Person comparing life insurance options on a laptop with notes about coverage needs.

Buy Life Insurance Direct Guide

Content

Getting life insurance doesn't require scheduling appointments or entertaining sales pitches in your living room anymore. More Americans now handle this purchase on their own, researching options at midnight in sweatpants and clicking "submit" without ever speaking to a commissioned salesperson.

Can you really navigate this alone? Absolutely—if you know what to look for and where the potential problems hide. This guide maps out the entire journey, from calculating how much coverage makes sense to spotting the fine print that could matter decades from now.

Why More Americans Are Choosing Direct Life Insurance Purchases

The independent buying process gained serious momentum around 2020, but its roots go back further. Insurance companies started building consumer-friendly platforms years earlier, betting that people who'd grown comfortable booking flights and managing investments online would eventually warm to buying coverage the same way.

Transparency appeals to modern buyers. Traditional policies involve agent commissions—sometimes 55% of your first year's premium for a term policy, occasionally climbing above 100% for certain products. These commissions get baked into the carrier's cost structure rather than appearing as separate line items on your bill. Still, knowing that nobody's earning a bonus by steering you toward Product B instead of Product A changes the psychology of shopping.

The control factor matters just as much. Buy direct and you're in charge of the timeline. Compare coverage on Tuesday night, sleep on it, revisit the decision Friday morning—nobody's calling to "check in" or creating urgency where none exists. Spreadsheet lovers particularly appreciate this autonomy.

The direct life insurance market has matured significantly. Ten years ago, I would have hesitated to recommend the DIY route for most clients. Today, the tools available for self-guided comparison rival what agents use internally—sometimes they're better because they're designed for consumer clarity rather than sales efficiency.

— Michael Keller

But here's the reality check: going solo isn't always smarter. Complicated scenarios—think second marriages with kids from previous relationships, seven-figure coverage needs, or significant health complications—often justify bringing in expertise. Understanding whether your situation fits the direct-purchase model matters more than following trends.

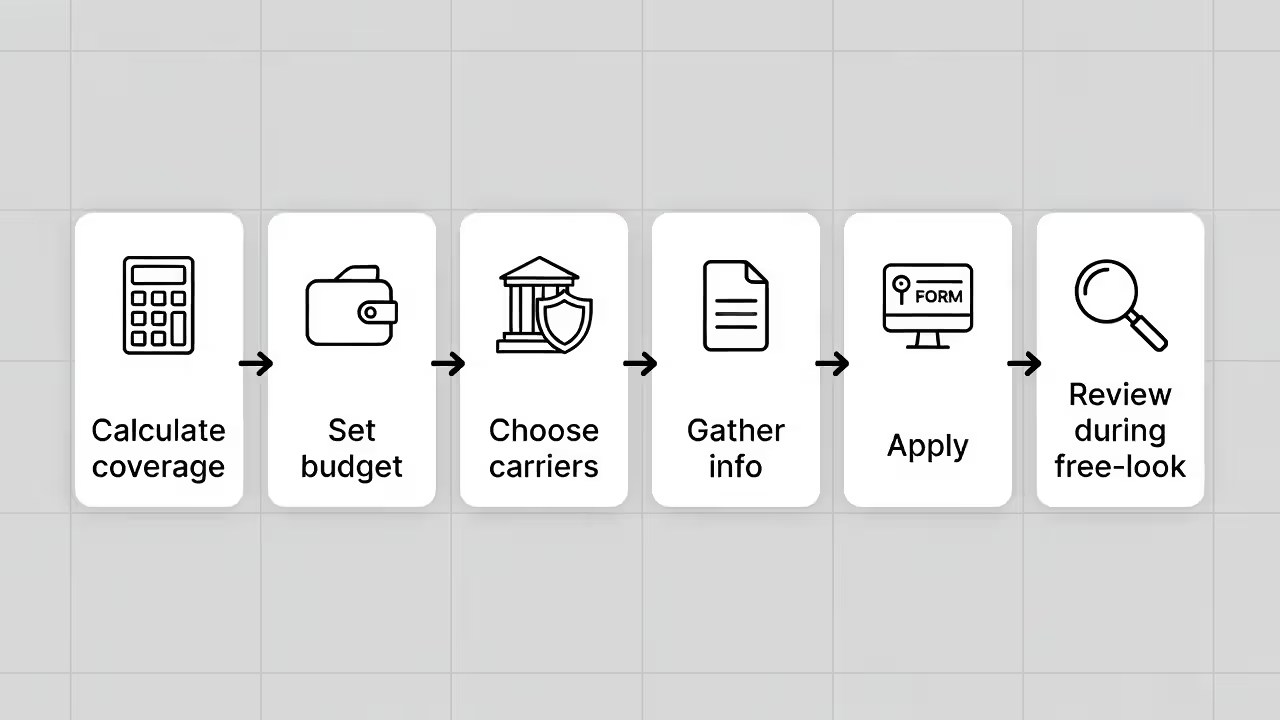

Step-by-Step Process for Buying Life Insurance Independently

Buying life insurance without an agent follows a logical path, but rushing through stages or skipping them entirely creates headaches later. Here's the systematic approach.

Author: Michael Stanton;

Source: everymuslim.net

Determining Your Coverage Needs and Budget

Before visiting any carrier's website, run the actual numbers. That "10x your salary" shortcut? Too simplistic.

Build your calculation from the ground up. List immediate obligations: mortgage balance ($285,000), car loans ($18,000), credit cards ($8,000), final expenses ($10,000). Then income replacement—figure five to ten years of your salary depending on your family's circumstances. A stay-at-home spouse might need longer coverage since reentering the workforce takes time. Tack on college funding if your kids are young.

Real example: A 37-year-old earning $82,000 annually with a $265,000 mortgage, two children ages 6 and 9, and $35,000 in various debts needs roughly $750,000 to $900,000. That covers the mortgage, replaces seven years of income, funds college contributions, and handles final costs plus a buffer.

Budget creates boundaries. Term life remains remarkably affordable—healthy 30-year-olds regularly secure $500,000 in 20-year coverage for $25 to $35 monthly. Age, health conditions, and policy type shift these numbers considerably. Run quotes at multiple coverage levels to find where adequate protection intersects with what you can actually pay.

Identifying Reputable Direct-to-Consumer Carriers

Not every insurance company sells directly to consumers. Many operate exclusively through agent networks. Direct-purchase options include Haven Life (MassMutual's digital arm), Ladder, State Farm's online channel, GEICO, Ethos, and Bestow among others.

Financial strength comes first. Check A.M. Best, Moody's, or Standard & Poor's ratings. Target carriers with A- ratings minimum—preferably A or better. Buying cheap coverage from a financially wobbly company is pointless if they can't pay claims in 2045.

Match carriers to your situation. Some specialize in simplified-issue policies (no medical exam, capped at $500,000 or lower coverage). Others provide fully underwritten policies with higher limits but require paramedical exams. Health conditions? Certain carriers show more flexibility—one might reject a controlled diabetes diagnosis while another offers standard rates.

Customer reviews need context. Insurance reviews skew negative because satisfied customers rarely post "This company hasn't paid a claim yet because I'm still alive—five stars!" Focus on application experience and claims handling instead of emotional reactions.

Gathering Required Documentation

Applications ask for basics: full legal name, address, Social Security number, employment information, beneficiary details. Then comes health history—medical conditions, prescriptions, height, weight, tobacco use, hazardous hobbies.

Keep recent medical records accessible for significant health events. Carriers check your answers against Medical Information Bureau (MIB) databases and prescription records. Inconsistencies cause delays or denials. Saw a cardiologist last year for a precautionary stress test? Disclose it. They'll discover it anyway through background checks.

Larger policies trigger paramedical exams. A technician visits your home, records vitals, draws blood, collects urine samples. Fast 8-12 hours beforehand and skip alcohol for 24 hours. Dehydration artificially elevates certain lab markers, so hydrate well.

How to Research and Compare Policies Without Professional Help

Author: Michael Stanton;

Source: everymuslim.net

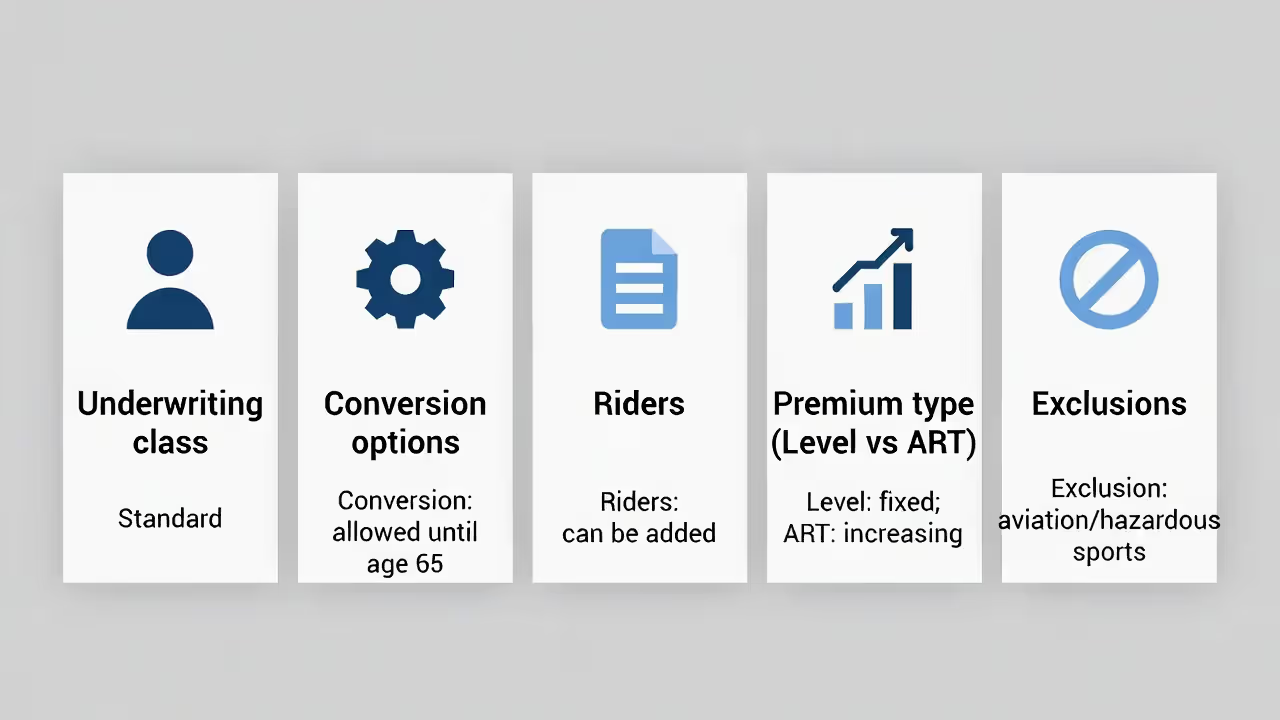

Effective online research starts with understanding what you're actually comparing. Two $500,000 20-year term policies priced similarly aren't identical if one restricts conversion options while the other offers flexibility until age 65.

Start with aggregator sites pulling quotes from multiple carriers—PolicyGenius, Quotacy, and SelectQuote's digital tools show side-by-side pricing. These platforms reveal which carriers offer competitive rates for your age, health profile, and coverage amount. Premiums matter, but don't make price your only consideration.

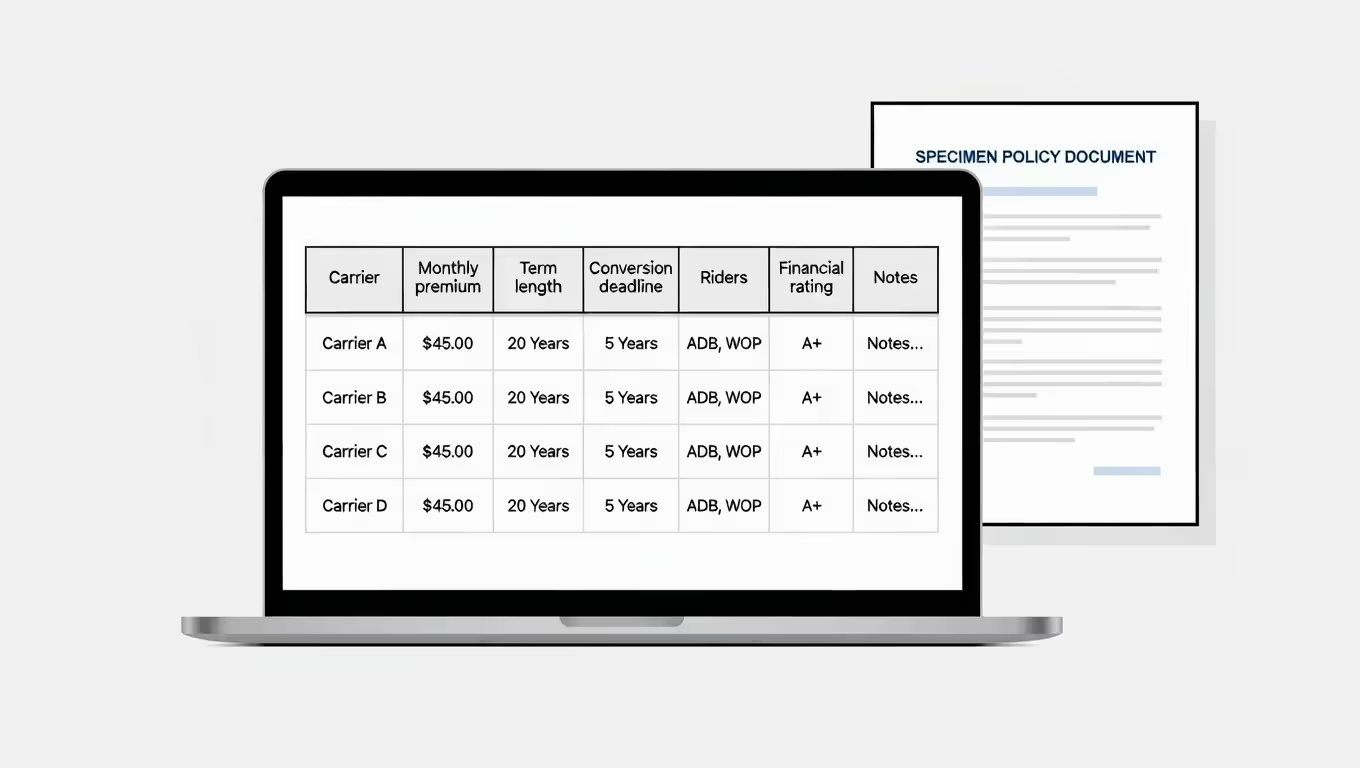

Download actual policy documents—not marketing summaries. Request the policy illustration and specimen policy (sample contract). These reveal buried details: contestability periods, suicide clauses, grace periods for missed payments, circumstances that void coverage.

Rating agencies offer more than financial strength scores. A.M. Best publishes detailed analyses of insurers' claims-paying history and business practices. State insurance department websites show complaint ratios—grievances received relative to market share.

Self-guided comparison becomes manageable with spreadsheets. List carriers down the left column. Create columns for premium, coverage amount, term length, conversion deadline, available riders, financial rating, and distinguishing features. This layout exposes trade-offs immediately. Maybe Carrier A costs $5 more monthly but allows conversion through age 65 versus Carrier B's ten-year conversion window—that extra $1,200 over 20 years might prove valuable if you develop health issues.

Online communities provide real experiences. Reddit's r/lifeinsurance and Bogleheads forums contain detailed carrier discussions and underwriting outcomes—actual people sharing "I'm 42, take blood pressure meds and a statin, Company X offered Standard Plus while Company Y gave me Standard" data points you won't find elsewhere.

Essential Policy Features You Must Evaluate on Your Own

Author: Michael Stanton;

Source: everymuslim.net

Policy evaluation methods depend on understanding contract components. Without an agent breaking these down, you're responsible for dissecting them yourself.

Underwriting classes determine premiums. Preferred Plus (sometimes Preferred Elite or Super Preferred) represents the top tier—reserved for exceptionally healthy applicants. Preferred follows, then Standard Plus and Standard. Substandard ratings (Table 2-10 or lettered ratings A-J depending on insurer) apply to higher-risk applicants. Moving down one class changes premiums 15-25%. Borderline between classes? Losing ten pounds or lowering cholesterol could save $3,000+ over a policy's life.

Conversion options allow exchanging term coverage for permanent insurance without new medical underwriting. Critical if your health declines. Picture a 30-year-old developing diabetes at 45—they can convert their term policy to whole life, securing insurability despite the diagnosis. Conversion windows differ dramatically. Some carriers permit conversion through age 65 or until two years before term expiration. Others cap it at ten years from policy issue. Shorter windows diminish the feature's utility.

Riders customize policies. Disability waiver of premium keeps coverage active if you become disabled and can't work—the insurer pays premiums on your behalf. Child term riders add coverage for your children at minimal cost. Accelerated death benefit riders provide access to part of the death benefit for terminal illness diagnoses. Some riders come standard while others add cost. Evaluate actual utility—return of premium riders sound appealing (recover premiums if you outlive the term) but typically increase costs 30-50%, rarely worth it mathematically.

Premium structures take two forms: level and annual renewable. Level premiums remain constant throughout the term—$35 monthly for 20 years straight. Annual renewable term (ART) starts cheaper but climbs yearly as you age. ART works for temporary needs like covering a five-year loan payoff. Level term makes more sense for longer protection periods.

Exclusions and limitations define what isn't covered. Nearly every policy excludes suicide during the first two years and deaths from illegal activities. Some exclude aviation deaths for private pilots, hazardous sports like BASE jumping, or travel to high-risk countries. Got relevant hobbies or occupations? Confirm the policy covers them or negotiate exclusion waivers.

Common Mistakes When Buying Life Insurance Direct (And How to Avoid Them)

Author: Michael Stanton;

Source: everymuslim.net

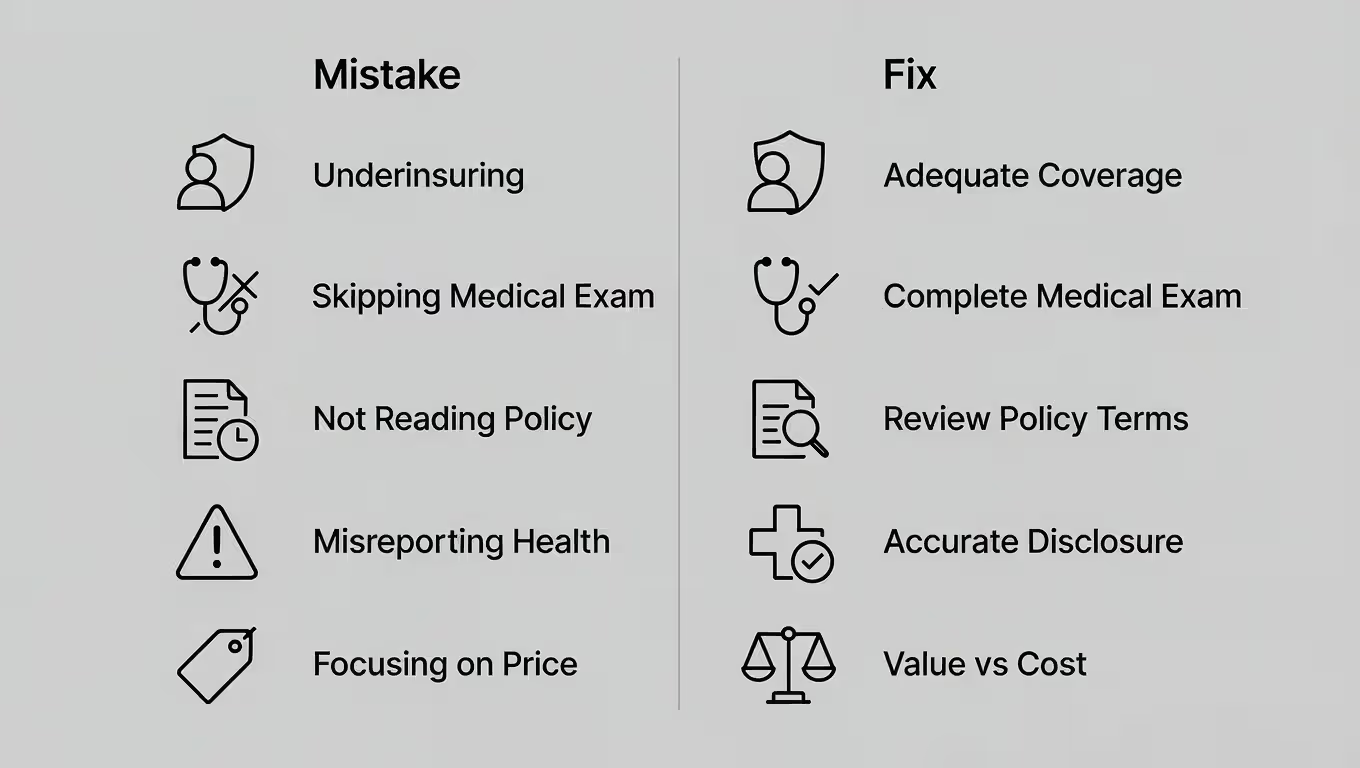

Underinsuring costs the most in the long run. Without an agent prompting comprehensive thinking, buyers lowball coverage. You mentally tally mortgage and debts, land at $400,000, call it done—forgetting your spouse loses your income, childcare contributions, and future earnings. Build buffers. If calculations suggest $400,000, consider $500,000 or $600,000. The incremental cost is modest relative to the protection gap.

Misunderstanding terminology trips up direct buyers. "Guaranteed renewable" doesn't mean premiums stay flat—it means the carrier can't cancel your policy but may raise rates (common with annual renewable term). "Convertible" doesn't guarantee affordability—you convert without underwriting, but the permanent policy's premium reflects your age at conversion, potentially prohibitively expensive.

Skipping medical exams when they'd benefit you seems counterintuitive but happens frequently. No-exam simplified-issue policies offer convenience but assume higher risk and price accordingly. Healthy applicants taking exams usually qualify for better rates offsetting the inconvenience. A 40-year-old non-smoker with solid vitals might pay $45 monthly for $500,000 via no-exam policy versus $32 with full underwriting—$3,120 saved over 20 years.

Ignoring policy documents until after the free-look period expires is inexcusable yet common. Most states mandate 10-30 day free-look windows allowing full-refund cancellation. Read every page during this period. Something contradicts website expectations or illustrations? Call immediately. After free-look expires, you're committed unless you surrender the policy and reapply elsewhere—risking higher premiums if you've aged or your health changed.

Lying or "forgetting" application details constitutes fraud. Some applicants rationalize omitting doctor visits or downplaying alcohol consumption. Carriers investigate claims, especially during the contestability period (first two years). Discovering misrepresentation lets them deny claims or rescind policies. Your beneficiaries receive nothing and you've wasted years of premiums.

Direct Purchase vs. Agent-Assisted: Cost and Service Trade-offs

Choosing between buying life insurance without an agent and working with one involves trade-offs varying by individual circumstances. Here's the comparison:

| Feature | Direct Purchase | Agent-Assisted |

| Cost/Commissions | No separate commission fee; potentially lower premiums from direct-only carriers | Commissions embedded in premium (50-110% of first-year premium for term); no direct buyer cost |

| Application Speed | Often faster; digital applications approved minutes to days | Slower; requires meeting scheduling, agent follow-up waiting |

| Policy Selection Support | Self-service tools, calculators, online resources; minimal human guidance | Personalized recommendations from detailed needs analysis; multi-carrier access |

| Ongoing Service | Automated reminders, online account management, chatbots; limited personal support | Dedicated contact for questions, policy reviews, beneficiary updates, claims help |

| Best For Whom | Straightforward situations, healthy applicants, financially literate consumers, control seekers | Complex needs, health issues needing underwriting expertise, human guidance preference |

| Typical Savings | 5-15% lower premiums with direct-only carriers; time savings avoiding meetings | Access to specialized products unavailable direct; potentially better underwriting for complicated cases |

Cost differences aren't always dramatic. Commissions don't necessarily inflate agent-sold policy prices because carriers price products based on distribution channels. A company selling both ways might charge identical premiums regardless, pocketing commission savings when you buy direct instead of passing savings along. Direct-only carriers like Ladder or Haven Life offer lower rates because their entire business model eliminates agent infrastructure expenses.

Service expectations play a role. Direct purchase makes you the project manager. Need to update beneficiaries? Log into a portal. Questions about claims? You call general customer service, not someone familiar with your situation. For most people this works fine—life insurance is set-it-and-forget-it. But valuing relationships and anticipating guidance needs makes paying for agent access (through slightly higher premiums or foregone savings) worthwhile.

Complex scenarios often benefit from agent expertise. Buying $5 million coverage, coordinating with estate planning, or navigating tricky medical history that requires shopping multiple carriers for optimal underwriting—an experienced agent saves time and potentially secures better outcomes than solo research achieves. Agents know carrier appetites—Company X rates diabetics favorably, Company Y handles anxiety disorders better. That intelligence is tough replicating through independent research.

Conversely, healthy 32-year-olds buying $500,000 of 20-year term coverage face straightforward decisions. You don't need someone explaining you should name your spouse as beneficiary or that term insurance expires when the term ends. The direct route saves time and potentially money.

Frequently Asked Questions About Buying Life Insurance Without an Agent

Taking responsibility for the entire purchase process requires more upfront work than delegating to a professional, but that effort pays off in understanding and control. You'll know precisely what you bought and why, rather than trusting someone else's recommendations.

Approach this seriously. Block dedicated time to run multiple quotes, thoroughly read policy documents, and verify financial ratings. Take advantage of self-guided comparison tools, but resist rushing. Careful decisions now prevent regret later when you realize the policy doesn't quite match your needs.

Purchasing directly doesn't mean complete isolation. Carriers provide educational resources, calculators model different scenarios, and customer service teams answer product-specific questions. You're bypassing commissioned salespeople, not abandoning all support.

Start by precisely determining coverage needs, identify three to five carriers serving your profile, request quotes and policy illustrations from each, compare them systematically, and choose the option balancing cost with features you'll actually use. After applying and receiving approval, read your policy during the free-look period and confirm it matches expectations.

For many Americans, direct purchase strategies deliver exactly what they need: straightforward protection at fair prices, purchased on their own terms. If your situation fits that model, the independent buying process gives you control over one of your family's most important financial safeguards.