Open life insurance contract on a desk with a checklist of key sections to review.

How to Read a Life Insurance Policy: A Step-by-Step Guide for Policyholders

Content

Most people spend more time reading their smartphone's terms of service than their life insurance contract. That's a problem. Your policy represents a promise worth hundreds of thousands—maybe millions—of dollars, yet it sits in a drawer gathering dust while you hope you understood what the agent explained during sign-up.

I've seen families blindsided at the worst possible moment. A widow discovers her husband's policy won't pay because he died during year one of a two-year suicide exclusion. A daughter learns her father's aviation hobby voided his coverage. A son finds out his mother's "guaranteed" benefits weren't actually guaranteed at all. These weren't bad policies—they were unread policies.

Let's fix that.

What Makes Life Insurance Policies Difficult to Understand?

Your policy reads like it was written by lawyers. That's because it was—specifically, attorneys whose job involves anticipating courtroom battles over every comma and semicolon. Their goal isn't helping you understand your coverage at 10 PM on a Tuesday. They're drafting ironclad contracts that insurance commissioners will approve and judges will uphold.

Here's what makes these documents so brutal to read:

Every third word gets capitalized because it has a "special definition" buried somewhere else in the contract. You'll see phrases like "the Insured under this Policy shall receive Benefits according to the Schedule." To understand that sentence, you need to flip to three different sections explaining what those capitalized terms actually mean.

Each insurance company organizes its contracts differently, even though state regulators require the same basic provisions. Company A puts suicide clauses on page 2 in bold font. Company B hides theirs in paragraph 14(c) under "Limitations on Coverage." You can't skim these documents using knowledge from your previous policy because nothing's in the same place.

The real danger? Small words with massive consequences. "Any" versus "own" in a disability definition. "And" versus "or" in a beneficiary designation. "May" versus "shall" in a payment obligation. These tiny differences determine whether your family gets $500,000 or nothing.

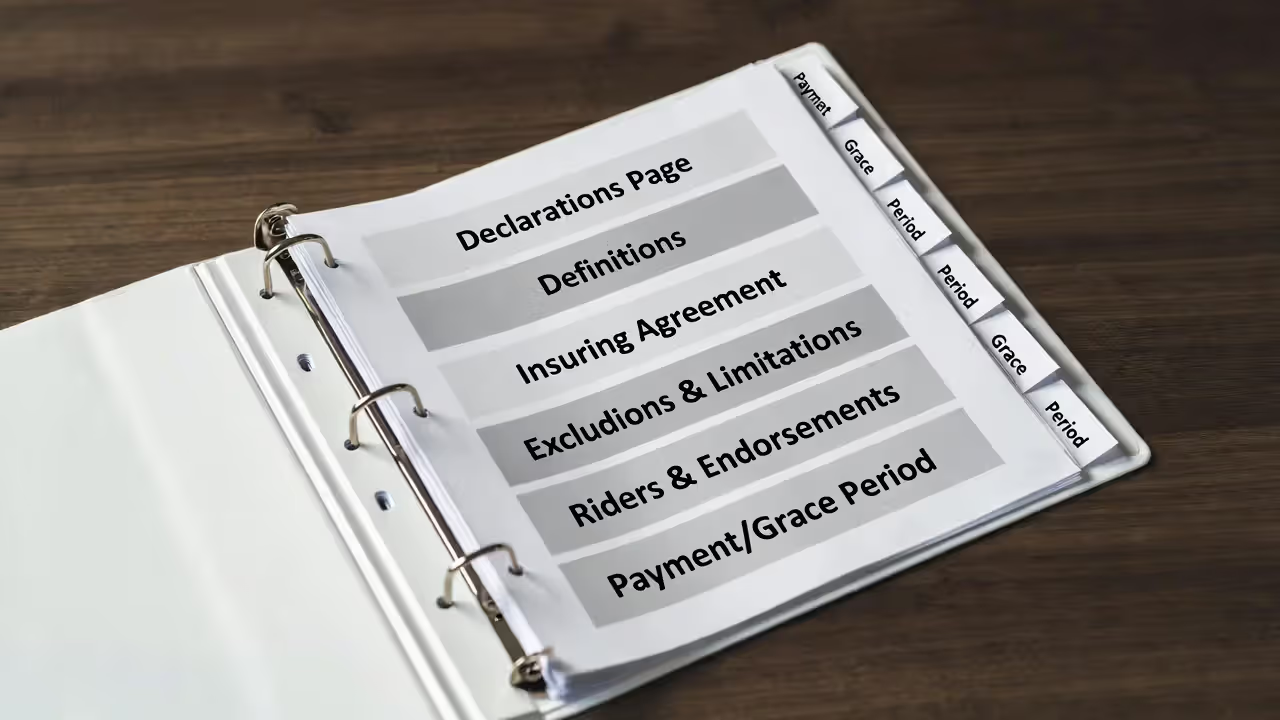

The Essential Sections Every Life Insurance Policy Contains

Author: Olivia Ramsey;

Source: everymuslim.net

Think of your policy like a legal manual with predictable chapters. Once you know the structure, you can navigate any insurer's contract.

Declarations Page: Your Policy at a Glance

This single sheet functions as your coverage snapshot. It lists your policy number (you'll need this for every customer service call), your death benefit amount, who gets the money when you die, and what you pay monthly or annually to keep everything active.

Pull this page out the moment your policy arrives. I mean immediately—before you file it away. Check that your $750,000 application actually resulted in a $750,000 policy, not $500,000 because of an underwriting change. Verify your spouse's name is spelled "Catherine" not "Katherine" if that's her legal name. Make sure your premium matches your budget, because if you got quoted $85 monthly and the declaration says $185, something went sideways during underwriting.

One client discovered his declarations page listed his ex-wife as beneficiary instead of his current wife. The policy had been issued during his divorce proceedings, and he'd never checked. Had he died before catching that error, his ex-wife—who he hadn't spoken to in three years—would've received $400,000.

Definitions Section: Where Terms Are Explained

Somewhere in your contract, probably near the front or shoved in an appendix, sits a section that defines every capitalized term. This is your Rosetta Stone.

When your policy mentions "Total Disability," you might think: "Can't work my job anymore." The definition might say: "Unable to perform the duties of ANY occupation for which you're reasonably qualified by education, training, or experience." See the problem? You could be a surgeon who loses fine motor control in your hands. You can't do surgery, but you could teach medical students. Under this definition, you're not totally disabled.

Or consider "Beneficiary." Sounds simple—it's whoever you named to get the money, right? But the definitions section might distinguish between "Primary Beneficiary," "Contingent Beneficiary," "Revocable Beneficiary," and "Irrevocable Beneficiary." Each term triggers different rules about when you can change designations or borrow against your policy.

Pro tip: Keep a printed copy of the definitions section in the front of your policy folder. When you read other sections and hit a capitalized term, you won't need to hunt through the entire document.

Insuring Agreement: The Core Promise

Author: Olivia Ramsey;

Source: everymuslim.net

This is the contract's beating heart—the insurer's fundamental promise to pay. But read carefully, because even this "simple" promise contains conditions.

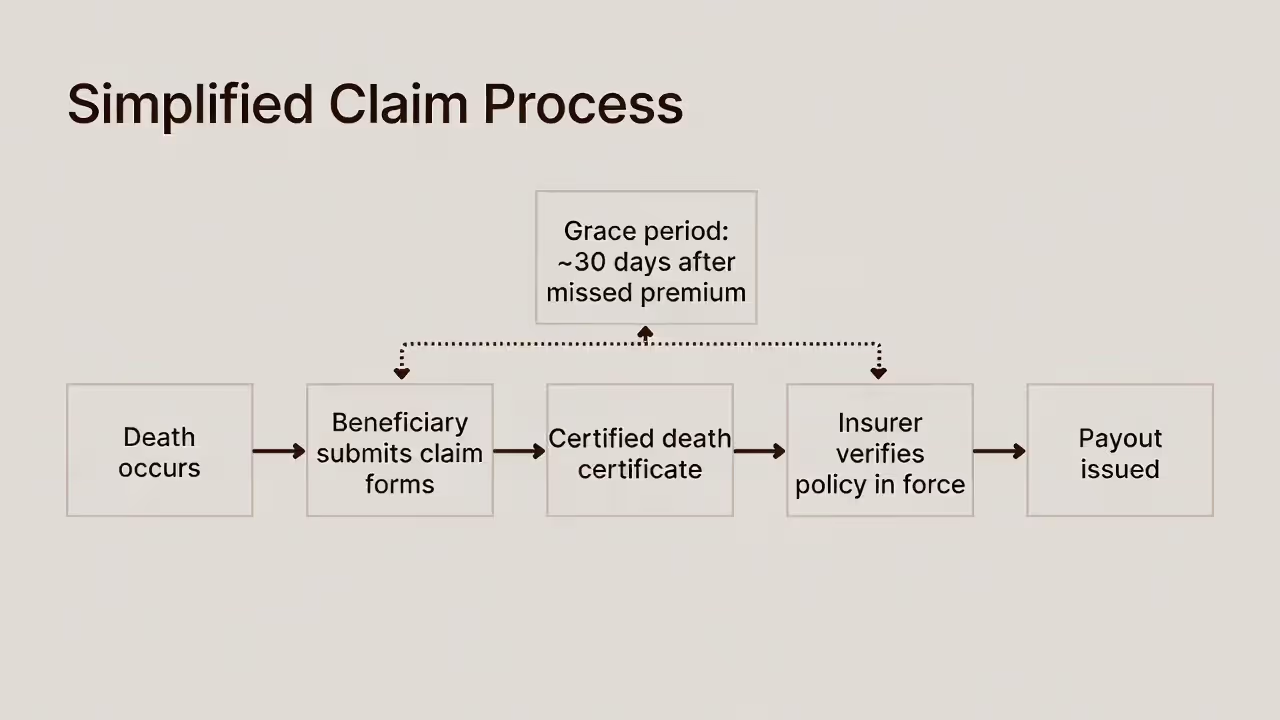

Typical language: "We will pay the Death Benefit to the Beneficiary upon receipt of due proof of the Insured's death, provided this policy is in force." That "due proof" phrase matters. Your beneficiaries can't just call and say you died. They'll need a certified death certificate, completed claim forms, and sometimes additional documentation depending on death circumstances.

The "provided this policy is in force" part is equally important. If you die three days after your grace period expires because you forgot to pay your premium, the insurer owes nothing. Your policy lapsed. Coverage ended. The insuring agreement's promise became void the moment you missed that payment deadline.

Some agreements specify payment timing: "within 60 days of receiving proof of death" or "within 7 days of claim approval." If your policy says 60 days and the insurer takes 90, you might be entitled to interest on the delayed payment under your state's insurance laws.

Exclusions and Limitations

This section lists scenarios where the insurer keeps your premiums but pays nothing. Or pays less than you expected. These clauses protect insurers from catastrophic losses and fraud, but they also create coverage gaps you need to understand.

I'll dive deeper into exclusions in a dedicated section below, but here's your overview: This is where you'll find suicide clauses (typically no payment if you die by suicide within two years of policy issue), aviation restrictions (private pilot? you might not be covered), war exclusions (death during military combat might be excluded), and material misrepresentation consequences (lie on your application, lose your coverage).

The difference between exclusions and limitations trips people up. An exclusion means zero payment. A limitation means reduced payment. If you die during the contestability period and the insurer discovers you understated your weight by 50 pounds, they might invoke a limitation—paying benefits based on what your premium should have been at your actual weight, rather than denying the claim entirely.

Riders and Endorsements

Riders are contract modifications that add features or change terms. Think of them as legal sticky notes attached to your base policy. An accelerated benefit rider might let you collect part of your death benefit early if you're diagnosed with a qualifying terminal condition. A child term rider extends coverage to your kids. A guaranteed insurability rider lets you buy more coverage later without medical exams.

Each rider comes with its own mini-contract: eligibility rules, definitions, exclusions, costs. A long-term care rider might only activate after you've been unable to perform at least two "activities of daily living" for 90 consecutive days. What counts as an activity of daily living? The rider defines six specific activities—bathing, dressing, eating, toileting, transferring, and continence. If you can't dress yourself or bathe independently for three months straight, the benefit triggers. Fall short of 90 days? The rider stays dormant.

Some riders come free; others cost extra. Some remain active for your policy's lifetime; others expire after certain periods. Read each rider's specific terms as carefully as you read the base policy.

Decoding Common Insurance Terminology in Your Contract

Author: Olivia Ramsey;

Source: everymuslim.net

Insurance companies speak their own language. Here's your translation guide:

| Technical Insurance Language | Plain English Translation |

| Beneficiary designation | Who you've chosen to receive money when you die. You can typically update this anytime unless you selected an "irrevocable" option, which locks it in. |

| Cash accumulation component | Permanent policies build a savings element that grows without immediate tax consequences. You can access this through loans or surrenders, but both options reduce what your family eventually receives. |

| Contestability window | The first two years after your policy starts, during which the insurance company can investigate whether you told the truth on your application and potentially cancel your coverage. |

| Death benefit payout | The dollar amount paid when you die. Some policies maintain the same amount throughout; others decrease over time according to a predetermined schedule. |

| Payment grace window | You get roughly 30 days after missing a payment before your policy cancels. Coverage continues during this window, but if you don't pay by the deadline, everything terminates. |

| Incontestability provision | After your contestability window closes, insurers lose most ability to cancel coverage or deny claims based on application inaccuracies (fraud being the notable exception). |

| Policy termination | What happens when you stop paying and your grace window expires. Your coverage ends. Some policies allow reinstatement if you act quickly and prove you're still insurable. |

| Cash value borrowing | Taking an advance against your policy's accumulated savings. You're accessing your own money, but the insurance company charges interest, and any unpaid balance plus interest gets subtracted from your eventual death benefit. |

| Coverage payment | What you owe monthly, quarterly, or annually to maintain active coverage. Amount might stay level for decades or vary depending on your policy type. |

| Policy modification attachment | An optional add-on that changes your base contract. Some modifications cost nothing; others increase your payment. |

| Early cancellation penalty | Permanent policies often charge hefty fees if you cancel during the first 10-20 years. These penalties can consume most of your accumulated cash value. |

| Risk evaluation process | How insurers decide whether to cover you and what to charge. They review medical records, conduct exams, check driving records, and evaluate lifestyle factors. |

Getting these terms wrong leads to expensive mistakes. That "payment grace window" isn't forgiveness—it's your final deadline before losing coverage entirely. When you see "cash value borrowing available," don't celebrate free money. You're taking an advance on your family's benefit with interest charges that compound over time.

How to Identify and Understand Policy Exclusions

Author: Olivia Ramsey;

Source: everymuslim.net

Finding exclusions takes detective work because they scatter throughout your contract, not just in the "Exclusions" section.

The suicide provision typically appears near the insuring agreement or in its own prominent paragraph. Standard language: No death benefit if you die by suicide within 24 months of policy issue. Instead, beneficiaries receive premium refunds—every payment you made, returned without interest. After that initial 24 months passes, suicide gets covered like any other cause of death.

Why does this exist? Without it, someone facing financial catastrophe could buy a $2 million policy Monday and die by suicide Wednesday, leaving their family wealthy. That's insurance fraud, not insurance protection. The two-year window balances protecting insurers from fraud while still providing coverage for suicides that occur after the policy has been in force.

Aviation exclusions vary wildly between carriers. Every policy covers commercial airline passengers—you're fine flying Delta to visit relatives. Private aviation gets messy. Some insurers exclude any death involving private aircraft unless you pay extra premiums for aviation coverage. Others cover you as a private plane passenger but not as a pilot. Still others cover private pilots who hold specific certifications but exclude student pilots or experimental aircraft.

I worked with a client who flew small planes recreationally every weekend. His policy excluded "death occurring during operation of any aircraft." He assumed that meant as a pilot, so he felt safe as a passenger. Wrong. "Operation of any aircraft" included being in the plane at all. When he switched insurers to one that only excluded piloting, not riding, his family's risk dropped dramatically.

Military and war exclusions protect insurers when governments send troops into combat zones. Typical language: "We will not pay if death occurs while the Insured is serving in military forces during war, declared or undeclared, or while serving in any military unit during conflict in a hostile fire zone."

What counts as a "hostile fire zone"? Usually wherever the U.S. Department of Defense designates service members as receiving imminent danger pay or hostile fire pay. Some policies exclude all military service during wartime, even stateside desk jobs. Others only exclude active combat zones. Veterans and active-duty personnel need to explicitly review these provisions and ask about military-friendly policies that minimize or eliminate war exclusions.

Application misrepresentation isn't listed as an "exclusion," but it functions identically during your contestability period. State on your application that you've never smoked when you actually smoke a pack daily? If you die within two years and the insurer investigates and discovers the truth, they can deny your entire claim. After the contestability period ends, this option disappears unless the insurer proves intentional fraud (remarkably hard to prove).

Why do exclusions exist at all? Risk management. Insurers calculate premiums based on average mortality risk. People who skydive, pilot helicopters, or deploy to war zones face dramatically higher risk than the average population. Rather than charge everyone higher premiums to cover these high-risk activities, insurers exclude them or charge extra to cover them. It's economically rational, even if frustrating when you're the helicopter pilot who needs coverage.

Reading and Comparing Benefit Clauses Across Different Policies

Author: Olivia Ramsey;

Source: everymuslim.net

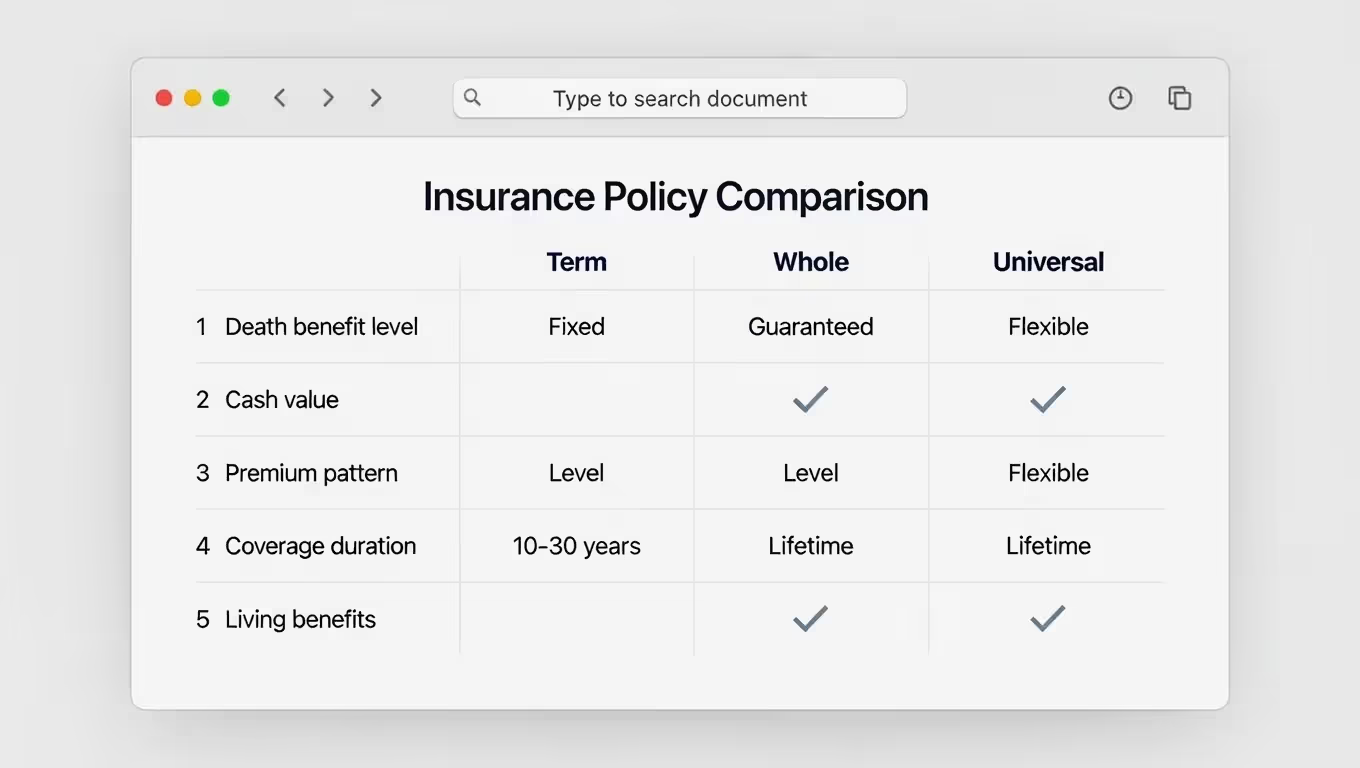

Your benefits vary enormously depending on which type of policy you purchased. Here's how term, whole, and universal life stack up:

| Policy Feature | Term Life Insurance | Whole Life Insurance | Universal Life Insurance |

| How the death benefit works | Stays level during your selected period (maybe 10, 20, or 30 years), then either disappears or becomes prohibitively expensive to continue | Contractually guaranteed to stay level for your entire life assuming you pay required premiums | Adjustable within policy limits—you can increase coverage with underwriting or decrease it based on changing needs |

| Savings component included | Zero savings element; pure death benefit protection that expires | Builds guaranteed cash reserves that grow based on contractual rates; available for borrowing or withdrawal | Accumulates cash based on current interest rates the insurer credits; more accessible than whole life but with fewer guarantees |

| Payment structure | Locked in for your term; expect dramatic increases if you renew past the initial period | Fixed payment that never changes; the insurer can't raise it | Variable within limits—you might skip payments or pay extra depending on how much cash you've accumulated |

| How long coverage lasts | Specific duration (10, 20, 30 years are common); some allow conversion to permanent options | Your entire lifetime provided you pay required amounts | Lifetime if you fund it properly; underfunding can cause unexpected lapses even decades after purchase |

| Access to benefits while living | Usually none except occasional conversion privileges | Might include provisions to advance benefits if you're diagnosed with qualifying terminal conditions | Typically offers flexible cash access plus death benefit acceleration for various qualifying events |

Accelerated benefits deserve your close attention. These contract provisions advance part of your death benefit while you're still breathing if you meet specific medical criteria. Terminal illness riders typically require a physician to certify you have 12 months or less to live (some policies say 24 months). Once certified, you can request an advance—often up to 50-75% of your death benefit—to cover medical bills, travel, or final expenses.

The advance isn't free money. Every dollar you take reduces what your beneficiaries eventually receive. Some insurers also charge administrative fees—maybe 2-4% of the accelerated amount—though many now include this feature at no extra cost.

Beyond terminal illness, many modern policies offer critical illness advances. Get diagnosed with a heart attack, stroke, cancer, or end-stage renal failure? You might qualify for a lump sum payment ranging from $10,000 to the full death benefit depending on your rider terms. The diagnosis triggers payment immediately rather than waiting until death.

Chronic illness provisions pay if you lose ability to perform multiple "activities of daily living" for at least 90 consecutive days. Can't bathe yourself or use the toilet independently for three months? The rider activates. But note that 90-day requirement—suffer for 89 days and you get nothing.

Policy disputes rarely arise because insurers are acting in bad faith. They usually happen because policyholders never understood what they bought. Reading your contract isn't optional—it's your fundamental responsibility as a contracting party. If provisions confuse you, ask questions before you file a claim, not during the claim when it's too late to fix misunderstandings.

— Sarah Mitchell

Long-term care riders convert your death benefit into nursing home or home health care funding. If you need a nursing facility, the rider might pay $3,000-$5,000 monthly toward costs, drawn from your death benefit. Need care for four years at $4,000 monthly? That's $192,000 subtracted from what your family receives. But if you never need long-term care, your full death benefit passes to beneficiaries.

Conversion privileges in term policies deserve special mention. These clauses let you convert to permanent coverage without new medical underwriting. Why does this matter? Imagine you buy a 20-year term policy at age 30 when you're healthy. At age 45, you're diagnosed with diabetes and high blood pressure. Your term expires at age 50, but you still need coverage. With a conversion option, you can switch to permanent coverage despite your health changes. Without it, you'd need new underwriting and face higher rates or potential denial.

Conversion terms vary dramatically. Some policies only allow conversion during the first five or ten years. Others permit it throughout the entire term. Some let you convert to any permanent product the insurer offers. Others restrict you to specific products, often the most expensive ones. Read your conversion provision carefully if you think you might want permanent coverage eventually.

Red Flags and Mistakes to Avoid When Reviewing Your Policy

Author: Olivia Ramsey;

Source: everymuslim.net

Even diligent readers make predictable errors. Watch for these:

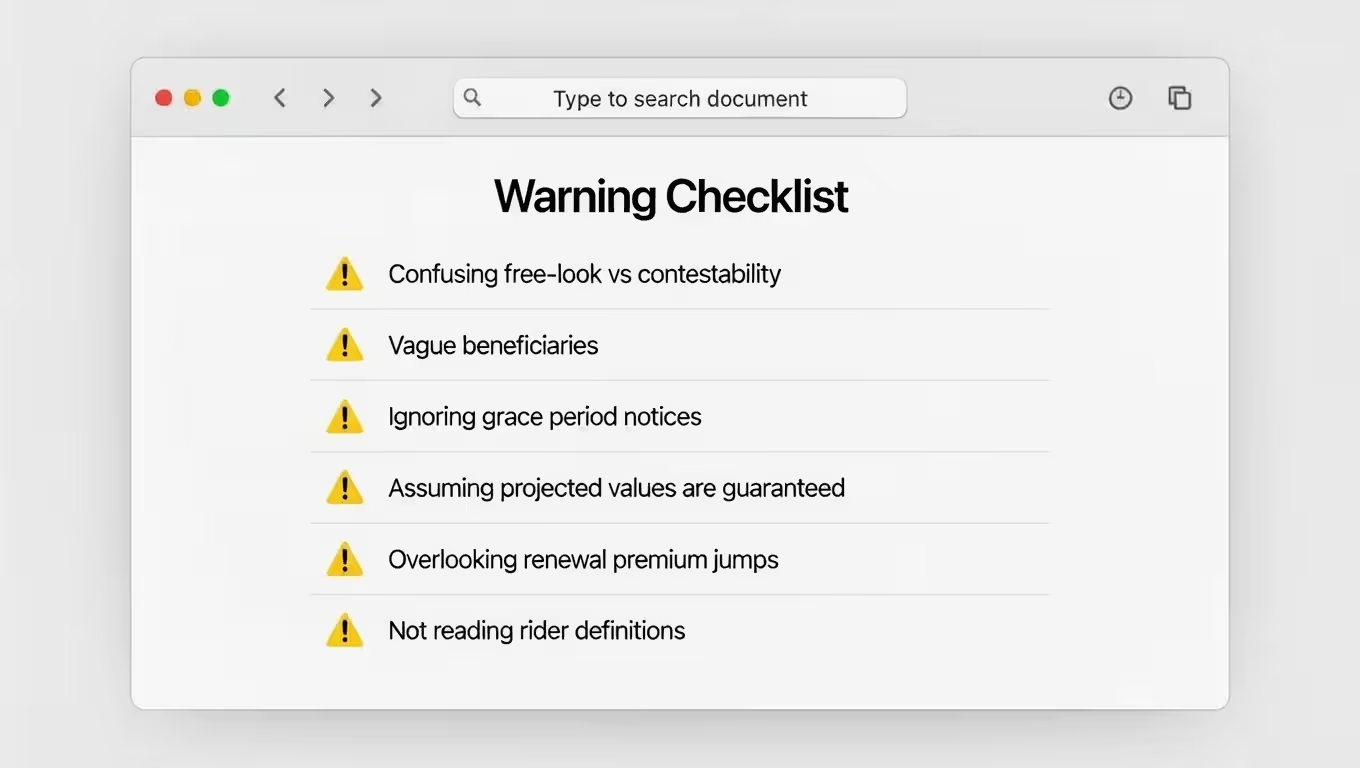

Mixing up your free-look period with your contestability period causes confusion. Your free-look period—typically 10 to 30 days after your policy arrives—functions as a money-back guarantee. Don't like what you bought? Cancel during this window and receive full premium refunds. The contestability period (usually two years) is when insurers can investigate your application and potentially void coverage if you lied. Completely different concepts with different time frames and different consequences.

Vague beneficiary designations create nightmares during claim processing. Naming "my children" sounds clear until circumstances change. You remarry and have more children—do they count? You have stepchildren—are they included? An adult child changes their name—will that cause confusion? Instead: "John Michael Smith, son, born March 15, 1995, and Sarah Elizabeth Smith, daughter, born June 3, 1998."

Also specify contingent beneficiaries—backups who receive benefits if your primary beneficiaries die before you. Without contingents, your death benefit might flow to your estate, triggering probate, delaying distribution, exposing funds to creditors, and creating tax complications.

Misunderstanding grace period mechanics leads to accidental policy lapses. Miss a payment and you've got roughly 30 days to catch up while coverage continues. Miss that 30-day deadline and your policy terminates. Many people assume insurance companies will send repeated warnings or call to remind them. Some do. Many don't. They send one notice saying "payment overdue, grace period expires March 15" and if you miss that date, coverage ends.

Reinstating lapsed policies is possible but painful. You'll need to reapply, prove you're still insurable through new underwriting, pay all back premiums with interest, and hope the insurer approves. If your health deteriorated during the lapse, you might face higher rates or denial.

Confusing guaranteed versus projected values in permanent policies creates false expectations. Your whole life illustration shows guaranteed cash values—contractual minimums the insurer must deliver regardless of market conditions. It also shows non-guaranteed dividends that might increase your values. Those dividends are projections based on current performance, not promises. Economic downturns can reduce or eliminate them.

Universal life projections get even trickier. Illustrations show current interest crediting rates (maybe 4-5%) and guaranteed rates (often 2-3%). The difference seems small until you project it over 30 years. At 5%, your cash value might reach $150,000. At 2%, you might barely reach $50,000. Assume you'll get 5% forever and you might face a shock when the insurer cuts rates during a recession.

Ignoring term policy renewal provisions sets you up for sticker shock. Your 20-year term costs $50 monthly with level premiums throughout. Fantastic—until year 21 arrives and the premium jumps to $300 monthly. The policy guarantees renewability but not price. At renewal, you get repriced based on your current age, often at drastically higher rates. Some term policies expire entirely at renewal, leaving you uninsured unless you buy new coverage.

If you might need coverage beyond your initial term, evaluate your options before the term expires. Some people assume they can just renew affordably. They can't. Plan ahead by checking conversion options, shopping for new coverage before your term ends, or buying a longer initial term.

Frequently Asked Questions About Life Insurance Policy Documents

When to Seek Professional Help Interpreting Your Policy

Most policies are readable with patience and perhaps a few clarifying phone calls to your agent. Some situations demand expert guidance.

If you're considering a policy loan or full surrender, talk to a financial advisor first. These decisions trigger tax consequences, permanently reduce death benefits, and might produce unexpected results like taxable income on surrenders or policy lapses if loan interest isn't paid. An advisor can model different scenarios showing exact outcomes under various approaches.

When you're comparing multiple policies from different carriers, an independent broker adds value by explaining subtle but important differences. Two policies might both offer $500,000 coverage with similar premiums, but one insurer has stronger financial ratings, better dividend history, more flexible underwriting for health conditions, or superior rider options. These distinctions aren't obvious from reading contracts alone.

Estate planning involving trusts, business buy-sell agreements, or coverage exceeding federal estate tax exemption amounts requires attorney involvement. Life insurance intersects with trust law, tax law, and business law in complex ways. A policy owned by an irrevocable life insurance trust (ILIT) operates under different rules than personally owned coverage. Structured incorrectly, your $3 million policy could trigger $1 million in estate taxes. Structured properly, it passes tax-free.

If you're filing a claim and the insurer denies it or offers significantly less than expected, consult an attorney before accepting their decision. Insurance law requires specialized knowledge, and attorneys focused on this area understand how to interpret ambiguous policy language, challenge improper denials, and negotiate settlements. Many work on contingency—they only collect fees if they recover benefits for you.

Warning signs you need professional help: policy language directly contradicting what your agent told you during the sales process, provisions that seem internally inconsistent or contradictory, riders that don't clearly explain eligibility or activation, or situations where the insurer's explanation simply doesn't make logical sense. Trust your instincts—if something feels wrong, seek a second opinion.

State insurance departments provide free resources worth exploring. Most maintain consumer assistance divisions that answer questions, distribute educational materials, and sometimes mediate disputes between policyholders and insurers. They won't provide legal advice or represent you in disputes, but they can clarify state regulations and help you understand your rights under insurance law.

Reading your life insurance policy isn't optional homework you can skip. This contract governs financial protection for the people who matter most in your life, and assumptions about coverage create devastating problems when families file claims after your death.

You don't need a law degree to understand your policy. You need patience, attention to detail, and willingness to ask questions when language confuses you. Start with the declarations page confirming basic facts match what you purchased. Work through each major section methodically. Pay extra attention to exclusions, beneficiary designations, and riders modifying your base coverage. Cross-reference defined terms, compare what you thought you bought against what the contract actually delivers, and immediately document any discrepancies.

Your policy should evolve as your life changes. Review it annually. Update beneficiaries as your family grows or changes. Don't hesitate to seek professional guidance for complex situations. The two hours you invest understanding your policy today might save your family months of confusion, thousands in legal fees, and immeasurable stress when they need to file a claim.