Life Insurance: Which Policy Type Fits Your Needs?

Group vs Individual Life Insurance Guide

Content

Most people first encounter life insurance through a job offer packet, sandwiched between 401(k) enrollment forms and health plan options. That employer coverage feels automatic and easy—but it's rarely the whole story when protecting your family's financial future.

What Makes Group and Individual Life Insurance Different?

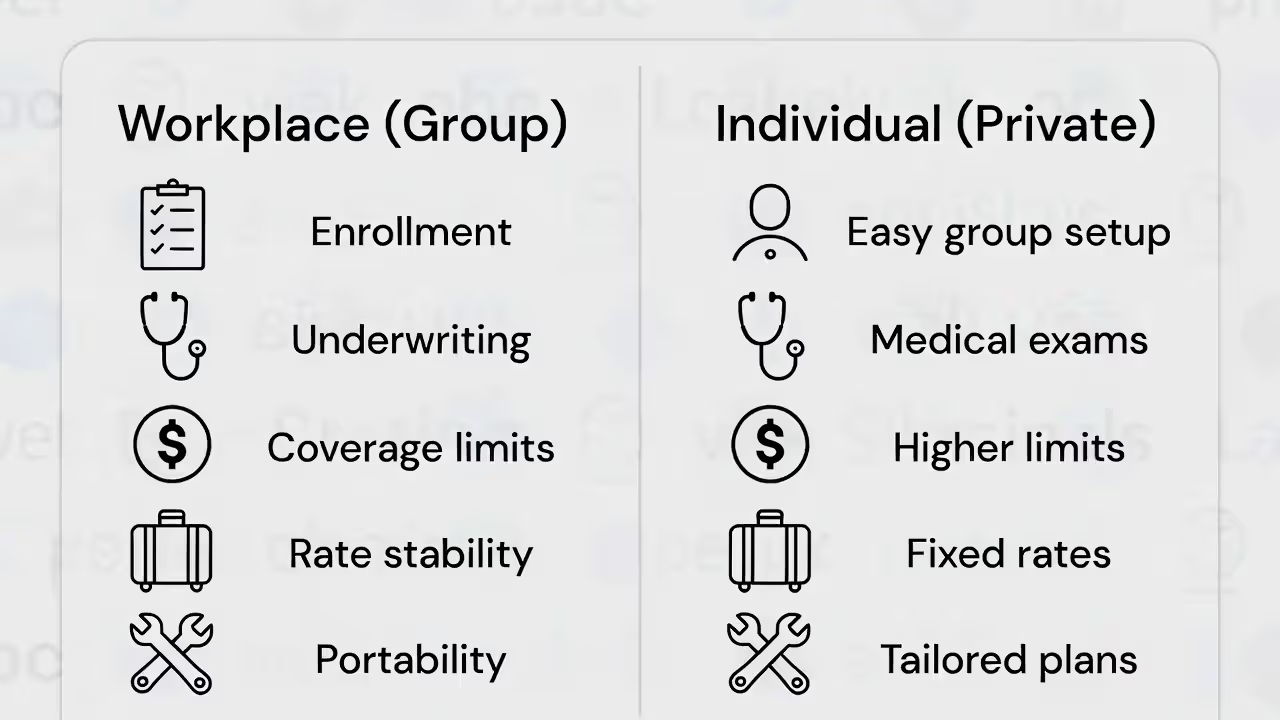

Your employer partners with an insurance company to create one blanket policy covering everyone who works there. That's group life insurance. During your first 30 days on the job, you'll usually qualify for some basic amount—maybe $50,000 or one year's salary—without proving you're healthy. No blood draws, no questions about your cholesterol or whether you've been skydiving lately.

Buying your own policy works differently. You contact an insurer or agent yourself, fill out applications asking about everything from your blood pressure to your family's medical history, and usually submit to a medical exam. Once approved, you're the policyholder. The contract belongs to you. Your employer never enters the equation.

Here's what really separates these two: who signs the actual insurance contract. When coverage comes through work, your boss's company holds the master policy. You get a certificate showing you're covered under that umbrella. But with a policy you purchase yourself, your name appears on the contract as the owner. That distinction affects nearly everything else—what happens when you switch jobs, whether you can modify coverage, and how much you'll ultimately pay.

Industry surveys show about 60% of American workers can access some employer-sponsored coverage. Many stop there, figuring they're set. The problem? Those workplace policies typically max out between one and three times your annual salary—often nowhere near the financial cushion experts recommend for families with mortgages, kids, and long-term obligations.

| Feature | Group/Workplace Coverage | Individual/Private Coverage |

| Cost | Company subsidizes premiums; basic tier often free | You cover the full premium based on your age and health profile |

| Medical exam required | Generally waived for initial enrollment period | Expected for most coverage levels above $250,000 |

| Coverage amount | Capped at 1-3x salary, frequently maxing under $500,000 | Customizable from $100,000 to several million if you qualify |

| Portability | Disappears when you leave the job (conversion sometimes possible) | Travels with you through any career change |

| Ownership | Company holds the master contract | You're the policy owner |

| Customization options | Standardized package with few modifications | Extensive menu of riders and features |

| Duration | Lasts only during your employment | Renewable through age 95-121 depending on terms |

| Beneficiary control | You name beneficiaries but can't alter policy foundation | Complete authority over all policy elements |

How Workplace Coverage Compares to Private Policies

Author: Michael Stanton;

Source: everymuslim.net

Cost Structure and Premium Differences

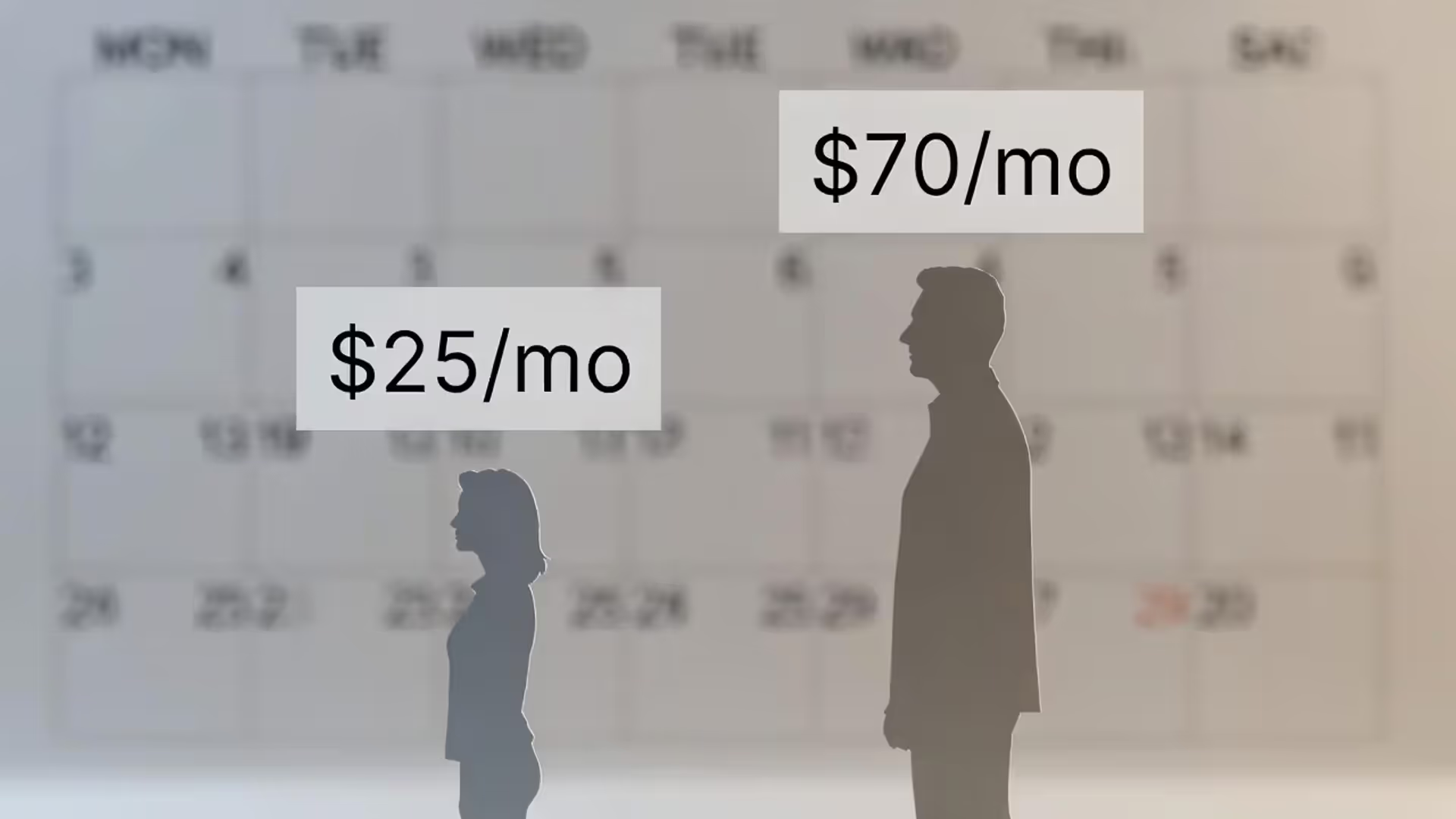

Your paycheck stub might show zero deductions for life insurance because your employer picks up the tab for basic coverage. That appears to be free money—and in one sense, it is. But once you want more than that base amount, you'll pay extra through payroll deductions. Those supplemental premiums use group pricing that seems reasonable until you compare it against what you'd pay elsewhere.

Group pricing averages everyone's risk together. The 28-year-old who runs half-marathons pays similar rates as the 55-year-old who smokes. If you fall into that healthy, young category, you're essentially overpaying to balance out higher-risk colleagues. I've seen healthy 35-year-olds quoted $40 monthly for $500,000 in coverage through individual underwriting—while their employer's supplemental group rate for the same amount ran closer to $75.

Another wrinkle: your company renegotiates that group contract every few years. Premiums can spike if the employee population ages or several large claims hit the plan. Individual term policies lock your rate for 10, 20, or 30 years. Permanent policies guarantee premiums for life. You won't wake up to a surprise increase because your company's demographics shifted.

Medical Underwriting Requirements

Workplace plans shine brightest during those first weeks on the job. Sign up within your eligibility window—usually 31 days from your start date—and you'll get guaranteed issue coverage up to a certain amount. Recent cancer diagnosis? Diabetes? Dangerous hobbies? Doesn't matter. You're approved automatically, typically for $50,000 to $150,000 depending on your employer's plan design.

Purchasing your own policy means answering 20+ pages of health questions, authorizing your doctor to release medical records, and likely scheduling a paramedical exam at your kitchen table. A nurse draws blood, takes urine samples, records your height and weight, and checks your blood pressure. Approval usually comes back in four to six weeks, though accelerated underwriting through some carriers can deliver decisions within 48 hours for healthy applicants requesting moderate coverage amounts.

But here's the upside of underwriting: exceptional health earns you exceptional rates. Insurers categorize approved applicants into preferred plus, preferred, standard plus, and standard tiers. That healthy marathon runner might land in preferred plus, paying 40% less than someone in standard health. Your workplace never rewards your good habits with lower premiums—you're priced with the group average regardless.

Coverage Amounts and Policy Limits You Should Know

Check your employee benefits handbook. Most workplace policies cap death benefits at two or three times your salary, with company-wide maximums between $250,000 and $500,000. Some generous employers push that higher, but it remains tethered to your paycheck. Pull in $80,000 annually? Your maximum group coverage might be $240,000—enough to cover about five years of lost income before factoring in any other expenses.

Financial planners typically recommend coverage equal to 10 to 15 times your annual earnings, adjusted for your specific situation. Got a $450,000 mortgage, two kids heading toward college, and a spouse who stayed home to raise them? You probably need $1.5 million or more in coverage. Three times your salary won't cut it.

Individual policies let you dial in the precise amount your family requires. Apply for $2 million if you need it and can demonstrate the financial justification. Insurers verify you're not buying more coverage than your income and assets reasonably support, but those limits stretch much further than workplace restrictions.

Watch out for another workplace policy quirk: age-based reductions. Many employer plans automatically slash your death benefit by 35% when you turn 65, then cut it again at 70. You're losing protection precisely when you might still carry debt or want to leave a legacy for grandchildren. Individual policies maintain full face value for the entire contract term—or your entire life with permanent coverage.

What Happens When You Change Jobs: Portability Explained

Author: Michael Stanton;

Source: everymuslim.net

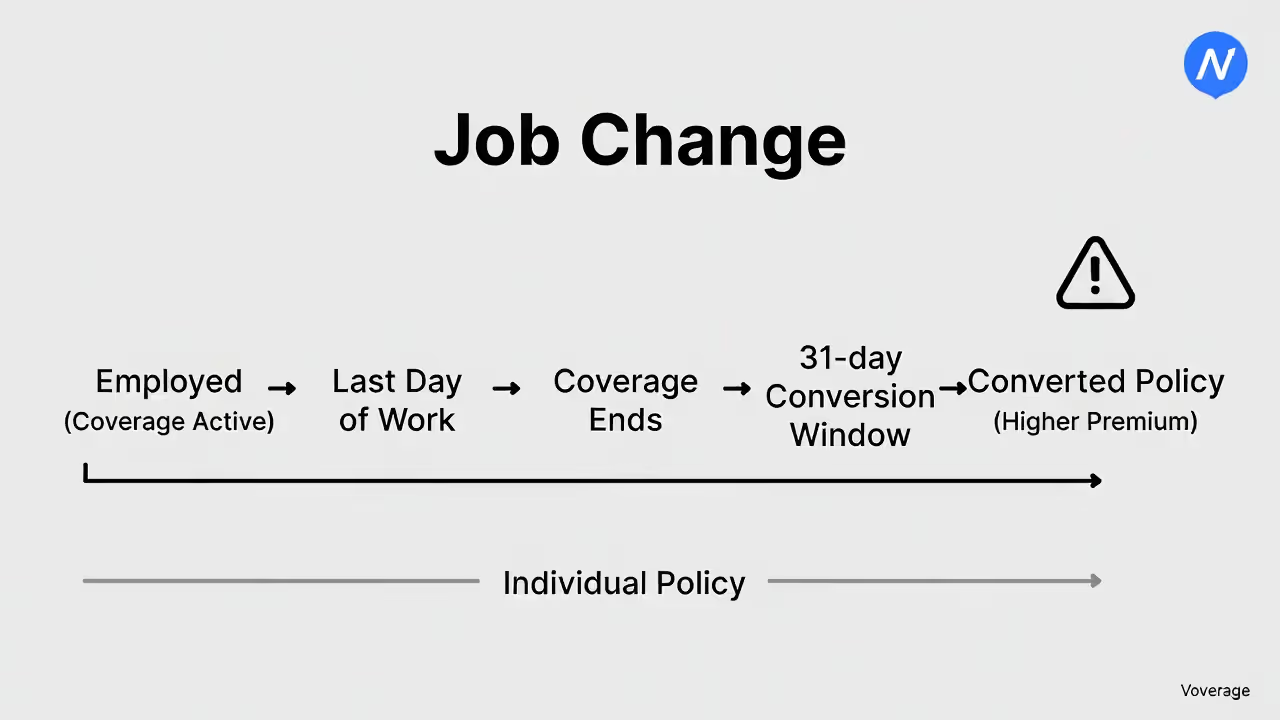

Americans switch employers every four years on average now. Each time you give two weeks' notice, your group life insurance clock starts ticking toward termination. Coverage typically ends your last day of work or possibly at month's end if your company's generous.

Some workplace policies include conversion privileges—you get 31 days after termination to convert your group coverage into an individual policy without answering any health questions. Sounds perfect until you see the price tag. Conversion policies assume you're converting because you're uninsurable elsewhere. Expect premiums running 200% to 400% higher than standard rates. That $250,000 in coverage might suddenly cost $450 monthly for a 48-year-old, compared to maybe $175 monthly if you applied for a new policy with underwriting.

The real danger surfaces when health changes while you're relying solely on employer coverage. Picture this: you work somewhere for 12 years, comfortable with your workplace policy. At age 47, your doctor diagnoses type 2 diabetes and high blood pressure. Now you want your own policy but discover applications either get declined or come back with premiums triple what you'd have paid five years earlier. You've aged and developed conditions that make affordable individual coverage nearly impossible—all while depending on protection that vanishes the day you leave your job.

Policies you own yourself eliminate this entire problem. Get laid off, fired, start consulting, launch a business, retire at 55—your coverage continues without interruption. Instead of payroll deduction, premiums draft from your checking account. But the protection stays locked in at the rate you secured when you were younger and healthier.

I've watched too many professionals in their 30s and 40s lean entirely on workplace coverage, then receive a diagnosis that makes them uninsurable on the individual market. By the time they grasp that group insurance doesn't follow them, their window for affordable portable protection has slammed shut.

— Michael Chen

Who Actually Owns Your Policy and Why It Matters

Ownership equals control. Your employer owns the master policy and can modify terms, switch insurance carriers, or cancel coverage entirely. You receive a certificate of insurance—basically a receipt proving you're covered under their contract. But you can't alter the policy's structure, tack on additional riders, or guarantee it continues beyond your employment tenure.

This creates real vulnerability. Your company gets acquired? The new ownership might offer worse coverage or none at all. Your employer faces budget constraints? They might slash benefits or eliminate voluntary coverage tiers. You have zero input into these decisions because you're not the policyholder.

Individual ownership hands you complete control. You designate and modify beneficiaries whenever you want, without routing paperwork through HR or getting anyone's permission. Need to change beneficiaries after a divorce and remarriage? That's between you and your insurance company. Your employer never appears in the conversation.

Beneficiary control becomes critical in blended families or complex situations. Workplace policies let you name beneficiaries, but some companies require spousal consent before you can designate anyone else as primary beneficiary. Your own policy lets you split benefits between children from a previous marriage, establish a special needs trust, name a charity, or create any arrangement that fits your situation—all privately, without workplace administrators involved.

For business owners and high-net-worth families, individual ownership enables sophisticated estate planning strategies. You can position policies inside irrevocable trusts, use them to fund buy-sell agreements, or create liquidity for estate taxes. These advanced planning techniques simply don't work with employer-sponsored coverage because you lack the ownership rights needed to execute them.

Flexibility to Adjust Your Coverage Over Time

Author: Michael Stanton;

Source: everymuslim.net

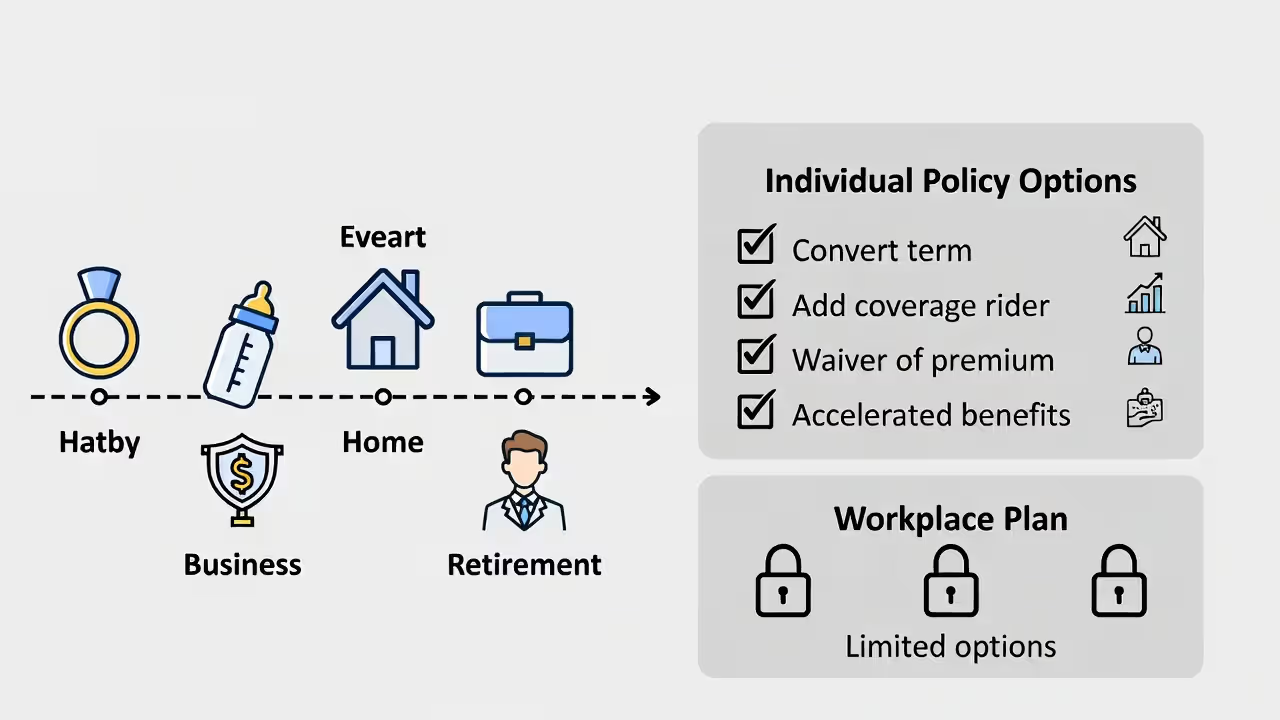

Life rarely stays static. You marry, divorce, have kids, buy houses, start businesses, send children to college, approach retirement. Individual policies adapt through riders and options that workplace plans almost never include.

Consider these common individual policy features:

- Term conversion riders let you switch from term to permanent insurance later without proving insurability again—critical if you develop health problems

- Guaranteed insurability riders allow purchasing additional coverage at specific life events regardless of health changes that occurred since you bought the original policy

- Accelerated death benefit riders provide early access to your death benefit if you're diagnosed with a terminal or chronic illness

- Disability waiver of premium keeps your policy active without requiring payments if you become disabled and can't work

Workplace coverage typically offers none of this customization. You get the standard package—take it or leave it. Some employers add options like supplemental accidental death coverage or small policies for dependents, but these pale compared to individual policy flexibility.

Permanent individual policies accumulate cash value you can tap through loans or withdrawals. Universal and whole life policies let you adjust both death benefits and premiums within contract limits, giving you financial breathing room during tight years. Variable universal life offers investment subaccounts that could potentially grow your cash value faster.

Group coverage delivers a fixed death benefit with zero cash accumulation. You can't borrow against it, adjust it based on changing needs, or use it as any kind of financial asset. When you leave your employer, every dollar you paid through payroll deduction is gone—you've essentially rented coverage rather than building an asset you own.

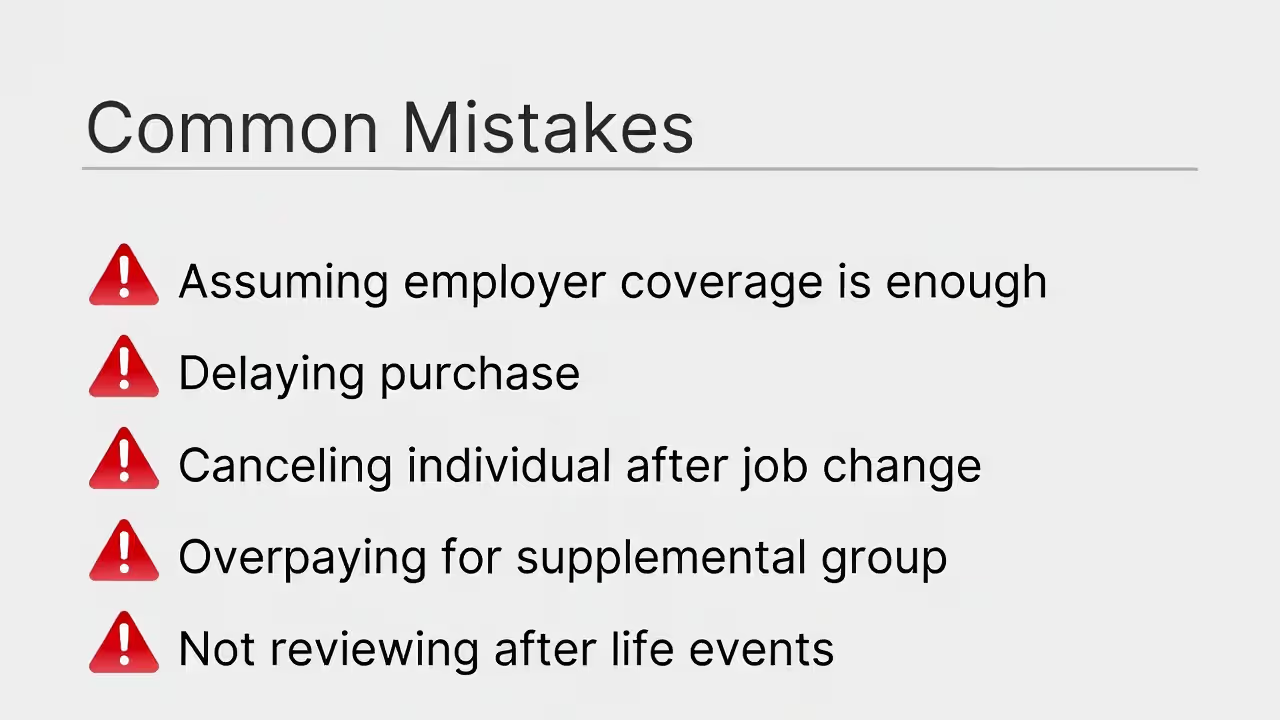

Common Mistakes When Choosing Between Group and Individual Coverage

Author: Michael Stanton;

Source: everymuslim.net

The costliest error? Assuming your employer's coverage handles everything. That $150,000 workplace policy feels substantial until you actually calculate needs. Subtract your mortgage balance. Add college costs for two or three kids. Estimate ten years of income replacement. Include final expenses. Most families land between $500,000 and $1.5 million in actual protection needs—multiples beyond typical workplace limits.

Plenty of people postpone buying their own coverage, planning to "get around to it eventually" after the next promotion or when their budget loosens up. Meanwhile they age into higher premium brackets and risk developing health conditions that either spike costs or kill insurability completely. A 32-year-old pays roughly 60% less than someone age 42 for identical coverage. Every birthday that passes costs you money.

Another expensive mistake: canceling individual coverage after landing a new job with better group benefits. You've already passed underwriting and locked in rates based on your younger, healthier self. Surrendering that policy for group coverage that disappears with your next career move wastes the insurability you've already secured. Keep that individual policy and treat workplace coverage as a bonus.

Some workers max out supplemental group coverage thinking they're capitalizing on group discounts. For healthy people, those group rates frequently exceed what individual term insurance would cost, while offering far less portability and flexibility. Calculate both options before assuming the workplace deal is better.

Failing to reassess coverage during major life transitions creates dangerous gaps. You get married—your new spouse assumes your work policy covers both of you. It doesn't. You have a baby—that $100,000 workplace policy suddenly looks inadequate for a family of three. You buy a $550,000 house—your group coverage wouldn't even satisfy the mortgage balance.

Frequently Asked Questions About Group and Individual Life Insurance

Group versus individual coverage isn't really an either-or choice for most families. Your employer's basic life insurance delivers immediate protection—often at zero cost—that absolutely makes sense to accept. But treating workplace coverage as your complete answer leaves your family exposed to coverage gaps when you change jobs, retire, or face health changes that make individual policies unaffordable or unavailable.

Securing your own policy while you're young and healthy locks in affordable rates and guaranteed coverage that follows you throughout your entire career. You control the contract, select the coverage amount your family genuinely needs, and sidestep all the portability problems that make group coverage unreliable for long-term planning.

Calculate what your family truly requires using honest estimates for income replacement, debt elimination, and future expenses like college funding. Compare that figure to your workplace coverage limits. The difference between what you've got and what you need determines how much individual coverage you should pursue.

Begin the individual policy application process sooner than later. Each birthday pushes your premium higher, and unexpected health changes can make coverage costlier or impossible to get. The ideal time to secure life insurance hits when you don't think you need it yet—when you're healthy, insurable, and can lock in the lowest possible rates for decades of protection ahead.