Life Insurance Buying Guide

Online Life Insurance Application Guide

Content

Remember when getting life insurance meant scheduling an appointment with an agent at your kitchen table? You'd spend an hour answering questions on paper forms, then a medical professional would visit your home to draw blood and check your vitals. Six weeks later, you'd finally hear whether you were approved.

That entire ritual has been flipped on its head. My colleague applied for $350,000 in coverage last month during her daughter's soccer practice—approval came through before halftime. This speed creates possibilities our parents never had, but it also raises questions about which application method actually fits your needs.

How Life Insurance Applications Have Changed in the Digital Era

The insurance industry spent decades perfecting the traditional model. Then technology companies entered the market around 2016, and everything accelerated.

Back in 2018, if you wanted $400,000 in term life coverage, you'd typically go through these steps: initial phone consultation with an agent (30-60 minutes), paper application mailed back and forth (one week), paramedical exam scheduled at your convenience (another week of coordination), blood and urine shipped to labs (3-5 days), underwriter review (2-3 weeks minimum). Total timeline: 4-8 weeks on average.

Flash forward to now. A 34-year-old friend with no health issues applied for $500,000 last Tuesday afternoon. She entered information on her phone, authorized some background checks, and received approval that evening. Coverage started the next day after she paid the first premium.

But here's what most articles won't tell you clearly: digital speed works for specific profiles. That same friend's father, who's 58 with treated high blood pressure, went through a four-week process even using a "digital-first" platform. His application required physician records and lab work that no algorithm felt comfortable approving automatically.

The traditional path still exists because it handles complexity better. You need $2 million at age 56? You're getting an exam, period. The shift isn't really about replacing old methods—it's about adding fast lanes for people who fit specific criteria.

What matters most: knowing which lane you're in before you start. Your age, health background, tobacco use, and requested coverage amount determine whether you'll finish in fifteen minutes or fifteen business days.

Breaking Down Digital Applications: Step-by-Step Process Explained

Author: Christopher Baldwin;

Source: everymuslim.net

Digital platforms follow surprisingly similar patterns, though the visual design varies wildly between companies.

First, you'll set up login credentials with an email and password. Basic demographic questions come next: birth date, sex assigned at birth, whether you've used tobacco products in the past three years. Then height and weight, which seem simple but matter enormously. Insurance companies use BMI calculations to assess risk, and someone who's 5'9" weighing 210 pounds gets different rate classes than someone the same height at 165 pounds.

The health history section arrives next, and this determines everything. You'll see checkboxes for conditions: heart disease, stroke, cancer, diabetes, kidney problems, liver disease, mental health diagnoses, sleep apnea. Each "yes" triggers follow-up questions about diagnosis dates, treating physicians, current medications, and your most recent status updates.

Here's where people stumble: you're asked to list every medication you currently take or have taken in the past five years. Most applicants remember their daily prescriptions but forget the antibiotic they took for eight months ago, the sleep medication they use occasionally, or the antidepressant they stopped taking three years back.

Why does this matter? Because you're about to click a button authorizing prescription database access. The system queries records from major pharmacy chains and pharmacy benefit managers. Within seconds, the platform sees every prescription filled under your name since roughly 2018. A forgotten medication creates an obvious red flag: "Applicant didn't disclose fluoxetine filled six times between January 2021 and July 2022."

You'll also permit checks through the Medical Information Bureau—a consortium where insurance companies share applicant data. If you applied for coverage with another carrier three years ago and disclosed diabetes then, that information lives in MIB records. Claiming "no diabetes history" now creates immediate contradictions.

Document uploads come next on many platforms. Expect to photograph your driver's license for identity verification. You'll enter beneficiary details: full legal names (not nicknames), Social Security numbers, birth dates, and relationship to you. Some applications for higher amounts request documentation of your income or existing assets to establish insurable interest—proving you're not trying to insure yourself for more than makes financial sense.

Most straightforward applications take 20-40 minutes. Complex health backgrounds stretch this to 60-90 minutes because you're providing detailed context about multiple conditions, surgeries, or ongoing treatments.

Common Application Mistakes That Delay Approval

Author: Christopher Baldwin;

Source: everymuslim.net

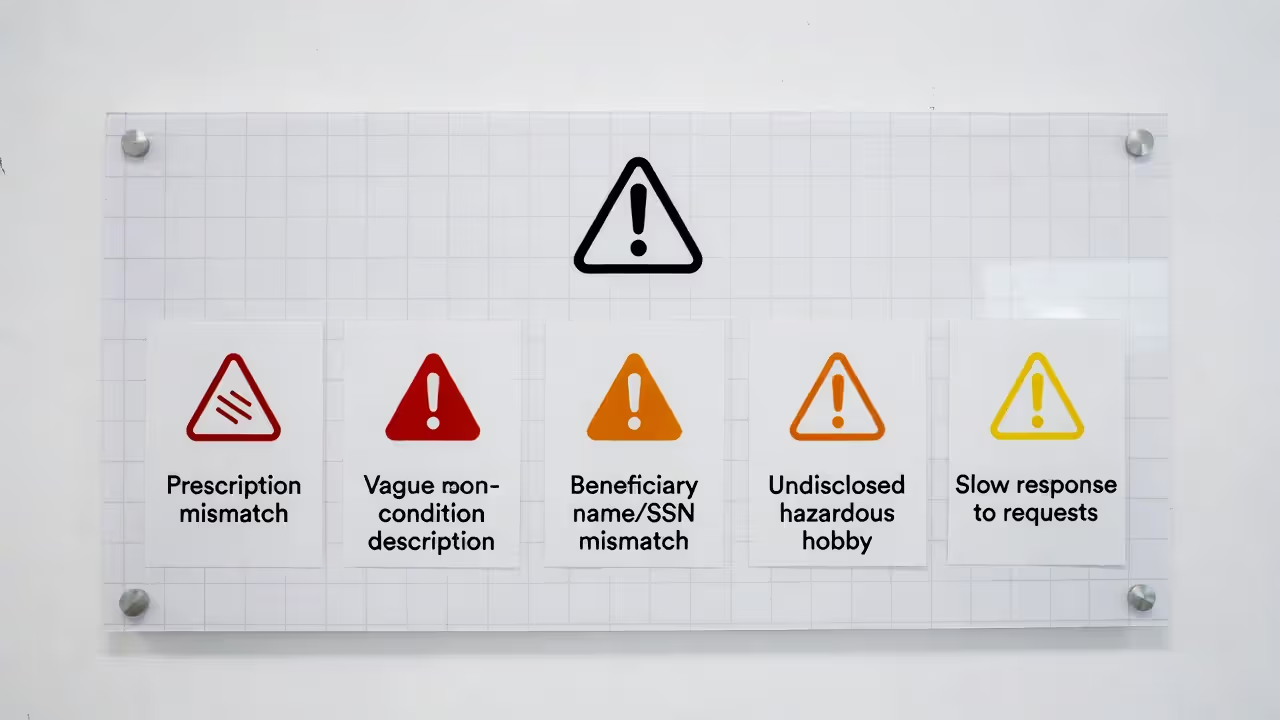

Prescription mismatches top the list. You state you take atorvastatin for cholesterol but forget to mention the lisinopril for blood pressure. The database shows both. Now an underwriter needs to contact you for clarification—adding 3-5 business days to your timeline.

Vague condition descriptions cause similar problems. Saying "I had high blood pressure a few years ago" leaves too many questions unanswered. Is it still present? Controlled with medication? What are your current readings? Better approach: "Diagnosed with hypertension in March 2020, currently controlled with 10mg lisinopril daily, most recent reading was 122/78 at my January physical."

Beneficiary information errors prevent policy finalization. Someone lists their spouse as "Mike Johnson" when his legal name is Michael Robert Johnson Jr. The Social Security number doesn't match the name variation. The policy sits in limbo until this gets corrected.

Undisclosed hobbies create bigger problems. You actively participate in competitive motorcycle racing but don't mention it because the application didn't specifically ask. The insurer discovers this through social media monitoring or background checks. Now there's a trust issue on top of the underwriting concern.

Average Timeline from Start to Decision

Algorithmic approvals happen within minutes to 72 hours for qualifying applicants. The system analyzes your data against risk models built from millions of previous applications and claims. If your profile matches low-risk patterns—think 32-year-old taking only allergy medication with perfect driving records—approval is instantaneous.

Manual review cases take 7-12 business days typically. An underwriter examines your file personally, possibly ordering medical records from your physician's office. This doesn't mean problems—it means your situation needs human judgment that algorithms can't confidently provide. Maybe you're taking a newer medication the system hasn't evaluated enough times to predict risk accurately.

Full traditional underwriting with medical exams extends timelines to 4-6 weeks. You schedule the exam (which might take a week depending on your availability), wait for lab results (another 5-7 days), then wait for underwriter review. If your physician is slow responding to medical record requests, this stretches to 8-10 weeks.

Decisions arrive within these same windows whether you're approved, denied, or offered coverage at higher-than-quoted premiums. Adverse decisions include detailed explanation letters citing the specific factors that affected your rating.

Online Underwriting Basics: What Happens Behind the Scenes

Author: Christopher Baldwin;

Source: everymuslim.net

Underwriters perform one core function: predicting mortality risk. They're calculating the statistical probability that you'll die during the policy period based on every available data point about your health, lifestyle, and background.

You get assigned to risk classifications that directly determine pricing. Preferred Plus represents the healthiest applicants—these are people who might outlive standard life expectancy tables. Preferred comes next, then Standard, then various Substandard ratings that increase premiums based on specific health concerns.

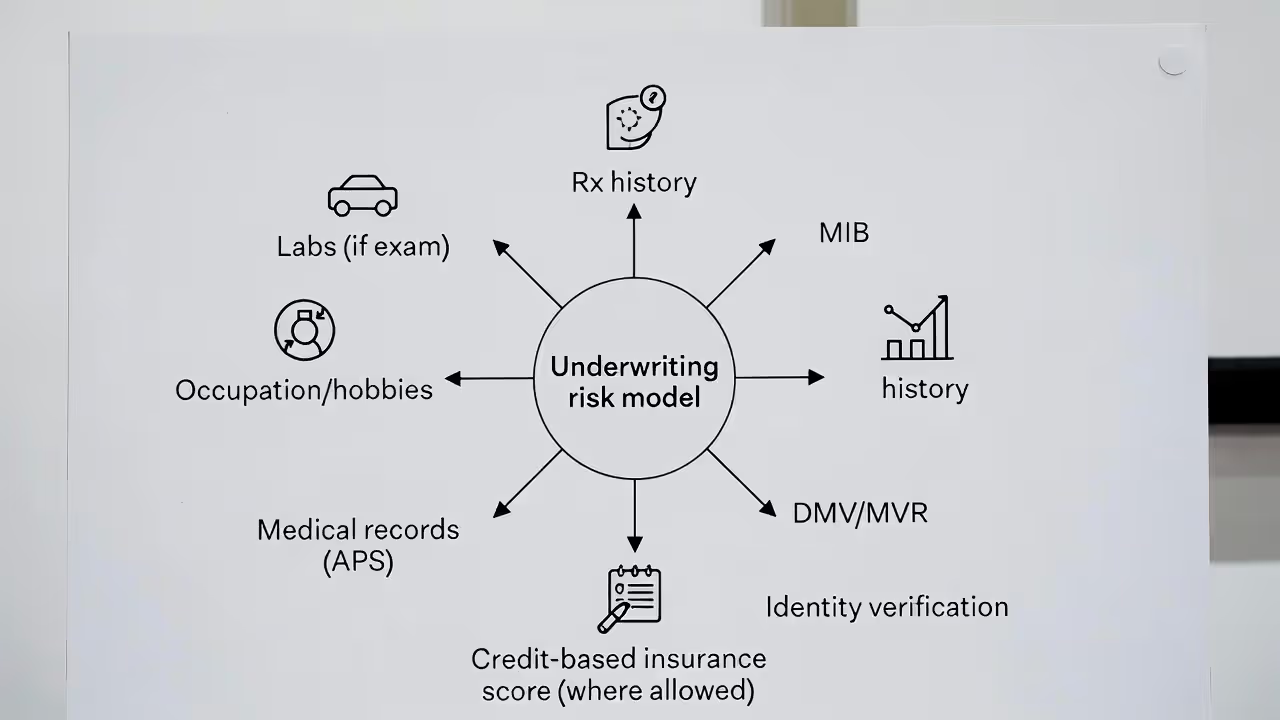

Digital underwriting substitutes third-party data for traditional medical evidence. When you authorize information sharing, carriers immediately query several sources:

Prescription history comes from pharmacy benefit manager databases that track every medication dispensed under your name. The system sees the drug name, strength, quantity, prescribing doctor, and refill pattern. A daily metformin prescription signals diabetes management. Multiple antidepressant fills indicate ongoing mental health treatment. Statin medications point to cholesterol concerns.

Driving records pull from state Department of Motor Vehicle databases. One DUI in the past seven years raises significant red flags because risky behavior patterns correlate with higher mortality rates across large population studies. Multiple speeding tickets matter less than one reckless driving conviction, though three speeding citations in one year still shows concerning patterns.

Medical Information Bureau reports contain coded data from your previous insurance applications across any participating carrier. Applied for disability coverage in 2019 and disclosed your sleep apnea diagnosis? That record exists here. Carriers use this to spot inconsistencies and prevent fraud where applicants "forget" significant conditions.

Insurance scoring models operate in most states, analyzing credit-related data to predict lapse probability and claim patterns. These aren't identical to credit scores—they're specialized algorithms trained on insurance-specific outcomes. Someone with severely damaged credit doesn't automatically get declined, but they might land in Standard rather than Preferred rating classes.

Accelerated underwriting relies on predictive models trained on literally millions of applications and subsequent claims. These algorithms identify low-risk patterns: a 38-year-old taking only thyroid medication, clean driving history, no Medical Information Bureau flags, stable credit patterns, and BMI under 28 presents statistically predictable low mortality risk. The system approves automatically without human review.

Traditional underwriting processes engage when your profile falls outside algorithm confidence boundaries. Perhaps you're taking a medication combination the system has only encountered 200 times—not enough data to predict outcomes confidently. Or your age and requested coverage amount require additional verification regardless of health status. Human underwriters then examine everything manually, often requesting attending physician statements—comprehensive medical records directly from your doctors detailing diagnosis, treatment, prognosis, and current health status.

Medical exams still get required for specific scenarios: coverage amounts exceeding $500,000 in most cases (some carriers use $750,000 or $1 million thresholds), applicants over age 50-55 depending on carrier, or anyone with significant health histories regardless of age or amount. The exam includes venipuncture for blood work, urine specimen collection, blood pressure measurement, height and weight recording, and sometimes EKG monitoring for older applicants or large policies. Laboratory analysis screens for cholesterol levels, glucose readings, liver and kidney function markers, HIV antibodies, nicotine metabolites, and occasionally recreational drug panels.

Setting Realistic Instant Approval Expectations

Author: Christopher Baldwin;

Source: everymuslim.net

When platforms advertise "instant approval," they mean their algorithm made an immediate underwriting decision—not that your policy is already protecting your family. You still need to review documents, sign disclosures, set up payment, and sometimes complete a brief verification call before coverage actually begins.

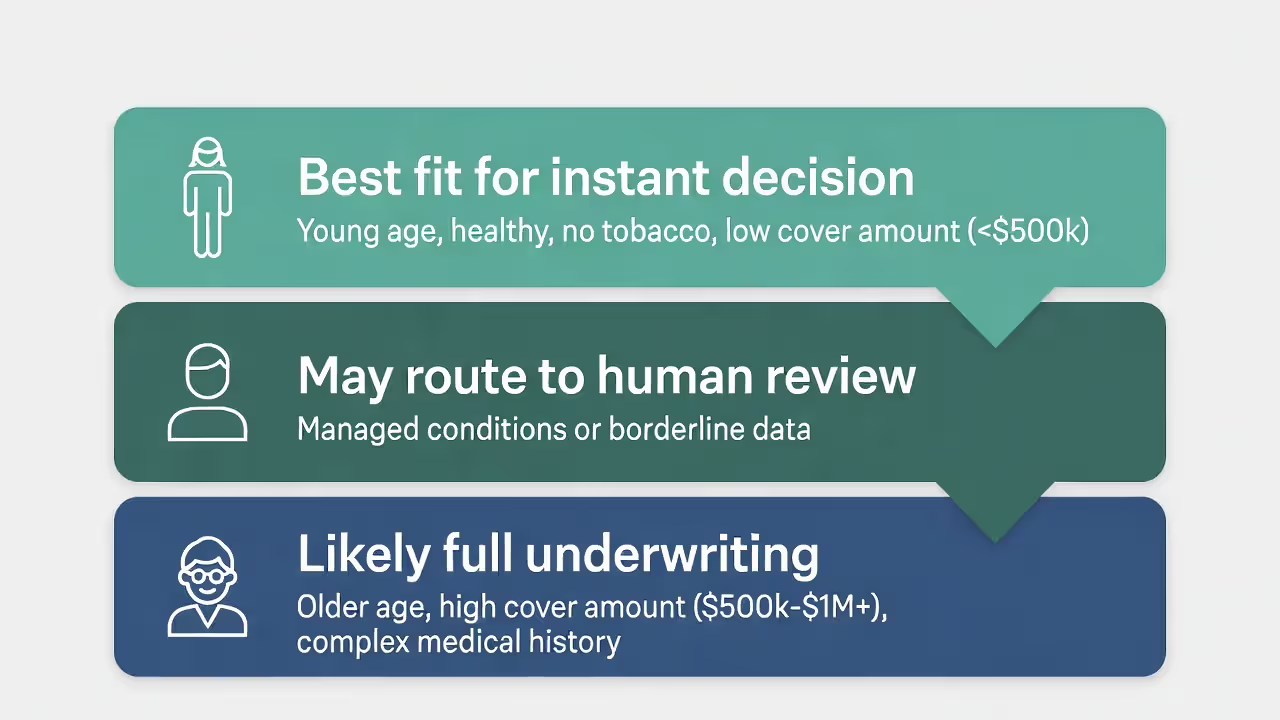

Instant decisions work best for these profiles: - Term life policies with death benefits between $100,000-$500,000 - Applicants between ages 20-45 who are in good health - Non-tobacco users with no significant diagnosed conditions - People in standard occupations without hazardous job duties

Coverage amounts above $500,000 almost universally trigger additional review regardless of how healthy you are. Carriers need to verify insurable interest—legitimate financial justification for that death benefit level. A 29-year-old earning $65,000 annually who requests $2.5 million in coverage will face questions about what makes that amount appropriate. Maybe you've got $1.8 million in business debt personally guaranteed, which justifies the amount. But you need to explain and document that.

Health situations that force manual underwriter review include: - Any form of diabetes, whether Type 1, Type 2, or gestational history - Cancer diagnoses even if you've been in remission for a decade - Cardiovascular disease, previous heart attacks, or stroke history - Chronic kidney disease at any stage - Mental health conditions requiring prescription medications - Diagnosed sleep apnea regardless of CPAP compliance - Body Mass Index calculations above 35 - Hypertension with blood pressure readings consistently above 140/90

You can absolutely still get approved with these conditions—an underwriter just needs to evaluate severity, how well controlled the condition is, treatment adherence, and current health trajectories. Well-managed Type 2 diabetes might only bump you to Standard rates instead of Preferred. Poorly controlled diabetes with A1C levels above 8.5 could mean Substandard ratings or even temporary postponements until you demonstrate better management.

| Application Method | Timeline to Decision | Maximum Coverage | Health Profile Needed | Medical Exam |

| Instant algorithmic approval | Same day to 24 hours | Usually caps at $500,000 | Excellent health, minimal medical history, younger applicants | Not required |

| Accelerated digital underwriting | 5-12 business days | Up to $1 million typically | Good health, some managed conditions acceptable | Not required |

| Traditional full underwriting | 4-6 weeks average | No upper limits | All health profiles including complex cases | Required for most |

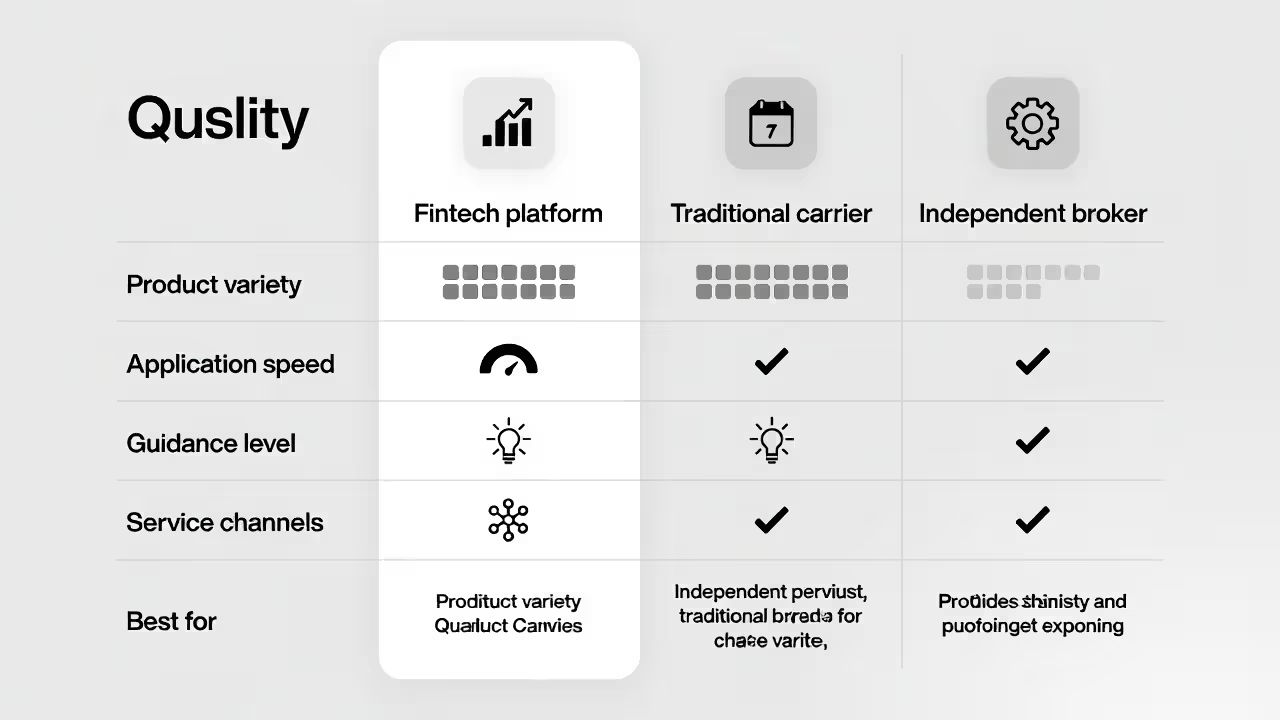

Evaluating Fintech Insurance Platforms vs. Traditional Carriers

Author: Christopher Baldwin;

Source: everymuslim.net

Fintech startups like Ladder, Ethos, and Bestow built their entire technology infrastructure specifically for fast digital applications. They designed mobile-first experiences from day one. Traditional carriers such as Northwestern Mutual, State Farm, and New York Life have bolted digital capabilities onto existing systems built over decades.

| Comparison Factor | Fintech Startup Platforms | Established Traditional Carriers | Independent Broker Services |

| Application completion time | 15-30 minutes typical | 25-50 minutes typical | 45-75 minutes including consultation time |

| Customer service channels | Primarily chat and email support, limited phone access | Multiple phone lines, email, in-person agent meetings | Direct relationship with your specific agent |

| Available policy types | Almost exclusively term life, limited customization | Term, whole life, universal, variable, and specialized products | Access to products from many different carriers |

| Price comparison transparency | Instant quotes displayed clearly | Often requires speaking with agent for accurate quotes | Can provide quotes from multiple companies |

| Educational materials | Digital guides, calculators, FAQ sections | Comprehensive materials, in-person seminars, workshops | Personalized advice specific to your situation |

Fintech platforms shine when you need straightforward term coverage and know exactly what you're looking for. The application flows smoothly on mobile devices, pricing appears upfront without phone calls, and you complete everything without human interaction if you prefer. Customer service exists but feels more like contacting Amazon support than consulting with a financial advisor.

These platforms make perfect sense when your needs are uncomplicated: a 28-year-old wants $300,000 in 20-year term coverage to protect their mortgage and young children's future expenses. You compare several quotes in ten minutes, apply through the best option, and have coverage by tomorrow.

Traditional carriers offer significantly more product variety and complexity. Want permanent life insurance that builds cash value you can borrow against? Need dividend-paying whole life for estate planning purposes? Looking for variable universal life policies where cash value gets invested in market subaccounts? You need a traditional carrier for these. Their agents provide education about products most consumers have never heard of, though this obviously comes with potential sales pressure toward higher-commission products.

The agent relationship becomes increasingly important as your financial situation grows more complex. A 53-year-old business owner exploring key person insurance, buy-sell agreement funding, executive bonus arrangements, and wealth transfer strategies needs sophisticated guidance that chatbots simply cannot provide. They need someone who understands business succession planning and estate tax implications.

Independent brokers access multiple carriers simultaneously, essentially shopping your application to whichever insurer offers optimal combinations of pricing and underwriting standards for your specific profile. Someone with well-managed diabetes might get declined by Carrier A, offered coverage at inflated Substandard rates by Carrier B, but approved at Standard rates by Carrier C. Experienced brokers know these carrier-specific underwriting philosophies.

The fundamental trade-off: speed and simplicity versus comprehensive guidance and extensive options. Neither approach objectively beats the other—the right choice depends entirely on your situation's complexity and your comfort level navigating options independently.

Online Safety Tips: Protecting Your Information During the Application

Life insurance applications demand highly sensitive personal information: Social Security numbers, complete medical histories, detailed financial data, and beneficiary identification details. This data concentration creates attractive targets for identity thieves and insurance fraudsters.

Begin by confirming platform legitimacy before entering any personal details. Every state maintains insurance department websites with searchable databases of licensed carriers and agents. California's Department of Insurance website, for instance, includes a licensee lookup tool where you can verify company and agent credentials instantly. New York's DFS website offers similar functionality. Use these official resources.

Legitimate insurance companies possess unique identification codes assigned by regulatory bodies. These company codes appear in public regulatory databases and on official correspondence. If a platform claims representation of a specific carrier but you can't locate that carrier name in regulatory databases, stop the application immediately.

Before sharing medical records or Social Security information with any insurance website, verify through your state's insurance department that they're either a licensed carrier operating in your state or a properly licensed agent representing a legitimate company. Check these official databases, not just Google searches. When you encounter aggressive sales pressure, requests for unusual payment methods, or evasive answers about licensing details, listen to your instincts and discontinue the process.

— Amy Bach, Executive Director of United Policyholders

Encrypted data connections show through several browser indicators. Website addresses beginning with "https://" include the crucial "s" denoting secure encryption. Modern browsers display padlock symbols in the address bar near the URL. Click that padlock to view the security certificate, which should be issued specifically to the company you believe you're dealing with, not some generic hosting service.

Legitimate insurance platforms will never request: - Payment through wire transfers, cryptocurrency, or retail gift cards - Your actual bank account passwords or ATM PIN numbers - Premium payments before you've received and reviewed policy documents - Social Security numbers before you've made a conscious decision to formally apply

Warning signs indicating potential fraud operations: - High-pressure tactics claiming rates expire within hours - Quotes substantially lower than competitors without reasonable explanation - Obvious grammatical errors and spelling mistakes in official communications - Contact options limited to web forms with no verifiable phone numbers or physical addresses - Requests to sign blank forms or documents with information sections left empty - Unsolicited contact claiming you've been "pre-approved" when you never applied

Review privacy policies before authorizing any information sharing. Legitimate carriers publish detailed policies explaining what data they collect, how they use that data, which third parties receive access, and how you can review or correct your information. The policy should specify security measures like encryption standards and access controls protecting your stored data.

After completing your application, monitor both credit reports and medical records proactively. Federal law entitles you to one free credit report annually from each of the three major bureaus through the official AnnualCreditReport.com website (not the commercial imposter sites). The Medical Information Bureau provides one free annual disclosure through their website at mib.com. Check these reports for unfamiliar inquiries or applications you didn't authorize.

If you suspect fraudulent activity, immediately report to your state insurance department, which investigates consumer complaints and can take enforcement action against fraudulent operators. Also file reports with the Federal Trade Commission through their website or hotline. Consider placing fraud alerts or security freezes on your credit files through each credit bureau to prevent unauthorized account openings.

FAQ: Common Questions About Buying Life Insurance Online

The digital transformation of life insurance buying has genuinely improved outcomes for many consumers. Healthy applicants seeking straightforward term coverage can complete applications during lunch breaks and receive same-day decisions. No more coordinating exam appointments that conflict with work schedules or sitting through hour-long presentations when you just want a simple policy.

But digital convenience doesn't mean every application belongs online. Complex health backgrounds benefit enormously from broker expertise and knowledge about which carriers underwrite specific conditions most favorably. Coverage amounts above $1 million require documentation and verification that automated systems can't adequately evaluate. Permanent life insurance products involve features, trade-offs, and tax implications that deserve thorough explanation from professionals who can answer follow-up questions in real time.

The key is honestly assessing which approach matches your specific situation. If you're 33, healthy, non-smoker wanting $400,000 in term coverage, fintech platforms probably make perfect sense. If you're 57 with treated high blood pressure seeking $1.8 million in coverage, expect traditional underwriting with medical exams and human review regardless of platform.

Whichever path you choose, verify platform legitimacy before sharing personal information. Confirm state licensing through official insurance department websites, read privacy policies carefully, and trust your instincts when something feels questionable. The convenience of digital applications should never compromise security or result in inappropriate coverage.

Begin by calculating how much coverage your family actually needs and for what time period. Online calculators help estimate appropriate death benefits based on your income, outstanding debts, and dependents' future needs. Then gather quotes from multiple sources—fintech platforms, traditional carriers, and independent brokers—to compare both pricing and application requirements for your profile. The most valuable life insurance buying guide is one that helps you understand your options clearly and choose confidently based on your particular circumstances.