Laptop displaying side-by-side life insurance quote comparisons with a checklist of key policy details.

How to Choose Life Insurance?

Content

Here's what happens when most people start shopping for life insurance: they open three browser tabs, get quotes that range from $30 to $300 monthly, and close their laptop feeling more confused than when they started.

The insurance industry doesn't make this easy. You're comparing products you don't fully understand, using calculations you've never done before, trying to predict your family's financial needs 20 years from now. No wonder people either buy whatever their workplace offers or avoid the decision entirely.

Here's what actually matters. Your situation—not your neighbor's, not some online calculator's generic recommendation—should drive every coverage decision you make. We'll break down exactly how to figure that out.

Why Your Coverage Needs Are Different Than Everyone Else's

Take two people, both 35 years old. Sarah has three kids under 10, owes $280,000 on her mortgage, and her spouse stays home full-time. James has no kids, rents an apartment, and his partner earns more than he does.

Should they buy the same life insurance policy? Of course not. Yet agents often start with "most people your age get $500,000 in coverage" without asking a single question about your actual life.

Your coverage calculation begins with one question: who would struggle financially if you died tomorrow? Write down specific names. Your spouse who gave up their career to raise kids. Your 8-year-old daughter who'll need 15 more years of support. Your mother whose retirement income you supplement each month. Each person on this list represents a coverage need you can't ignore.

Then comes debt—the money you owe doesn't care that you're gone. Your $350,000 mortgage continues. That $18,000 car loan still needs monthly payments. Credit card balances of $8,000 sit there waiting. Add every dollar you owe to anyone. Your family will either pay these debts, watch assets get liquidated, or default while grieving.

Income replacement creates the biggest number in your calculation, and it should. If you bring home $6,000 monthly and your family needs that money to maintain their lifestyle for the next 18 years until your youngest finishes high school, you're looking at $1.3 million just for income replacement. Seems like a huge number, right? But $6,000 times 12 months times 18 years equals exactly that.

Don't forget the immediate costs when someone dies. Funerals run $7,000 to $12,000 depending on your choices. Outstanding medical bills from your final illness might add $5,000 to $20,000. Probate and estate settlement fees typically cost $3,000 to $8,000. These expenses hit within weeks of your death, right when your family has the least capacity to handle financial stress.

Age changes everything about this calculation. Buy coverage at 28, and you're locking in premiums based on decades of good health ahead of you. Wait until 48, and insurers price in the increased probability you'll die during the policy term. That's why a 30-year-old might pay $28 monthly for $500,000 in term coverage, while a 50-year-old pays $140 for an identical policy. Same coverage, five times the cost.

Author: Christopher Baldwin;

Source: everymuslim.net

Term vs. Permanent: Which Life Insurance Type Fits Your Budget and Goals?

Most first-time buyers should start with term insurance, then consider permanent coverage only if they have specific reasons. That's not the advice you'll get from insurance agents who earn bigger commissions on permanent policies, but it's what works for most families.

When Term Life Insurance Makes Sense

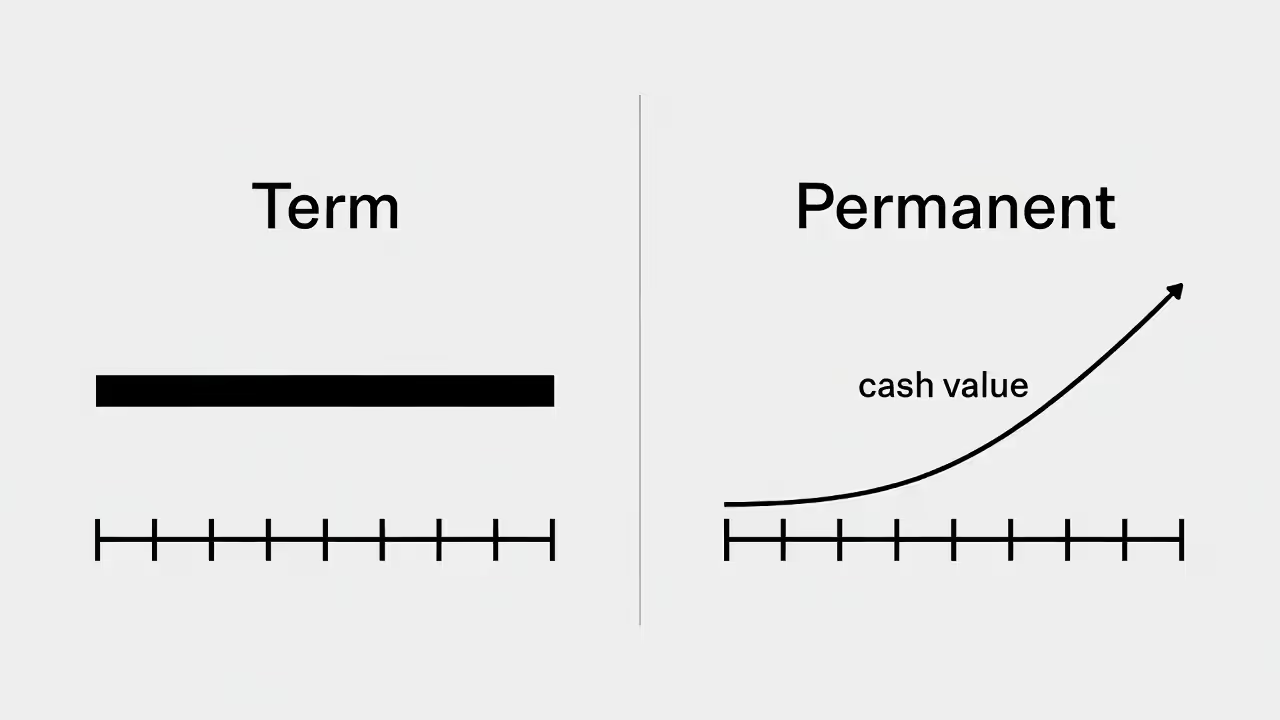

Term coverage protects you for a specific timeframe—maybe 15 years, maybe 30—then it ends. You pay the same premium every month during that period. When the term expires, you can sometimes renew at much higher rates, or you just let the policy lapse because you don't need it anymore.

This structure works beautifully when your financial responsibilities have a clear endpoint. Your kids will eventually support themselves. Your mortgage will get paid off. Your business partner will buy out your share of the company. These temporary needs match perfectly with temporary coverage.

The cost difference between term and permanent insurance is staggering. That $500,000 policy costing $35 monthly for a 30-year-old? The same death benefit in whole life might cost $420 monthly. You're paying twelve times more for features that might not benefit your situation at all.

Critics say term insurance "expires worthless" if you outlive the term, making it a bad investment. But life insurance isn't supposed to be an investment—it's protection against dying too soon. If you outlive your policy, congratulations. Your kids grew up, your debts got paid, and you didn't need the safety net. That's the best possible outcome.

Permanent Policies: Whole Life and Universal Life Explained

Whole life insurance guarantees coverage for your entire lifetime, charges premiums that never increase, and builds cash value that grows at rates the insurance company promises upfront. Die at 95, and your beneficiaries still collect the full death benefit.

This approach makes sense for estate planning when you know you'll leave a tax burden for your heirs. It works if you've maxed out 401(k) contributions, IRAs, and health savings accounts but want more tax-deferred growth. High-net-worth individuals sometimes use whole life specifically for its tax advantages and guaranteed death benefit.

But that coverage costs six to ten times what term insurance costs for the same death benefit. You're paying for lifetime protection and cash accumulation, whether those features solve actual problems in your financial life or not.

Universal life gives you flexibility—adjust your premiums up or down, increase or decrease the death benefit within certain limits, and watch your cash value grow based on current interest rates instead of guaranteed rates. This appeals to people whose income fluctuates unpredictably or who want the option to modify coverage as their situation changes.

The flexibility cuts both ways, though. If interest rates drop and your cash value doesn't grow as projected, your premiums might need to increase to keep the policy from lapsing. Indexed universal life tries to solve this by linking growth to stock market indexes while protecting against losses through guaranteed minimums. Variable universal life lets you put cash value into investment subaccounts similar to mutual funds, accepting market risk for potentially higher returns. Both variations add complexity and fees that require careful analysis before buying.

| Policy Type | Coverage Duration | Premium Structure | Cash Value | Best For | Typical Cost Range |

| Term | Set period like 20 years, then ends | Same payment monthly throughout the term | Doesn't build any | People with temporary financial obligations, families on tight budgets, anyone under 40 | $25-$70 monthly for $500K at age 30 |

| Whole Life | Until you die, no matter when | Fixed forever—never goes up | Grows at guaranteed rates | Estate planning needs, high earners wanting more tax-deferred growth, people needing lifetime coverage | $380-$580 monthly for $500K at age 30 |

| Universal | Your whole life if you fund it correctly | You can change it within limits | Grows based on current interest rates | People with irregular income, those wanting adjustment options | $180-$380 monthly for $500K at age 30 |

How Much Life Insurance Do You Actually Need?

Author: Christopher Baldwin;

Source: everymuslim.net

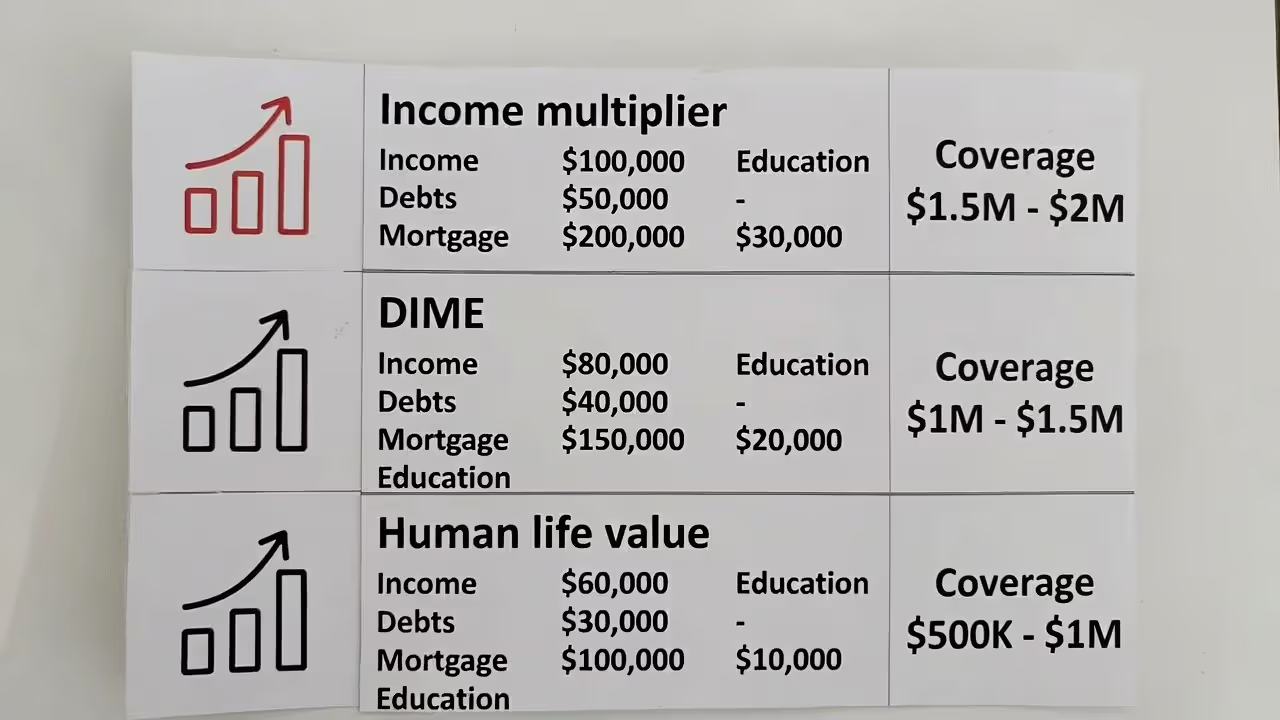

Different calculation methods will give you different numbers, which is frustrating but actually helpful. Run three different calculations, compare the results, and you'll find a reasonable range for your coverage amount.

Start with the simplest approach: multiply your annual income by 10 or 12. Earn $85,000? That suggests $850,000 to $1,020,000 in coverage. This takes about 30 seconds to calculate but completely ignores your specific debts, existing savings, and family structure. Use it as a rough starting point, not your final answer.

The DIME method—Debt, Income, Mortgage, Education—adds the specificity you need. Grab your most recent mortgage statement, loan balances, and that mental list of education costs you're worried about. Add them up:

- Debt: $22,000 in credit cards and car loans

- Income: $70,000 yearly for 20 years = $1,400,000

- Mortgage: $310,000 remaining balance

- Education: $120,000 for three kids' college funds

That totals $1,852,000 before you subtract existing assets. Got $200,000 in retirement accounts and savings? Subtract that. Your net coverage need drops to $1,652,000, which you might round to $1.75 million for a clean policy amount.

The human life value approach calculates the present value of your future earnings minus what you spend on yourself. This gets mathematical fast. Say you earn $95,000, spend about $32,000 annually on personal expenses (everything that wouldn't continue after you die), and plan to work 28 more years. Using a 3% discount rate for inflation, your economic value to your family calculates to roughly $1.6 million. You can do this in Excel or find online calculators that handle the present value math.

Let's work through a real example. Marcus, age 37, earns $92,000 annually. He's got two kids, ages 6 and 9. Outstanding debts include a $265,000 mortgage, $8,500 in credit card balances, and a $19,000 car loan. His spouse works part-time earning $28,000, enough to cover basics but not maintain their current lifestyle. Marcus wants both kids to attend in-state public universities—figure $100,000 total for both.

Marcus's calculation: - Debt payoff: $292,500 - Income replacement: Need to replace $64,000 annually (his salary minus spouse's income) for 16 years until both kids finish college = $1,024,000 - Education fund: $100,000 - Final expenses: $12,000 for funeral and estate costs - Total: $1,428,500

Marcus rounds to $1.5 million. He splits this between two policies: a $1 million 20-year term (covering peak responsibility years) and a $500,000 30-year term (maintaining some protection longer). When his youngest graduates college in 15 years, he'll still carry $500,000 in coverage for another 15 years at premiums he locked in at age 37.

5 Critical Factors That Should Drive Your Policy Decision

Author: Christopher Baldwin;

Source: everymuslim.net

Premium cost matters, obviously. But five other insurance decision factors determine whether your policy actually protects your family or fails at the worst possible moment.

Your current health and medical background: Insurance companies sort applicants into risk categories—preferred plus for exceptionally healthy people, preferred for generally healthy folks, standard for average health, and substandard for people with significant medical issues. The difference between preferred plus and standard pricing might mean paying $38 monthly versus $68 monthly for identical coverage. Pre-existing conditions don't automatically disqualify you. Diabetes, previous heart attacks, or cancer history will increase your premiums, sometimes dramatically, but specialty insurers work with high-risk applicants when standard companies decline coverage.

Whether you can actually afford the premiums long-term: A policy you cancel in four years because the payments became unmanageable helps nobody. Run a stress test on your budget—could you maintain these premium payments if your income dropped 25%? When choosing policy length, remember that longer terms cost more monthly but lock in rates for more years. A 30-year term might cost $58 monthly while a 20-year term costs $42. That extra $16 buys you an additional decade of rate protection. If budget constraints are tight, buy less coverage you can sustain rather than maximum coverage you'll eventually drop.

Rider options that address your specific risks: Riders customize your base policy for particular situations. Waiver of premium coverage means your policy stays active even if a disability prevents you from working and paying premiums—you're typically out of work six months before this kicks in, and it costs roughly $3 to $7 monthly per $100,000 of coverage. Accelerated death benefit riders allow you to collect part of your death benefit early if doctors diagnose a terminal illness—most insurers include this free. Child term riders cover all your children under one addition to your policy rather than buying separate policies for each kid. Evaluate riders based on realistic risks in your life, not their low cost or the agent's recommendation.

The financial stability of the insurance company: Your policy's value depends entirely on the company's ability to pay claims in 20 years. Check financial strength ratings from AM Best, Moody's, or Standard & Poor's—look for ratings of A or A+ at minimum. Companies rated B or lower might offer attractive premiums but carry concerning financial risks. A weak insurer might delay claim payments, fight valid claims, or in worst cases, fail completely and leave your beneficiaries with reduced payouts from state guarantee funds (which have limits). Always verify financial ratings before buying, especially from companies you've never heard of offering suspiciously low premiums.

Conversion rights and renewal terms: Most term policies let you convert to permanent coverage without taking another medical exam. This matters enormously if you develop serious health problems during your term and want to extend protection. Some policies allow conversion during the entire term period, while others restrict conversion to the first 10 or 15 years. Similarly, check renewal provisions—when your term ends, can you renew coverage (at higher rates) without medical underwriting? Some policies guarantee renewability through age 95, giving you options even if you become uninsurable.

People choose policies by comparing premium costs in a spreadsheet without ever asking whether the coverage actually solves their financial problem. I've reviewed $250,000 policies bought by parents with $400,000 mortgages and three young kids—they saved $20 monthly but left a massive gap that defeats the entire purpose of buying life insurance. Any premium is expensive if the coverage doesn't match your needs.

— Michael Chen, CFP with Cornerstone Wealth Advisors

How to Compare Life Insurance Quotes Without Getting Confused

You've requested quotes from four different insurers. Now you're staring at numbers ranging from $42 to $89 monthly, trying to figure out what justifies the price differences. These policy comparison tips help you evaluate options systematically instead of just picking the cheapest.

Calculate total cost over the entire term, not just monthly premiums. A policy charging $48 monthly for 20 years costs $11,520 total. One charging $56 monthly costs $13,440 total. That $8 monthly difference equals $1,920 over the policy's lifetime—significant enough to matter, but maybe worthwhile if the pricier policy comes from a financially stronger company or includes better conversion options.

Request full policy illustrations for permanent insurance, which show both guaranteed values and projected values under different scenarios. Pay closest attention to the guaranteed columns—those represent the worst-case performance the company promises contractually. Projected columns assume favorable interest rates or investment returns that might never materialize. If you're buying based on projected values, you're gambling.

Read the exclusions section, usually buried on page 20-something of the policy documents. Nearly all policies exclude suicide during the first two years of coverage and deaths resulting from illegal activities. Some exclude aviation deaths except commercial airline flights, deaths during war or military conflict, or deaths during dangerous recreational activities. If you're a private pilot, frequent international traveler to unstable regions, or serious rock climber, find a company that covers your specific activities without exclusions.

Understand the two-year contestability period. During the first two years of coverage, insurers can investigate claims and deny payment if they discover you misrepresented information on your application—even innocent mistakes can cause problems. Did you forget about that high blood pressure diagnosis from eight years ago? The insurer might deny your claim. Be completely truthful on your application, even if it means higher premiums or waiting to apply after improving your health.

Check company complaint data through your state insurance department's website. Some insurers offer attractively low premiums but generate excessive complaints about denied claims, poor customer service, or payment delays. The National Association of Insurance Commissioners compiles complaint ratios showing which companies receive more complaints than their market share would predict. A company with 5% market share shouldn't generate 15% of complaints.

Compare identical coverage amounts and terms across all quotes. If one quote shows $750,000 coverage and another shows $1 million, you can't accurately compare prices—adjust your requests so every quote reflects the same death benefit and term length. Otherwise you're comparing different products and the premium differences become meaningless.

Common Mistakes People Make When Buying Their First Policy

Author: Christopher Baldwin;

Source: everymuslim.net

Learn from other buyers' mistakes instead of making expensive errors yourself.

Buying too little coverage to save money: Purchasing $300,000 in coverage when you actually need $1 million saves you maybe $40 monthly. But it leaves your family $700,000 short, meaning they'll burn through that death benefit in three or four years, then face financial crisis. If premium cost is your limiting factor, buy term insurance to maximize coverage per dollar spent rather than reducing your coverage amount below what your family actually needs.

Making decisions based purely on price: The cheapest premium usually indicates something—weaker financial ratings, more restrictive policy terms, or an insurer taking on riskier applicants to gain market share. When one company's quote comes in 35% below three competitors, dig deeper. Sometimes you get what you pay for. Balance cost against company quality, customer service reputation, and policy features.

Skipping riders that would actually help: Disability waiver of premium costs maybe $6 monthly but prevents policy lapse if you become unable to work. Skipping it to save that $6 feels smart until a car accident leaves you disabled, unable to pay premiums, and watching your coverage disappear when your family needs it most. Evaluate riders against realistic risks in your situation, not their cost. A $5 monthly rider that prevents a $50,000 problem is worth buying.

Never reviewing coverage after life changes: Your coverage needs shift dramatically when you have another baby, buy a bigger house, start a business, get divorced, or inherit significant assets. Set a calendar reminder to review your policy every four years minimum, and always reassess coverage after major life events. You might need additional coverage, a second policy with a different term length, or beneficiary updates. Insurance isn't a "buy it and forget it" product.

Only checking one source for coverage: Some people only review their employer's group life insurance offering. Others call a single agent recommended by a family member. Group coverage through work frequently disappears when you change jobs and rarely provides adequate death benefits—it's typically one or two times your salary, nowhere near enough for most families. Independent insurance agents can quote multiple carriers but might push products offering them higher commissions. Check employer coverage, obtain quotes from independent agents, and research direct-to-consumer online insurers for comprehensive comparison before deciding.

Delaying purchase until you're older or sick: Waiting costs you, sometimes dramatically. Every birthday that passes increases your premiums. A health diagnosis can make you uninsurable or push premiums so high that coverage becomes unaffordable. The difference between buying at 30 versus 40 might mean paying one-third of what you'd pay at the older age for identical coverage. Buy when you're young and healthy, even if your need for protection seems theoretical. You're locking in rates based on current health that you'll never get again.

Frequently Asked Questions About Choosing Life Insurance

Choosing life insurance comes down to honest assessment of what happens financially to your family when your income disappears. Calculate outstanding debts that would burden survivors. Figure out income replacement needs based on how long dependents will rely on your earnings. Add future expenses like college tuition that won't pay themselves.

Compare term and permanent options starting from your actual situation, not from what sounds appealing in an agent's pitch. Get quotes from at least three insurers, checking both premium costs and company financial strength ratings. Don't sacrifice adequate coverage to shave $25 off monthly premiums—proper protection matters more than minimal cost.

Consider which riders address real risks in your life, and verify your policy includes conversion privileges in case your situation changes. Most importantly, review your coverage every three or four years as financial circumstances evolve. Life insurance isn't something you buy once and ignore for 30 years—it's an ongoing piece of your financial protection that should adjust as responsibilities grow and eventually shrink.

Start this process today instead of waiting for some mythical perfect moment. Your current health and age give you pricing advantages that erode with every passing month. One afternoon spent comparing options and completing an application buys decades of protection for the people who depend on you financially.