Life insurance quote comparison on a laptop with a checklist for coverage, term length, and carrier rating.

How to Compare Life Insurance Policies?

Content

Most people treat life insurance like a one-and-done purchase—sign on the dotted line, file the papers away, and assume everything's sorted. That's a costly mistake.

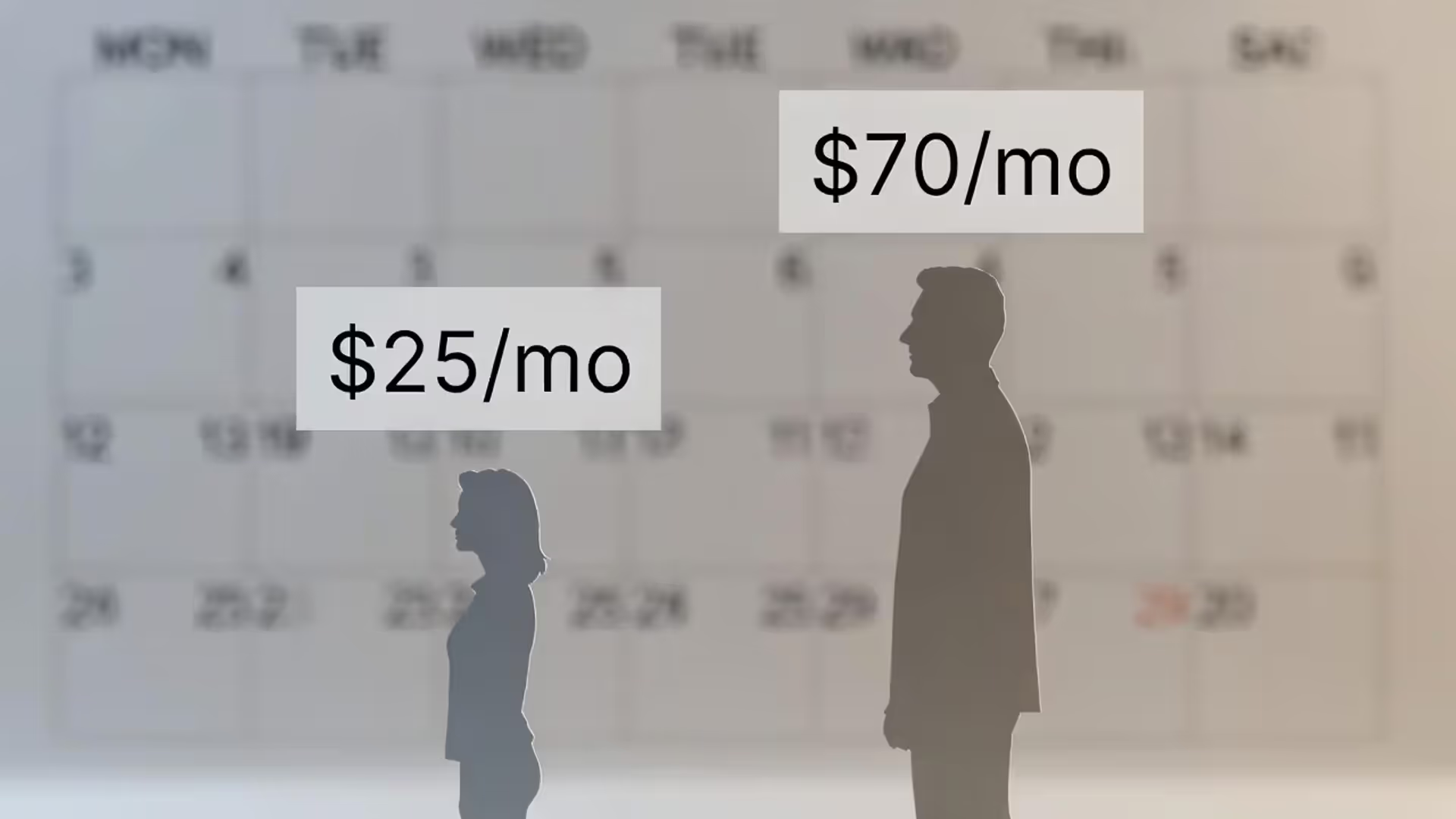

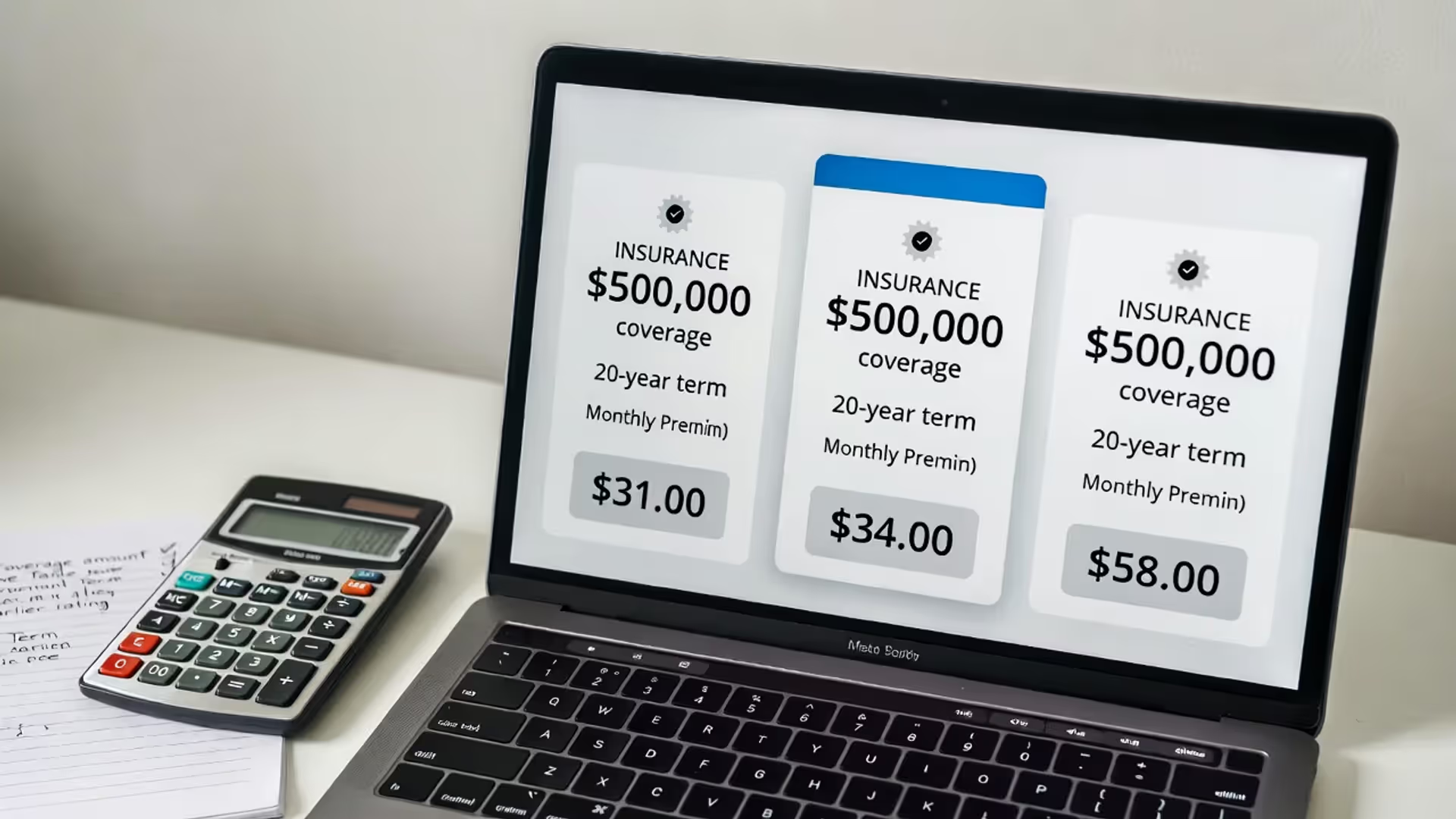

Here's what I mean: my neighbor Tom bought a $500,000 policy from the first agent who called him. Paid $58 monthly. Didn't shop around. Turns out, three other carriers would've given him identical coverage for $31-$37 per month. Over his 30-year term, Tom's throwing away roughly $7,560. That's a decent used car he'll never drive.

The price isn't even the scary part. Some policies look bulletproof until you crack open the fine print and discover they won't pay out if you die while traveling to certain countries. Or they cap payouts for specific causes of death. Or they've stretched the contestability period (when insurers can investigate your application) from the standard two years to three or four.

Then there's the opposite problem—buying more coverage than you actually need. I've seen clients paying $200 monthly for permanent policies when a $45 term policy would've handled their needs perfectly. The cash value growth sounded attractive during the sales pitch, but they're now struggling to keep up with payments.

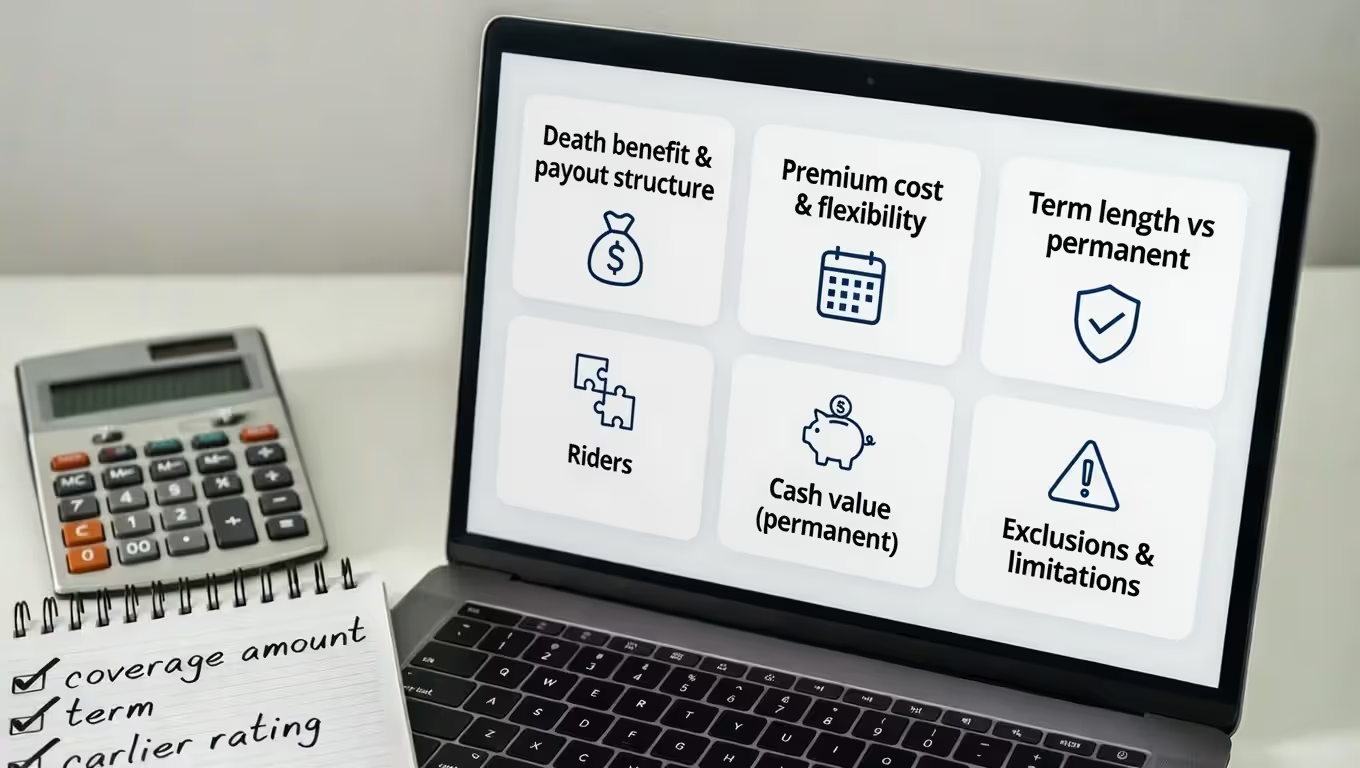

What's the real goal here? Match the right coverage amount, the right policy type, and a rock-solid insurance company to your actual situation. Your health today. Your debts. Who depends on your income. How much risk keeps you up at night.

6 Essential Policy Features You Must Compare

Author: Christopher Baldwin;

Source: everymuslim.net

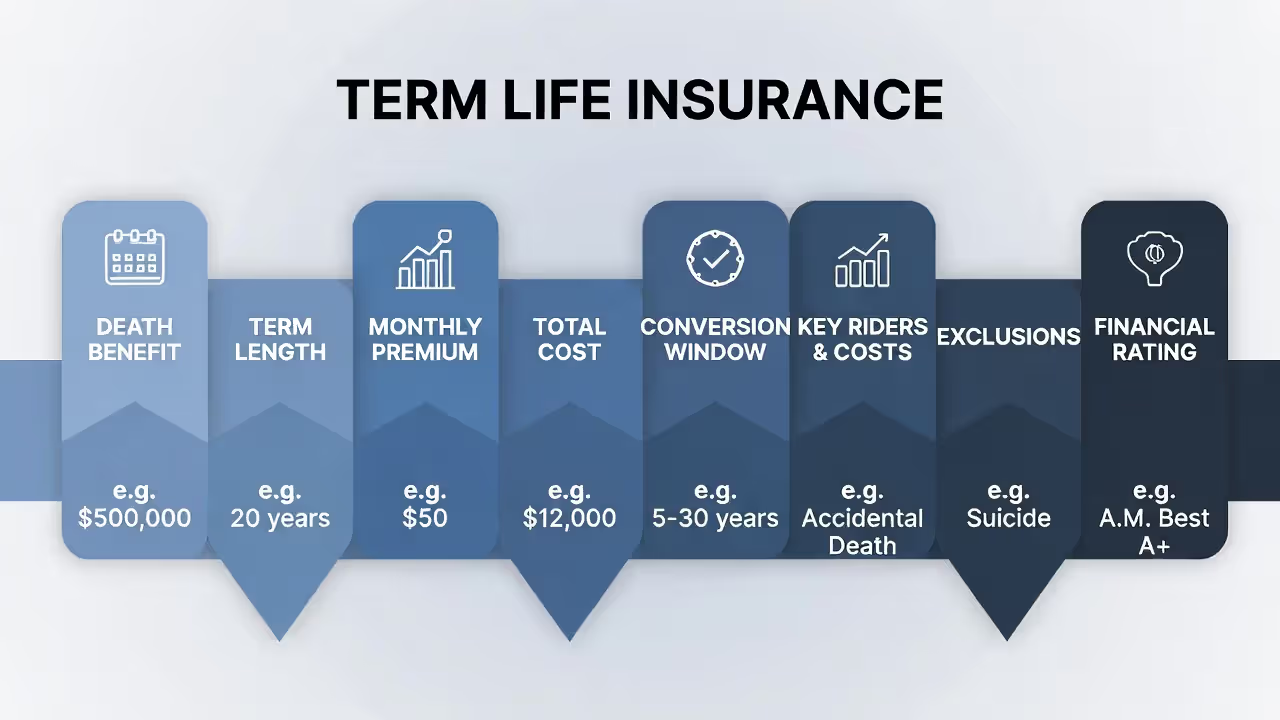

Death Benefit Amount and Payout Structure

Every life insurance policy promises to pay your beneficiaries when you die, but how they pay varies wildly.

Some policies pay the full death benefit immediately after the contestability period—usually two years. Others use graded death benefits, meaning if you die in year one, your family gets back premiums plus maybe 10% interest. Die in year two, perhaps 50% of the face value. Full payout doesn't kick in until year three.

You'll encounter three basic structures:

Level benefits stay constant. You buy $500,000, your beneficiaries get $500,000 (assuming you're past contestability).

Increasing benefits grow over time, usually tied to cash value growth in whole life or universal life policies. Your $300,000 policy might be worth $350,000 after fifteen years.

Decreasing benefits shrink systematically—common in mortgage protection insurance. You start with $400,000 in coverage that drops to $200,000 after fifteen years, matching your declining mortgage balance.

Which makes sense depends entirely on what you're protecting. Got young kids? You want level or increasing coverage—your obligations aren't shrinking anytime soon. Covering a specific debt that decreases over time? Declining benefits with lower premiums might work.

Don't skip the settlement options either. Some insurers only offer lump sums. Others let beneficiaries choose installment payments over 5, 10, or 20 years. Or leave the money with the insurance company earning interest while taking withdrawals as needed. Families without financial experience often benefit from structured payouts—prevents blowing through $500,000 in eighteen months.

Premium Costs and Payment Flexibility

Insurance premiums aren't as straightforward as they appear in advertisements.

Fixed premiums never change. Your payment in year twenty-three matches year one. Period. Most term life and whole life policies work this way.

Flexible premiums let you adjust payments within certain limits. Universal life policies typically offer this feature. Sounds great until you realize that consistently underpaying the recommended amount can cause your policy to implode—coverage ends, and you've got nothing to show for years of payments.

Look beyond the monthly number. Calculate the total outlay. A $40/month policy maintained for thirty years means you've paid $14,400. When comparing term policies, check whether you can convert to permanent coverage later without taking another medical exam. This conversion privilege can save you thousands if you develop diabetes or heart disease and need permanent coverage.

Payment frequency matters more than you'd think. Paying annually instead of monthly usually costs less—sometimes $30-$50 less per year than twelve monthly payments combined. Many insurers discount premiums if you set up automatic bank withdrawals. Others tack on administrative fees. A $50 yearly fee doesn't sound terrible until you realize it's a 10% surcharge on a $500 annual premium.

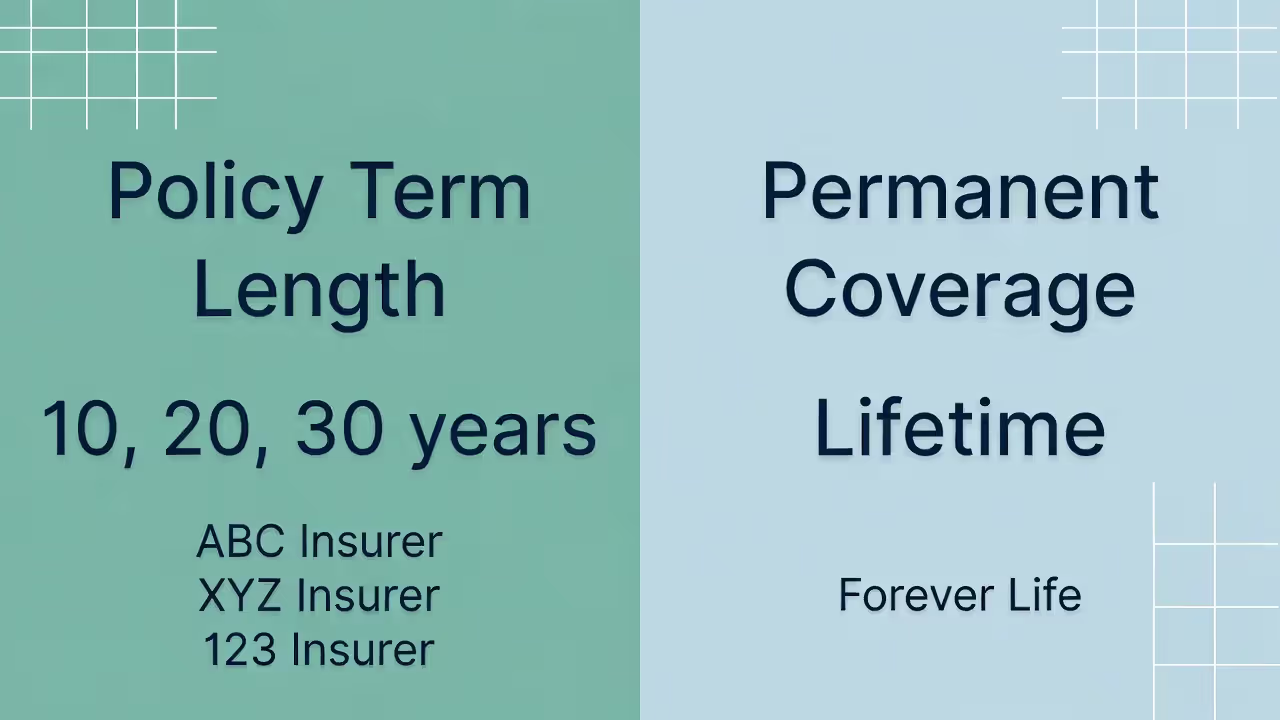

Policy Term Length vs. Permanent Coverage

Author: Christopher Baldwin;

Source: everymuslim.net

This decision splits your path into two completely different directions.

Term policies protect you for specific timeframes—10, 15, 20, or 30 years—then they're done. Zero cash value. Nothing. Permanent coverage (whole life, universal life, variable life) continues until you die, as long as you keep paying premiums.

The cost difference is dramatic. I just ran quotes for a healthy 35-year-old woman. Twenty-year term with $500,000 coverage: $28 monthly. Whole life with identical death benefit: $347 monthly. The term policy delivers nothing if she lives past 55. The whole life policy builds cash value and guarantees a payout eventually.

How do you choose? Match the coverage timeframe to your actual protection needs.

Need coverage until your kids finish college and your mortgage is paid off? That's probably 20-25 years. Term insurance makes financial sense. Why pay $347 monthly when $28 accomplishes your goal?

Planning estate transfers, guaranteeing burial costs regardless of when you die, or want forced savings discipline? Permanent coverage deserves consideration despite costing more.

Riders and Customization Options

Riders modify your base policy, adding features for extra money (sometimes free).

What's frustrating: rider availability and pricing fluctuates dramatically between insurance companies. This is where policy feature comparison gets granular.

Terminal illness riders let you access death benefit money early if doctors diagnose you with something that'll kill you within 12-24 months (timeframes vary). Some carriers include this automatically. Others charge $8-$15 monthly extra.

Disability waiver riders keep your coverage active without requiring premium payments if you become disabled. Sounds simple until you read the definitions. One insurer might require you to be completely unable to work any job whatsoever. Another waives premiums if you can't perform your specific occupation. Huge difference if you're a surgeon who loses fine motor control but could still work an office job.

Child coverage riders protect all your kids under one provision—typically $50,000-$100,000 per child for $5-$10 monthly total.

Accidental death riders double or triple payouts for accident-related deaths. They increase costs and add complexity (beneficiaries must prove the death was accidental, not related to health conditions).

Here's the critical comparison point: one carrier might include chronic illness riders at no extra charge. Another might charge $15 monthly. Across twenty years? That's $3,600 for identical protection.

Cash Value Accumulation (for Permanent Policies)

When you're doing a benefit evaluation guide for permanent policies, cash value mechanics separate mediocre policies from solid ones.

Cash value is basically a savings account inside your policy. It grows tax-deferred. You can borrow against it or make withdrawals.

Whole life policies build cash value on published schedules. You can look at year 15 and know exactly what your cash value will be. Guaranteed.

Universal life credits interest based on company performance. They guarantee a minimum (usually 2-3%) but might credit more. Variable life invests your cash value in sub-accounts similar to mutual funds—higher growth potential, but you can actually lose money.

Always distinguish guaranteed values from projected illustrations. Sales presentations love showing 7% annual returns. Sounds fantastic. Then you notice the guarantee only specifies 3%. That difference compounds dramatically over thirty years.

Look at surrender charges too—penalties for canceling your policy or withdrawing cash value early. Some policies charge 100% of cash value in year one, declining to zero over 10-20 years. You're effectively trapped in the policy during this period.

Borrowing provisions vary significantly. Certain policies charge 5-8% interest on loans while crediting your cash value 4-6%, creating a small spread that costs you money. Other structures use "wash loans" where the borrowing rate equals the crediting rate—effectively zero-cost loans.

Exclusions and Limitations

Every policy excludes specific circumstances or restricts coverage under certain conditions.

Standard exclusions typically cover suicide during the first two years and deaths resulting from illegal activities. Beyond those baseline restrictions, policies diverge considerably.

Aviation exclusions might apply only to private pilots. Or they might encompass any non-commercial flying whatsoever—even as a passenger in a friend's Cessna.

Military exclusions could address declared wars exclusively or include participation in any armed conflict, even peacekeeping missions.

Hazardous activity exclusions range widely. Some policies don't care if you skydive, scuba dive, rock climb, or race motorcycles. Others exclude all of these. One company rejected my client because he went bungee jumping once three years earlier.

The contestability period—typically two years—lets insurers investigate your application and deny claims if they discover material misrepresentations. Some policies extend this window for specific medical conditions. If you answered "no" about diabetes when you actually had a prior diagnosis, the carrier can reject claims during this period even when diabetes didn't cause death.

Geographic limitations occasionally pop up, restricting or eliminating coverage for deaths in certain countries. If you travel internationally for work, this matters significantly.

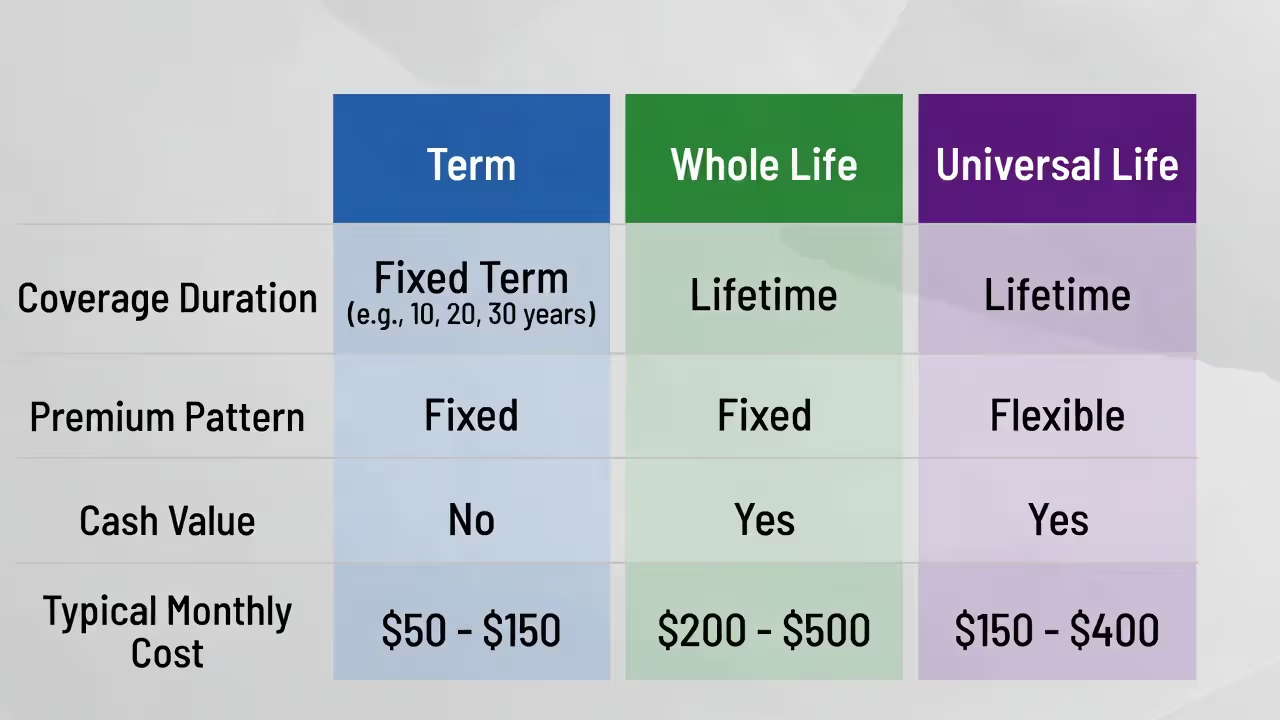

How to Evaluate Coverage Differences Between Term and Whole Life Insurance

Author: Christopher Baldwin;

Source: everymuslim.net

Choosing between term and permanent insurance isn't about which product category wins objectively. It's about which structure fits your financial situation and protection goals.

| Policy Type | How Long You're Covered | How Premiums Work | Does It Build Cash Value? | Who Should Buy It | What It Costs Monthly |

| Term Life | Fixed period (10-30 years) | Locked rate during term, then skyrockets if you renew | Nope—pure protection | People with temporary needs, tight budgets, young families | $25-$65 for $500K (age 35, 20-year term) |

| Whole Life | Until you die (usually to age 100-121) | Fixed forever—never increases | Yes—guaranteed growth, conservative returns | Estate planning, forced savings, lifetime coverage needs | $300-$500 for $500K (age 35) |

| Universal Life | Lifetime with flexibility | Adjustable within limits | Yes—fluctuates based on credited interest | Permanent protection wanted, but need payment flexibility | $200-$400 for $500K (age 35) |

Term insurance works best when your protection needs have clear end dates. You're raising kids who depend on your income, but that dependency evaporates once they're self-sufficient. You're 30 years old with a newborn—buy 25-year term coverage, and you're protected until the kid's 25.

The math favors term for straightforward protection. That same 30-year-old could buy $1 million in 25-year term coverage for roughly $50 monthly. Comparable whole life protection? Try $800 monthly. Invest that $750 monthly difference in retirement accounts earning 7% annually, and you'd accumulate approximately $600,000 over 25 years—while maintaining life insurance protection the entire time.

Permanent insurance makes sense when coverage needs extend indefinitely. Estate tax obligations don't disappear at 60. Final expenses exist regardless of when you die. Business owners using insurance to fund buy-sell agreements need permanent protection since nobody knows when a partner will die. Special-needs dependents requiring lifelong care need coverage that won't expire prematurely.

The cash value component adds a savings element absent from term. Yes, whole life returns typically lag stock market investments. But they're guaranteed, tax-advantaged, and enforce savings discipline. For people who struggle saving consistently or want genuinely conservative asset allocation, that savings feature provides value beyond pure insurance protection.

5 Common Mistakes When Comparing Life Insurance Quotes

Author: Christopher Baldwin;

Source: everymuslim.net

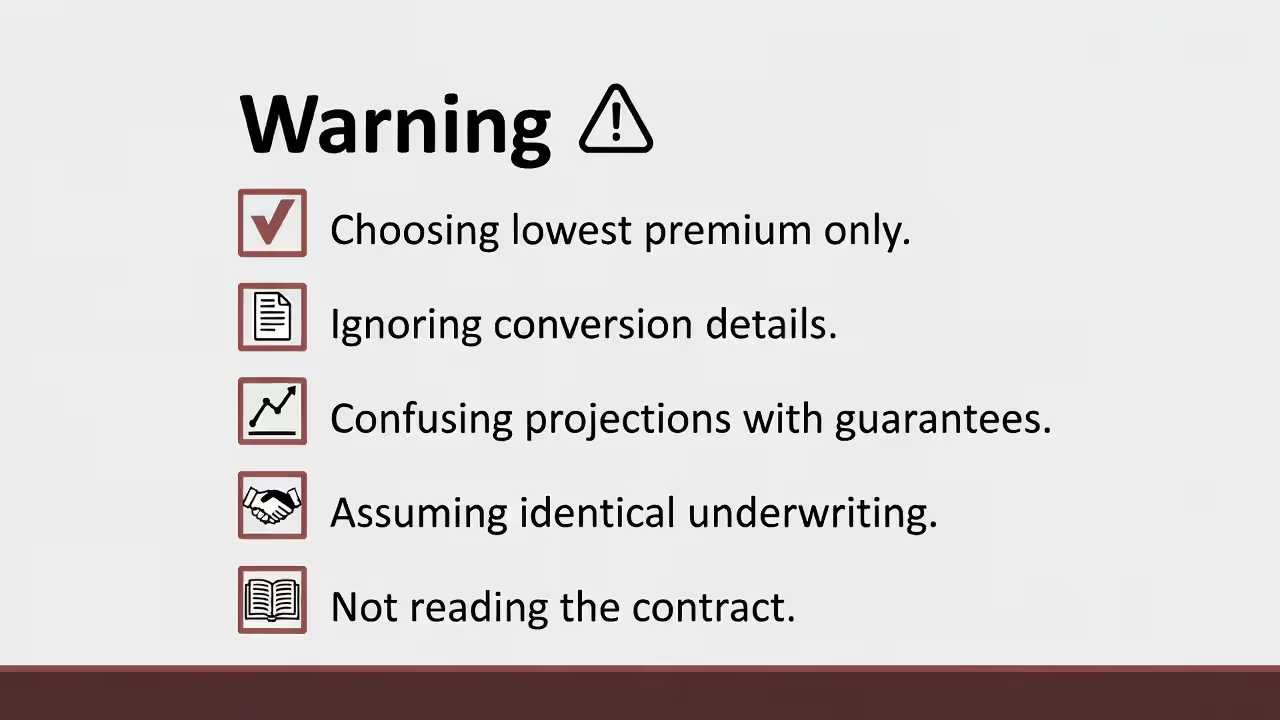

Chasing the lowest premium regardless of everything else. A $30 monthly policy from a B-rated carrier doesn't legitimately compare to a $35 policy from an A++-rated company. That $5 difference equals $1,200 over 20 years. Is saving twelve hundred bucks worth accepting a financially weaker insurer that might struggle paying claims in 2045?

Ignoring conversion option fine print. Many term policies let you convert to permanent coverage without taking another medical exam. Sounds great—and it is, if you read the specifics. Some contracts allow conversion throughout the entire term. Others restrict this to the first 5-10 years. Some let you convert to any permanent product the carrier sells. Others force you into specific whole life contracts only. If you're buying term but think you might want permanent coverage later, conversion privileges matter enormously.

Mistaking projected illustrations for guarantees. Permanent policy presentations show guaranteed performance (contractual minimums) and projected performance based on current assumptions. Sales reps emphasize projections displaying substantial cash value growth and potentially vanishing premiums. Compare the guaranteed columns between policies—those represent legal minimums insurers must deliver. Projections are educated guesses that might not happen.

Assuming all insurers underwrite health conditions identically. They don't. One company might rate someone with controlled hypertension as standard risk. A competitor adds a 25% premium surcharge. Different carriers specialize in different health conditions. If you're managing diabetes, sleep apnea, high cholesterol, or other medical issues, get quotes from multiple companies. I've seen identical applicants receive quotes from $85 to $210 monthly for the same coverage.

Skipping the actual policy contract review. Marketing brochures and agent explanations carry zero legal weight compared to actual policy language. Before finalizing anything, request and read the actual contract (or sample contracts if you're still comparing). Look specifically for exclusions, limitations, and conditions that weren't thoroughly explained during sales conversations. This matters especially for riders—that chronic illness rider you think covers any serious diagnosis might contain strict qualification criteria making claims extremely difficult.

Building Your Insurer Comparison Strategy: What to Research Beyond Price

Author: Christopher Baldwin;

Source: everymuslim.net

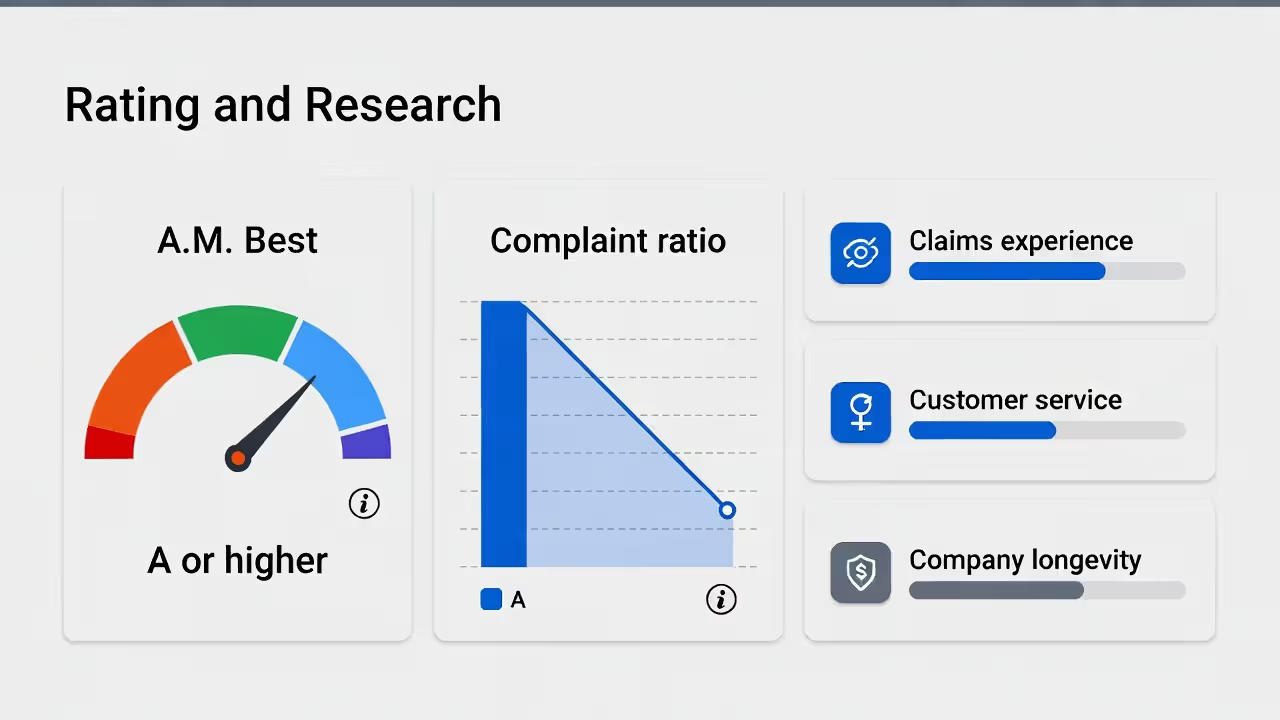

Financial strength deserves equal weight with premium costs when evaluating carriers.

Life insurance represents a multi-decade promise to pay. Your insurer needs financial stability to honor that promise in 2050. Rating agencies—A.M. Best, Moody's, Standard & Poor's, Fitch—assess insurers' financial health and claims-paying ability.

Target carriers rated A- or higher by A.M. Best (excellent financial strength). A++ and A+ ratings signify superior strength. Ratings below B++ suggest vulnerability during economic downturns. Check ratings across multiple agencies—consensus matters more than one isolated high rating.

When you're evaluating insurance companies, financial stability should weigh as heavily as premium comparisons—your policy's only as valuable as the carrier's ability to pay claims twenty or thirty years from now.

— Kevin Haney, Certified Financial Planner

Claims payment history reveals how insurers treat beneficiaries when it matters most. State insurance departments track complaints—these records are publicly accessible. High complaint ratios relative to company size indicate problems. Focus specifically on complaints about delayed claims, rejected claims, and poor communication during claims processes.

Customer service quality affects your experience throughout policy ownership. You'll contact your carrier to update beneficiaries, change addresses, request policy loans, or clarify coverage questions. Research customer service through J.D. Power ratings, Consumer Reports, and review platforms. Prioritize feedback addressing responsiveness, clear communication, and ease of making policy changes.

Company longevity signals stability. Insurers operating 50-100+ years have survived multiple economic crises, regulatory changes, and market disruptions. Newer companies can be perfectly sound, but established carriers demonstrate proven resilience. Check whether companies focus on life insurance or treat it as supplementary to other financial services—specialists often deliver better service and more competitive pricing.

State guaranty association coverage provides safety nets if your insurer collapses, but limits apply. Most states guarantee $300,000 in death benefits and $100,000 in cash values per insured life. If you're buying $1 million in coverage, $700,000 exceeds guaranty protection. Insurer financial strength becomes increasingly critical for larger policies.

Step-by-Step: How to Analyze and Compare Your Top 3 Policy Options

Author: Christopher Baldwin;

Source: everymuslim.net

Start by building a comparison spreadsheet. Columns represent each policy. Rows capture every feature relevant to your situation—death benefits, premiums, coverage duration, available riders, conversion privileges, financial strength ratings, specific exclusions. This visual framework exposes differences that remain hidden when reviewing policies individually.

Weight factors based on your specific circumstances. A 28-year-old in excellent health? Emphasize affordability and conversion flexibility—you've got decades ahead, and circumstances will change. A 55-year-old managing a health condition? Prioritize guaranteed acceptance and lenient underwriting over small premium differences. Buying permanent insurance? Cash value guarantees and loan provisions deserve heavy emphasis.

Calculate total long-term costs, not just monthly premiums. A $45 monthly policy with a $75 annual administrative fee totals $11,700 over 20 years. A $47 monthly policy without fees totals $11,280—you're saving $420 despite higher monthly premiums. For permanent coverage, calculate cost per thousand dollars of death benefit at years 10, 20, and 30 to understand how expenses evolve.

Request in-force illustrations for permanent policies showing cash value accumulation under different scenarios. Ask for illustrations assuming current rates, guaranteed minimums, and intermediate scenarios. Compare how policies perform if interest rates decline or company performance disappoints. The policy looking optimal under rosy assumptions might underperform under conservative projections.

Scrutinize language relevant to your specific circumstances. Travel internationally regularly? Find the exact language addressing geographic limitations. Pursue hobbies the insurer might classify as hazardous? Get written confirmation about whether they're excluded. Buying permanent insurance planning to use policy loans? Understand loan interest rates, repayment requirements, and impacts on death benefits.

Test customer service before purchasing. Contact each insurer with specific questions: "If I'm diagnosed with a chronic illness in year 8, what's the process for activating the chronic illness rider?" "What's your typical timeframe for beneficiary payouts?" "Can I change my beneficiary online or must I complete paper forms?" Response quality and speed indicate what service looks like when you actually need help.

Document everything. If representatives promise something—"You can convert this term policy anytime during the first 15 years"—request written documentation showing that feature in policy contracts. Verbal promises don't override written agreements. If you can't find a promised feature in policy documents, it doesn't exist contractually.

Frequently Asked Questions About Comparing Life Insurance Policies

Comparing life insurance means balancing numerous factors without complete information. You're forecasting future needs, evaluating company promises that won't be tested for decades, and building cost-benefit analyses based on unknowable variables like your actual lifespan.

The goal isn't discovering a theoretically perfect policy. It's identifying coverage that protects your family adequately, fits your budget sustainably, and comes from an insurer likely to fulfill commitments when needed. A good policy you actually buy beats a perfect policy you never purchase because you're endlessly comparing options.

Start with your coverage need—the amount your dependents would require if you died tomorrow. Work backward from that figure to identify policies delivering adequate protection at premiums you can maintain through income fluctuations and competing financial priorities. Emphasize financial strength ratings over minor premium differences. Read actual policy contracts before signing.

Most importantly? Get coverage now rather than waiting for the perfect moment or perfect policy. Life insurance costs increase with age. Health changes can render you uninsurable. Spend days or weeks comparing, not months. Your family's financial security depends on having active coverage, not on optimizing every detail of that coverage.