leave your spouse enough income replacement to retire comfortably? Do the math. Requesting coverage that seems unreasonably high for your income triggers extra scrutiny and paperwork. Requesting too little leaves your family vulnerable.

Timing your application matters more than you'd think. Apply while you're healthy, not after receiving troubling news from your doctor. Planning to quit smoking? Do it first, then wait twelve months before applying—you'll qualify for non-smoker rates that can save you thousands. Want to lose weight? Drop those 30 pounds and keep them off for six months before applying. However, don't delay if you're healthy right now. Health can change suddenly, and waiting for the "perfect" moment might mean missing your best opportunity.

Shop around—but do it smart. Don't just apply to six companies hoping one says yes. Different insurers specialize in different risk profiles. Company A might excel at underwriting people with diabetes. Company B might offer surprisingly good rates for applicants with past cancer diagnoses. Company C might be the go-to for folks with controlled high blood pressure. An independent agent who represents multiple carriers can match your specific health situation to the companies most likely to treat you favorably.

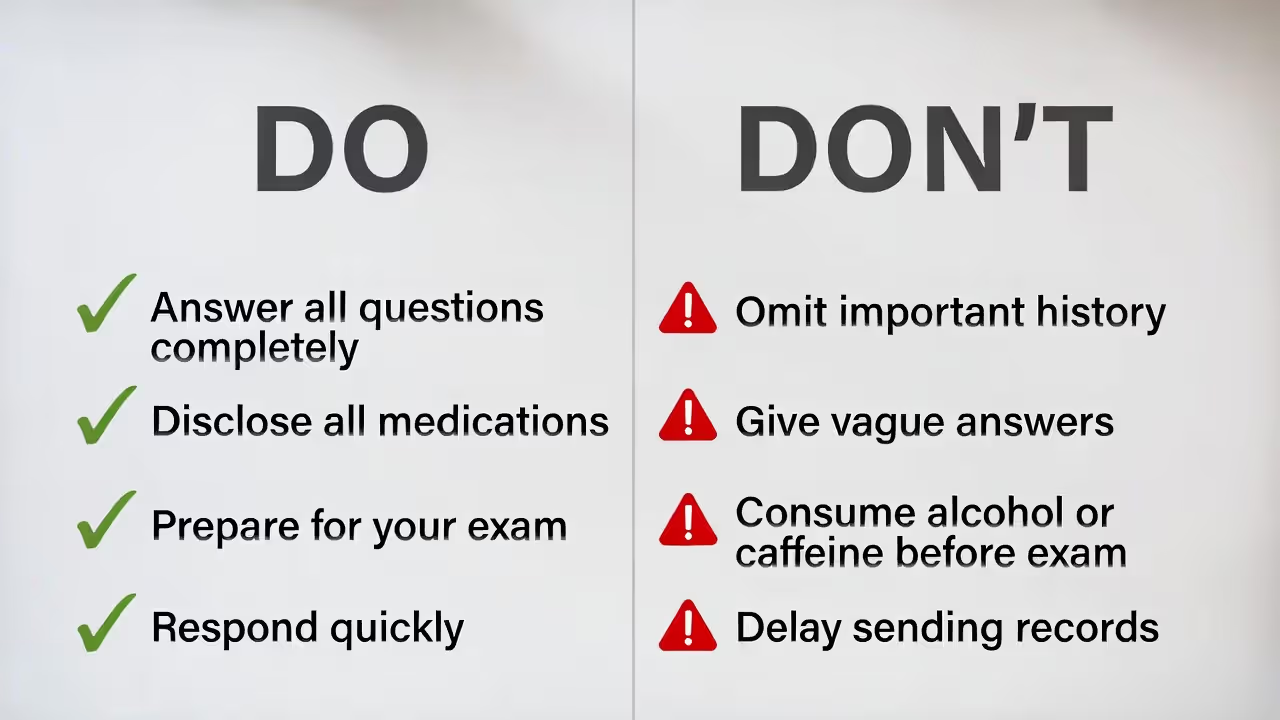

Prepare for your medical exam like you're studying for a test. Fast for ten to twelve hours beforehand so your glucose and cholesterol readings come back accurate. Skip alcohol for 24 to 48 hours before your appointment—it affects liver enzymes and blood pressure. Don't drink coffee the morning of the exam; caffeine spikes your blood pressure temporarily. Get a full night's sleep because exhaustion elevates blood pressure readings. Drink plenty of water starting the day before—it makes blood draws easier—but don't chug two liters right before, which can dilute your urine sample and require a retest.

The Underwriting Process: What Insurers Evaluate and Why

Author: Christopher Baldwin;

Source: everymuslim.net

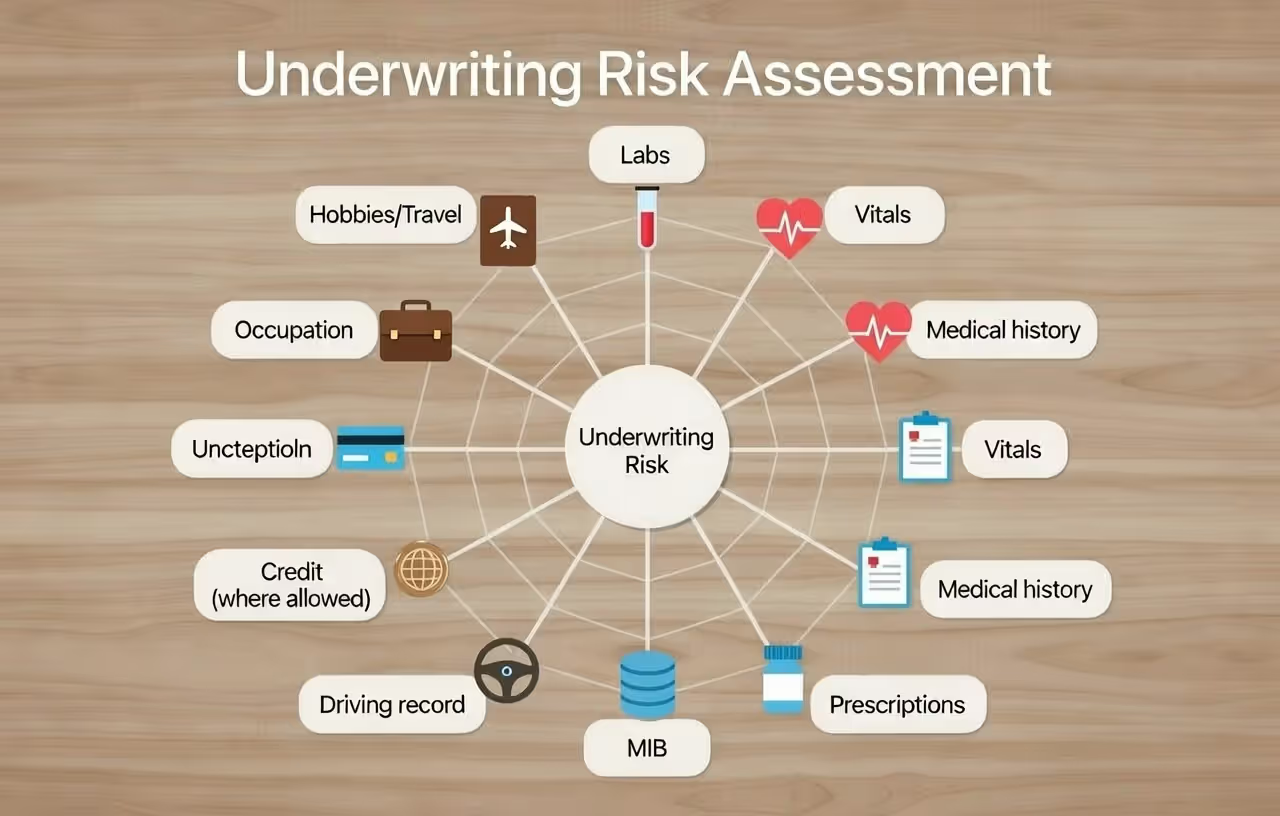

Underwriters are professional risk assessors armed with actuarial tables that predict mortality based on thousands of data points. Your medical exam results matter enormously—cholesterol levels, blood pressure readings, glucose numbers, liver enzyme counts, kidney function markers, and various disease indicators all get measured against normal ranges. Abnormal results don't automatically disqualify you, but they bump you into higher premium categories.

Prescription drug databases paint a detailed picture of your health whether you volunteer it or not. Taking multiple medications for the same condition? The underwriter wonders if your disease isn't well-controlled. Recently started or changed medications? Something new must be going on with your health. On medications for conditions you didn't mention in your application? Now you've got a credibility problem on top of whatever health issue you tried to hide.

The Medical Information Bureau functions as a shared filing cabinet for insurers. Applied for coverage five years ago? That application's key details are stored in your MIB file. If your current application contradicts information from your past applications—different medical histories, conflicting details about your health—the underwriter will notice and ask questions. You can request your MIB file once per year at no charge; doing this before applying lets you correct any errors.

Your driving record matters because how you drive correlates with how long you live. Multiple speeding tickets signal risk-taking behavior. A DUI from last year is a major red flag—not just because of drunk driving, but because statistics show people with DUIs have higher overall mortality rates. At-fault accidents, reckless driving charges, suspended licenses—all of these raise premiums or trigger denials, especially if they happened recently.

Credit checks—where state law permits—work as a proxy for responsibility and life stability. Researchers have found correlations between credit management and mortality risk, though the mechanism isn't always obvious. Recent bankruptcies, tax liens, multiple collection accounts, or severe delinquencies might affect your rates. Credit carries less weight than medical factors, but it's still part of the equation.

Your job and hobbies get evaluated too. Work as a commercial fisherman, logger, or roofer? Your occupation lands on the dangerous jobs list, potentially increasing premiums. Enjoy skydiving, rock climbing, cave diving, or BASE jumping? The underwriter wants to know how often you do these activities and what safety measures you follow. Travel frequently to countries with political instability or serious health risks? You might face coverage exclusions or extra charges.

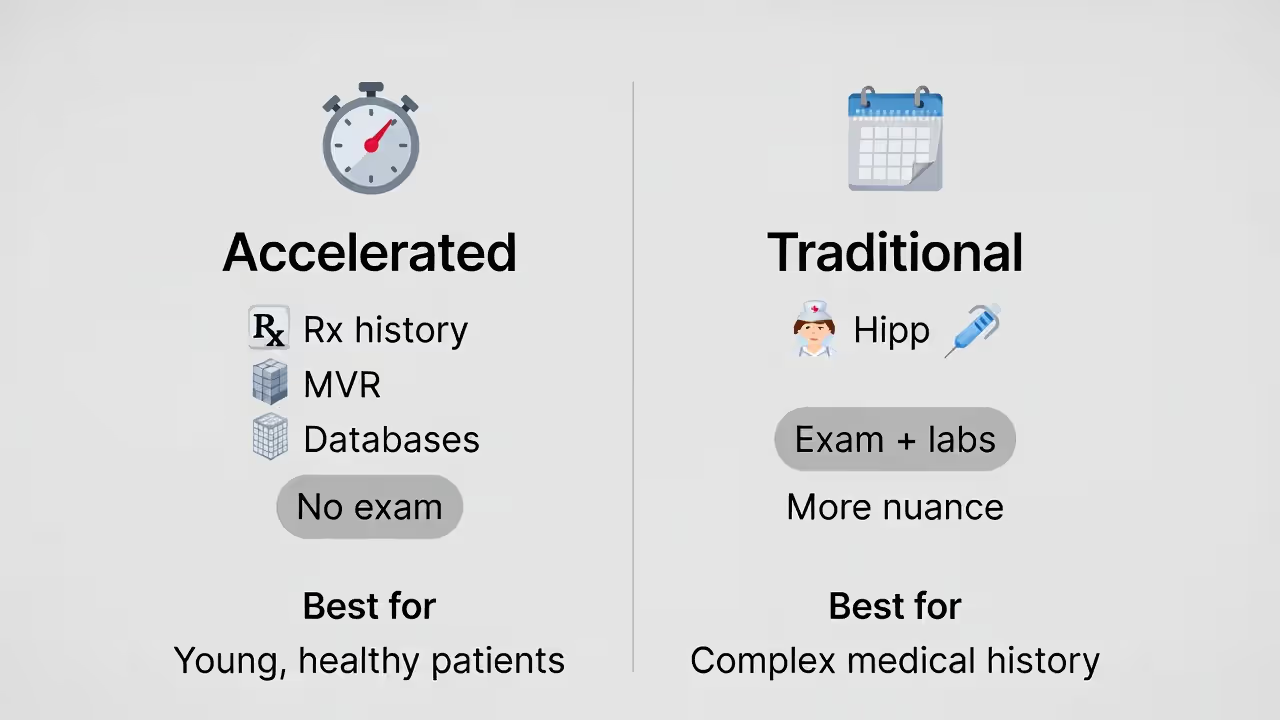

Accelerated vs. Traditional Underwriting

Author: Christopher Baldwin;

Source: everymuslim.net

Accelerated underwriting relies on algorithms that assess your risk using data instead of needles. The insurer pulls your prescription records, motor vehicle history, and sometimes consumer behavior data to build a risk profile without sending anyone to draw your blood. This approach works best for younger, healthy applicants seeking moderate coverage—usually under half a million dollars.

The upside? Speed. Many accelerated underwriting decisions arrive within one to two days. The downside? Less flexibility. If the algorithm spots anything concerning, you get routed to traditional underwriting anyway, losing the time advantage. Also, accelerated underwriting might miss recent positive health changes that would show up in a fresh medical exam—like that 40 pounds you lost over the past year.

Traditional underwriting includes the full medical workup, detailed underwriter review, and often requests for records from your doctors. The process stretches over four to eight weeks typically. But this longer timeline has advantages if your health history is complicated but well-managed. A human underwriter can evaluate context and nuance that an algorithm might miss. Your atrial fibrillation diagnosis sounds scary to a computer, but an underwriter can see it's been successfully controlled for five years with no incidents.

Risk Classification Tiers Explained

Preferred Plus (sometimes called Super Preferred) is the golden ticket. These applicants have excellent health, no family history of early death from heart disease or cancer, ideal height-to-weight ratios, perfect or near-perfect lab results, and zero dangerous hobbies. Premiums in this category run 30% to 40% below standard rates—the difference can mean thousands of dollars over a 20-year term.

Preferred classification goes to applicants with good overall health and maybe one or two minor managed issues. Your cholesterol runs slightly high but medication keeps it controlled. Your father died of a heart attack, but your own cardiac health checks out fine. You're carrying an extra 15 pounds but not enough to be clinically obese. You take medication for mild anxiety or depression. Rates here are still competitive, just not the absolute lowest.

Standard Plus sits in the middle—average health with some manageable conditions. You might be moderately overweight, have blood pressure that requires medication, or take something for acid reflux or seasonal allergies. Most Americans who apply for life insurance fall into either Standard Plus or straight Standard rating. Your health isn't perfect, but nothing's seriously wrong either.

Standard rates apply when you have more significant health concerns or several minor issues stacking up. Type 2 diabetes controlled with medication, obesity with a BMI over 35 but no related complications, controlled sleep apnea requiring a CPAP machine, or a combination of lesser issues that collectively increase mortality risk.

Substandard (also called Table Rated) classifications kick in when health problems create meaningfully elevated mortality risk. Table ratings add percentage surcharges to standard premiums—Table 2 adds 50%, Table 4 adds 100%, Table 6 adds 150%, and so on. Recent heart attacks, stroke within the past five years, cancer diagnosed less than five years ago, or poorly controlled diabetes typically land you in table-rated territory. Coverage costs more, sometimes a lot more, but at least you can still get it.

Life Insurance Application Timeline: What to Expect at Each Stage

Author: Christopher Baldwin;

Source: everymuslim.net

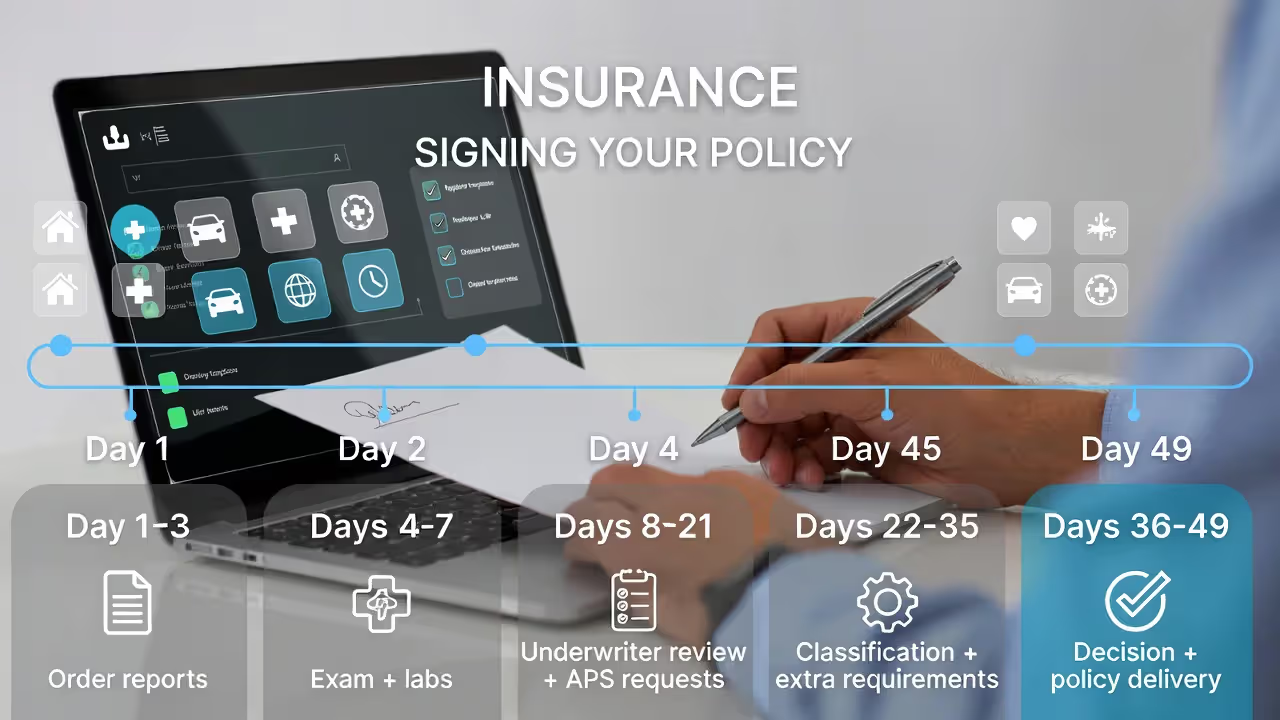

Days 1-3: You submit your application and schedule the medical exam. The insurance company immediately orders your Medical Information Bureau report, prescription drug history, and driving record. These reports usually arrive within 48 to 72 hours.

Days 4-7: The paramedical examiner visits for your medical workup. Blood and urine samples go to the lab, which processes results in three to five business days typically. If your application mentioned past medical issues—surgeries, hospitalizations, specialist visits—the insurer sends requests to those doctors' offices for copies of your records.

Days 8-21: Your lab results arrive at the underwriter's desk. They start reviewing your complete file. Need more information? Maybe they want clarification about a medication you're taking, or details about that hospitalization from 2019. They'll contact your physician's office requesting specific records. This is where delays multiply. Some medical offices respond within days; others take two to three weeks, especially if they're busy or understaffed.

Days 22-35: The underwriter finishes analyzing everything and assigns your risk classification. Straightforward cases get offers quickly. Complicated situations—conflicting information in your records, borderline lab results, unclear medical documentation—trigger additional rounds of investigation. The underwriter might order a second blood test, request records from additional providers, or send your file to a medical director for consultation. Each extra step adds one to three weeks.

Days 36-49: You receive the insurance company's decision. If approved, you review policy documents, sign them (usually electronically now), and submit your first premium payment. Your policy activates within one or two business days after they receive payment.

What makes the process faster? Applying for accelerated underwriting products that skip medical exams. Having recent lab work your doctor can quickly share. Choosing smaller death benefit amounts that don't require extensive financial documentation. Being young and healthy with minimal medical history. Responding immediately to any requests for additional information.

What slows everything down? Submitting an incomplete application that requires follow-up. Doctor's offices that drag their feet sending records. Abnormal lab results requiring retests or specialist consultation. Complex medical histories needing extra review. Financial documentation problems for large policies. Replacing an existing policy, which triggers additional scrutiny.

| Policy Type | Processing Time | Medical Exam? | How Thorough Is Review? | Who Benefits Most? |

| Term life (traditional underwriting) | 4 to 8 weeks | Yes | Very thorough—full medical workup and detailed underwriter review | Healthy people who want rock-bottom rates and large death benefits |

| Term life (accelerated underwriting) | 1 to 2 days | No | Algorithm-driven using prescription data and other records | Younger, healthy applicants with simple medical histories and coverage needs under $500,000 |

| Whole life | 6 to 10 weeks | Usually | Extremely thorough given the permanent nature and cash value component | People wanting lifetime coverage with cash accumulation; typically larger death benefits |

| Simplified issue | 1 to 2 weeks | No | Moderate—health questions only, no medical records or lab work | Applicants with minor health issues who want to skip medical exams |

| Guaranteed issue | Same day | No | None—acceptance is guaranteed regardless of health | Seniors or people with serious health conditions who can't qualify anywhere else |

Common Application Mistakes That Cause Delays or Denials

Author: Christopher Baldwin;

Source: everymuslim.net

Leaving questions blank or giving vague answers is the most common problem. Every unanswered question or unclear response triggers a follow-up call or email. Answer everything thoroughly even if the question seems irrelevant. "Have you ever consulted a physician for back pain?" might seem nosy, but the underwriter needs to know. Saying "yes" and explaining you saw a chiropractor twice for muscle strain gives them the full picture.

Misrepresenting your health history—intentionally or accidentally—creates major problems. Some people genuinely forget about medical events from years ago. Had your gallbladder removed a decade ago? It might have slipped your mind, but it's sitting in your medical records. Others deliberately leave out information, hoping it won't surface. Both approaches backfire. Insurers discover omissions through prescription databases, MIB reports, and medical records. When they catch inconsistencies, they might deny your application. Worse, if you die during the first two years (the contestability period), they can investigate the claim, discover the omission, and deny payment to your beneficiaries.

Applying at the wrong time costs money. Submit your application immediately after receiving a worrying diagnosis? You'll face higher premiums or denial. Apply while actively in treatment? Same result. Wait until a condition is well-managed—ideally for twelve months or more—and your rates improve dramatically. However, this advice has limits. If you're healthy now, don't wait for some future "perfect" moment. Health can change unexpectedly, and delaying too long might mean missing your window entirely.

Forgetting to list medications is particularly problematic since prescription databases capture everything. Say you take three medications but the database shows seven? The underwriter assumes you're hiding something. Include all prescriptions, even ones you only take occasionally or recently stopped taking. That allergy medication you take for three months every spring? List it. The pain medication you stopped six months ago? List it.

Applicants' biggest mistake is not being completely transparent about their health history. With modern data-sharing capabilities, we'll discover omissions—and when we do, it damages the applicant's credibility for everything else they've told us. Honesty isn't just ethical; it's strategically smart. We can work with nearly any health condition if we know about it upfront.

— Sarah Mitchell, CLU, Senior Underwriting Manager

Choosing the wrong coverage type wastes months. Apply for a traditional fully-underwritten policy despite health issues that make approval unlikely? You're better off with simplified issue or guaranteed issue products from the start. An experienced agent matches your situation to appropriate product types, saving you from application dead ends.

Treating your medical exam casually produces worse results than necessary. Schedule it after a stressful week with poor sleep? Your blood pressure reading will suffer. Eat a big meal two hours beforehand? Your glucose will spike. Drink alcohol the night before? Your liver enzymes will be elevated. One applicant's blood pressure can vary 20 points just based on stress levels, hydration, and rest quality. That variance can be the difference between Preferred and Standard rating—and hundreds of dollars annually.

Frequently Asked Questions About Applying for Life Insurance

The life insurance application process rewards preparation and honesty. Applicants who understand what insurers evaluate, gather documentation early, and present their health history accurately consistently get better outcomes than people who treat applications casually.

Begin with an honest health assessment and address controllable issues before applying. Work with an independent agent who can match your profile to suitable carriers and products. Prepare thoroughly for your medical exam—treat it as seriously as any important medical appointment. Answer all application questions completely and accurately, even when information seems unfavorable. Underwriters can work with disclosed issues but react negatively to omissions they discover later.

The underwriting process, while sometimes frustrating, protects both you and the insurer. Accurate risk assessment means you pay appropriate premiums and the company can reliably pay claims. The time invested in a thorough application yields decades of financial protection for your family, making the effort worthwhile.

If you hit roadblocks during underwriting—unexpected test results, requests for additional records, or initial denials—don't quit. Many applicants who face initial setbacks ultimately secure coverage by working with experienced agents, improving their health profiles, or finding carriers with more favorable underwriting for their specific situations. Persistence and preparation separate frustration from success.