Questions Before Buying Life Insurance

Questions to Ask Before Buying Life Insurance and Getting Coverage

Content

Most people spend more time researching their next smartphone than the financial product meant to protect their family's future. A 2022 industry study found that 63% of policyholders wished they'd asked more detailed questions before signing their application. The difference between asking the right questions and simply accepting what an agent offers can mean thousands of dollars and the gap between adequate protection and a coverage disaster.

Buying life insurance isn't complicated, but it requires strategic inquiry. The questions you ask determine whether you'll overpay for unnecessary features, discover exclusions only when filing a claim, or lock in coverage that actually matches your family's needs.

Why Most Buyers Ask the Wrong Questions (And What to Focus On Instead)

Walk into any insurance office and you'll hear the same questions: "What's the cheapest policy?" or "How much coverage do I need?" These aren't bad questions, but they're starting at the wrong end of the conversation.

The mistake follows a pattern. Buyers focus on price before understanding what they're buying. They ask about monthly payments without clarifying what those payments include. They accept coverage recommendations without questioning the assumptions behind them. This approach to policy understanding basics creates three common problems: purchasing insufficient coverage to save money now, buying riders that duplicate existing benefits, and selecting policy types that conflict with long-term financial goals.

Smart buyers flip the script. They ask questions that reveal how a policy actually works, what the insurer's track record shows, and whether the coverage aligns with specific family scenarios. They treat the purchase as buyer preparation for a multi-decade financial commitment, not a transaction to complete quickly.

The questions that matter most aren't about features—they're about fit. Does this policy solve the actual problem your family would face? Will this company be there when needed? Do you understand every term in the contract well enough to explain it to someone else?

12 Critical Questions About Your Coverage Needs

Author: Michael Stanton;

Source: everymuslim.net

Coverage clarification tips start with brutal honesty about your family's financial reality. These questions force specificity instead of guesswork.

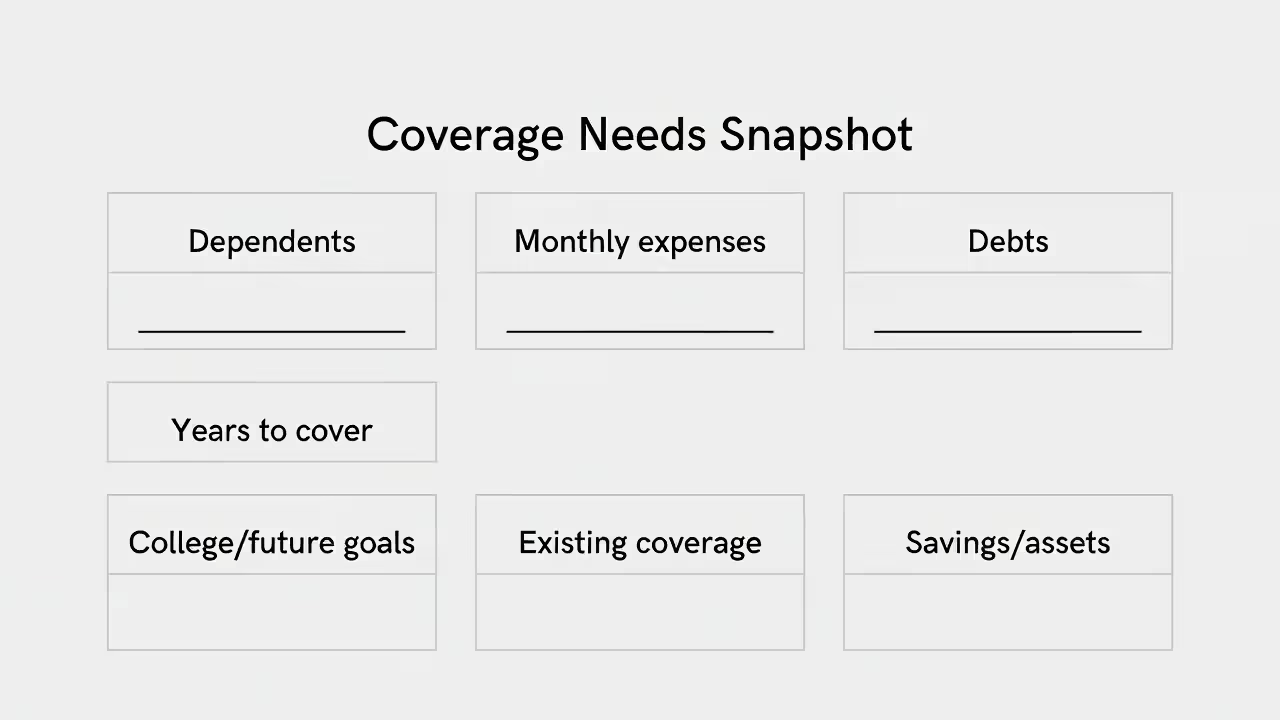

What happens to my dependents if I die tomorrow? Walk through a typical month of expenses. Mortgage or rent, utilities, groceries, childcare, transportation, insurance premiums, debt payments. Multiply by 12, then by the number of years until your youngest child reaches independence or your spouse reaches retirement age. This calculation reveals the income replacement gap your policy must fill.

How much debt would my family inherit? List every obligation: mortgage balance, car loans, credit cards, student loans, business debts, co-signed loans. Some debts disappear at death; others become your estate's problem. Your policy should prevent your family from choosing between paying creditors and maintaining their standard of living.

What income replacement duration makes sense? A 35-year-old with toddlers needs coverage lasting until those children finish college—potentially 20+ years. A 50-year-old with teenagers might need only 10 years of income replacement before retirement assets kick in. The timeline determines whether term insurance makes sense or if permanent coverage offers better value.

Should I cover final expenses separately? Funerals cost $7,000 to $12,000 on average. Estate settlement, outstanding medical bills, and final income taxes add more. Some buyers purchase small whole life policies specifically for these costs, keeping term insurance focused purely on income replacement. Others build final expenses into their total coverage calculation. Neither approach is wrong, but mixing them without intention leads to coverage gaps.

Do I need riders, and which ones matter for my situation? Waiver of premium riders continue coverage if you become disabled—critical for single-income households. Accelerated death benefit riders allow accessing funds if diagnosed with terminal illness. Child riders add coverage for children at low cost. Accidental death riders double payouts for accident deaths but statistically add little value since most deaths aren't accidental. Disability income riders provide monthly payments during disability. Each rider increases premiums; the question is whether the specific risk justifies the cost for your family.

Ask your agent to show coverage calculations using different scenarios: death in year one versus year fifteen, with and without each rider, accounting for inflation and changing family needs. The policy evaluation checklist should include side-by-side comparisons of coverage adequacy across multiple timelines.

How does my existing coverage factor in? Many people already have group life insurance through employers, often one to two times annual salary. This existing coverage reduces the gap your personal policy must fill, but relying on employer coverage creates risk—you lose it when changing jobs or during layoffs when you might need it most.

What coverage amount accounts for inflation? A $500,000 policy seems substantial today. In 20 years, inflation will erode its purchasing power significantly. Some buyers add 20-30% to their calculated need to account for inflation, while others purchase increasing benefit riders that raise the death benefit annually.

Questions That Reveal the True Cost of Your Policy

Author: Michael Stanton;

Source: everymuslim.net

Premium quotes sound straightforward until you examine what drives those numbers. These questions expose the real financial commitment.

What's included in the premium vs. what costs extra? Base premiums cover the death benefit. Everything else—riders, policy fees, administrative charges, cost of insurance increases in universal life policies—may be additional. Request an itemized breakdown showing exactly what you're paying for and which costs might change over time.

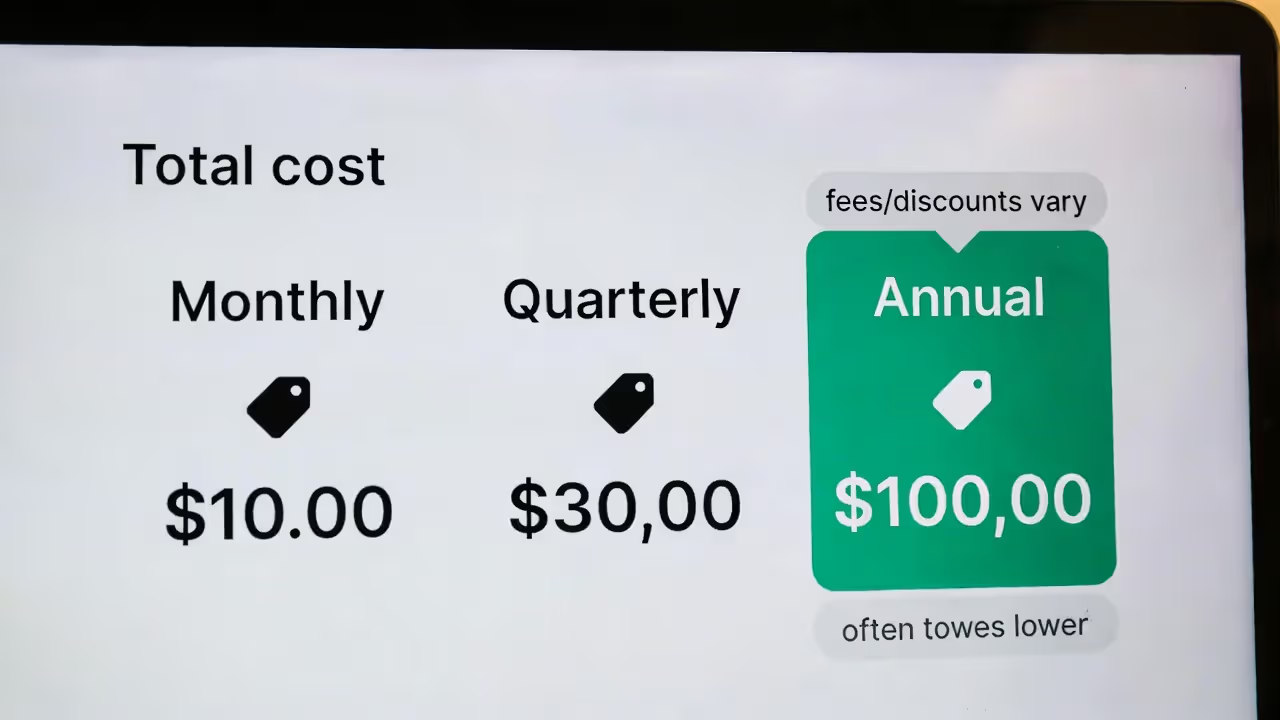

How do payment frequencies affect total cost? Annual payments typically cost less than monthly payments over a year. Insurers often charge 3-8% more for monthly billing to cover administrative costs. A $1,200 annual premium might become $104 monthly ($1,248 yearly). Over 20 years, that's an extra $960 for the convenience of monthly payments.

When do premiums increase, and by how much? Term insurance premiums stay level during the term but skyrocket if you renew after the term ends—often increasing 300-500%. Whole life premiums typically stay fixed for life. Universal life premiums can increase if policy performance underperforms illustrations. Get specific numbers: "If I renew this 20-year term at age 55, what will my new premium be?"

What fees or charges apply if I miss a payment? Most policies include a 30-31 day grace period. After that, some insurers charge reinstatement fees, require new underwriting, or let policies lapse entirely. Universal and whole life policies might automatically borrow against cash value to cover missed premiums, creating loan interest charges you didn't authorize.

Premium Structure & Cost Comparison: Term vs. Whole vs. Universal Life Insurance

| Policy Type | Upfront Costs | Ongoing Fees | Premium Flexibility | Cash Value Growth | Total 20-Year Cost Example (35-yr-old, $500K coverage) |

| Term (20-year) | Application fee ($0-$150); medical exam ($0-$300) | None (premium covers all costs) | Fixed; no flexibility until renewal | None | $18,000-$24,000 |

| Whole Life | Application fee ($0-$150); medical exam ($0-$300); first premium | Policy administration fees (built into premium); potential loan interest | Fixed; no changes allowed | Guaranteed minimum + potential dividends | $120,000-$180,000 |

| Universal Life | Application fee ($0-$150); medical exam ($0-$300) | Monthly administrative fees ($10-$30); cost of insurance charges (increase with age); surrender charges (first 10-15 years) | Flexible; can adjust premiums and death benefit | Depends on credited interest rate (not guaranteed) | $45,000-$90,000 (highly variable) |

This table illustrates why term insurance costs significantly less but offers no cash accumulation, while permanent policies cost more but build values you can access. The "total 20-year cost" column shows approximate premiums paid, not the death benefit received.

What to Ask About the Insurance Company Before You Commit

Author: Michael Stanton;

Source: everymuslim.net

Your policy is only as reliable as the company backing it. These insurer comparison questions reveal financial stability and customer treatment.

How do I verify the insurer's financial strength ratings? Four independent agencies rate insurers: A.M. Best, Moody's, Standard & Poor's, and Fitch. Look for ratings of A or higher from A.M. Best, Aa or higher from Moody's, AA or higher from S&P. These ratings assess the insurer's ability to pay claims decades from now. Your state insurance department website also lists companies under supervision or rehabilitation.

What's your claims denial rate and average payout time? Some insurers pay 98% of claims within 30 days. Others deny 10-15% of claims and take 60-90 days to process payments. Ask specifically about denial rates for policies past the two-year contestability period—these reveal how the company treats legitimate claims, not just fraud cases. Request the company's annual statement data, which includes this information.

How long have you been writing policies in my state? Insurers new to a state sometimes offer attractive rates to build market share, then raise prices or exit the market entirely. Companies with 20+ years of state presence demonstrate stability. Check your state insurance department's website for complaint ratios—the number of complaints relative to the company's market share.

What do current policyholders say about customer service? Check the National Association of Insurance Commissioners (NAIC) complaint index and sites like the Better Business Bureau. Look for patterns: Are complaints about claim denials, premium increases, poor communication, or aggressive sales tactics? A few complaints mean nothing; consistent patterns reveal company culture.

Ask about the company's claims philosophy. Some insurers pride themselves on fast, hassle-free payments. Others scrutinize every claim aggressively. You want an insurer that investigates fraud but doesn't treat every beneficiary as a suspect.

Underwriting Questions That Affect Your Approval and Rates

Author: Michael Stanton;

Source: everymuslim.net

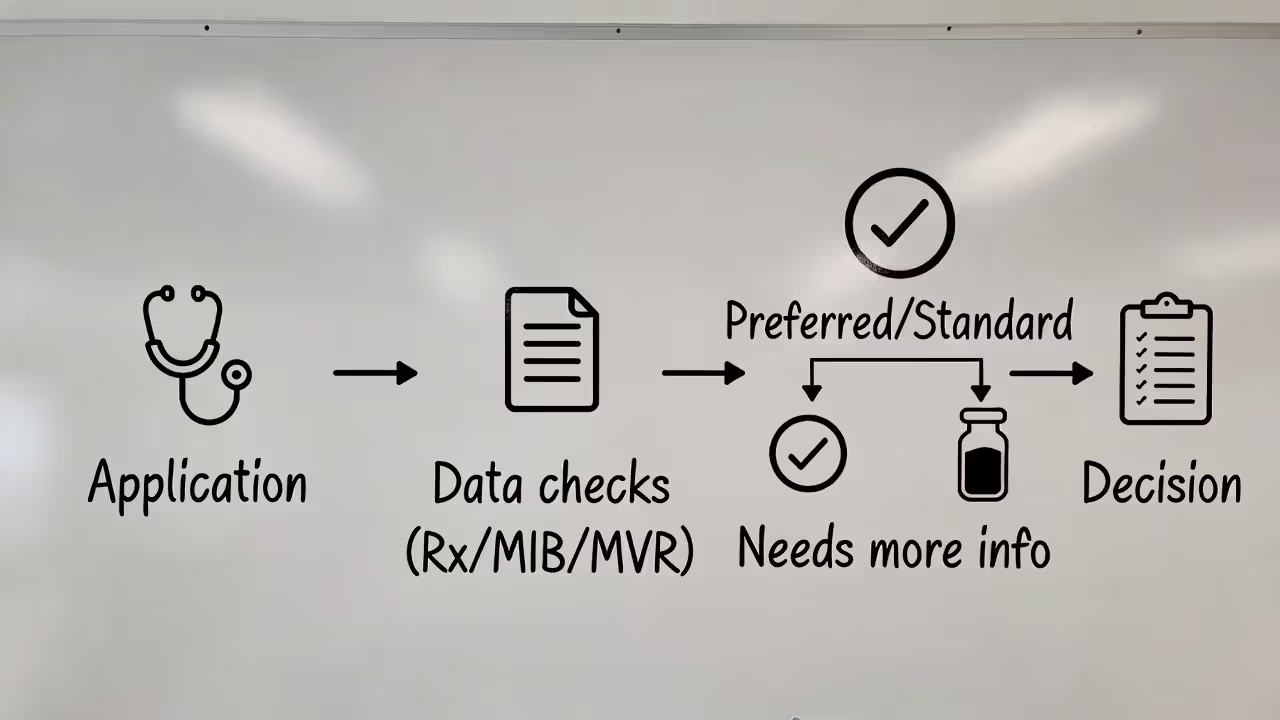

The underwriting questions guide determines whether you'll get coverage and at what price. These questions prepare you for the process and reveal opportunities to improve your rating.

Which health conditions will increase my premium or cause denial? Heart disease, cancer history, diabetes, high blood pressure, high cholesterol, obesity, and mental health conditions all affect pricing. But severity matters more than diagnosis. Well-controlled high blood pressure might add 25% to premiums; uncontrolled hypertension might mean denial. Ask specifically about your conditions: "I take medication for anxiety—how does that affect my rating?"

Do you require a medical exam, and what does it involve? Traditional policies typically require exams including height, weight, blood pressure, blood work (cholesterol, glucose, liver and kidney function), and urine samples (checking for nicotine, drugs, protein). Some insurers offer accelerated underwriting using prescription databases and medical records instead of exams for healthy applicants. Exam-free policies cost more but offer faster approval.

How far back do you review medical and lifestyle history? Most insurers review five to ten years of medical records. They check prescription databases, driving records, and the Medical Information Bureau (MIB), which tracks insurance applications across companies. Recent DUIs, reckless driving, or dangerous hobbies like skydiving affect ratings. Ask specifically: "I had a DUI six years ago—how does that impact my application?"

Can I appeal or reapply if I'm denied or rated higher? If you're offered coverage at a higher rate class than expected, you can often provide additional medical documentation supporting a better rating. If denied, ask specifically why—sometimes it's correctable (like outdated medical records) or you can reapply after improving health markers. Some insurers specialize in high-risk cases; a denial from one company doesn't mean universal denial.

What happens if my health improves after purchase? Some insurers allow re-rating if you lose significant weight, quit smoking for 12+ months, or improve other health markers. This isn't automatic—you must request reconsideration and provide documentation. Not all companies offer this option, so ask upfront if it's available.

Smokers pay 2-3 times more than non-smokers. If you quit, most insurers require 12 months nicotine-free before re-rating. Vaping counts as tobacco use at most companies. Ask about the specific definition: "Does occasional cigar smoking count as tobacco use?"

Policy Terms You Must Clarify Before Signing

Author: Michael Stanton;

Source: everymuslim.net

The policy contract contains the actual agreement, not the marketing materials or agent's verbal promises. These coverage clarification tips prevent surprises when filing claims.

What specific events are excluded from coverage? Most policies exclude suicide during the first two years, death resulting from illegal activities, and death while committing a felony. Some exclude death during aviation activities (except as a commercial passenger), war or acts of war, and deaths in certain countries. Accidental death policies add extensive exclusions: death from illness, drug overdoses (even accidental), and deaths while intoxicated. Get the exclusions list in writing and ask about scenarios relevant to your life.

Can the insurance company cancel my policy, and under what conditions? After the contestability period (typically two years), insurers cannot cancel for health reasons as long as you pay premiums. They can cancel for non-payment or fraud discovered during the contestability period. Some universal life policies lapse if cash value depletes—the company doesn't "cancel" but stops coverage when your account can't cover costs.

What's the contestability period, and what triggers an investigation? For two years after policy issue, insurers can investigate claims and deny coverage if they discover material misrepresentations on the application. This doesn't mean they investigate every claim, but they can. After two years, they generally must pay claims regardless of application errors (except outright fraud). Ask: "What constitutes a material misrepresentation? If I forgot to mention a doctor visit five years ago, is that grounds for denial?"

How does the beneficiary designation process work? Primary beneficiaries receive the death benefit first. Contingent beneficiaries receive it if primary beneficiaries predecease you. You can name multiple beneficiaries with percentage allocations. Revocable beneficiaries can be changed anytime; irrevocable beneficiaries cannot be changed without their consent (rare except in divorce situations). Ask about naming trusts as beneficiaries if you have minor children—direct beneficiary designations to minors create legal complications.

What conversion or portability options exist? Many term policies include conversion rights allowing you to convert to permanent insurance without new underwriting, typically within the first 10-20 years. This protects you if health deteriorates and you want permanent coverage. Group policies sometimes offer portability, letting you take coverage with you when leaving an employer. These options cost nothing unless used but provide valuable flexibility.

Request a policy illustration showing guaranteed values versus projected values. Whole life and universal life illustrations show optimistic projections based on current assumptions. The guaranteed columns show worst-case scenarios. Ask: "What happens if performance matches guarantees instead of projections?"

The single most overlooked question that leads to buyer's remorse is 'What problem am I actually solving?' People buy policies based on coverage amounts or monthly payments without clearly defining the financial gap the insurance must fill. When I ask clients to describe exactly what would happen to their family financially if they died tomorrow—who would struggle, with what expenses, for how long—the conversation transforms from abstract to concrete. That clarity drives every other decision.

— Sarah Chen

FAQ

The questions you ask before buying life insurance determine whether you'll purchase appropriate protection or discover costly mistakes when it's too late to fix them. Start with coverage needs—understanding exactly what financial problem you're solving. Move to cost structures, ensuring you know what you're paying for and when costs might change. Evaluate the insurer's stability and reputation, since they must be financially sound decades from now. Prepare for underwriting by understanding how your health and lifestyle affect pricing. Clarify every policy term that could affect claims payment.

Most importantly, ask yourself the hard questions about whether you truly understand what you're buying and whether it fits your overall financial plan. The policy evaluation checklist isn't about asking the most questions—it's about asking the right questions that reveal whether this specific policy from this specific company solves your family's specific needs.

Your family's financial security shouldn't depend on assumptions, agent assurances, or marketing materials. It should rest on clear answers to direct questions, documented in policy contracts you've read and understood. The hour you spend asking thorough questions before purchasing prevents years of regret and potentially prevents financial disaster for the people who depend on you.