Person using a life insurance calculator with financial documents and notes showing how coverage is calculated.

How Much Life Insurance Do I Need?

Content

Figuring out the right amount of life insurance feels like guessing at a moving target. You want enough to protect your family without overpaying for coverage you don't need. The stakes are high—get it wrong, and your loved ones could face financial hardship or you'll waste thousands on unnecessary premiums.

Most people start with a quick online calculator that spits out a number based on minimal information. That's a starting point, but your actual needs depend on factors these tools can't capture: your career trajectory, family dynamics, existing assets, and financial obligations that extend years into the future.

This guide walks through the calculation methods financial professionals use, shows you how to apply them to your situation, and helps you avoid the common traps that leave families either under-insured or paying for more coverage than they'll ever use.

Why Standard Rules of Thumb Fall Short for Most Families

The "10 times your salary" rule gets repeated so often it sounds like gospel. A $75,000 earner buys $750,000 in coverage, checks the box, and moves on. But this oversimplified approach ignores whether you have two kids or five, whether your spouse works, and whether you're carrying $300,000 in debt or none at all.

Other multipliers—like 5x or 15x salary—suffer from the same problem. They treat everyone in the same income bracket identically, regardless of their actual financial situation. A single parent with three children and a mortgage has radically different needs than a married professional with no kids and substantial savings, even if they earn the same amount.

Needs based insurance calculations look at your specific obligations, dependents, and resources. Instead of starting with your income and multiplying, you start with what your family would actually need if you died tomorrow. The difference between these approaches can easily be $200,000 or more in either direction.

Generic multipliers were created for speed, not accuracy. I've seen families with $1 million in coverage who needed $2.5 million, and others paying for $500,000 they didn't need. The ten-minute calculation that considers your actual debts, dependents, and existing assets is worth far more than the ten-second rule that doesn't.

— Jennifer Martinez, CFP® and principal at Cornerstone Financial Planning

The policy sizing guide that works for you must account for variables that generic formulas ignore: your spouse's earning potential, your children's ages and education plans, whether you own a business, and how much you've already saved. These factors can swing your required coverage by hundreds of thousands of dollars.

The Income Replacement Method: Calculating Years of Lost Earnings

The income replacement rule starts with a straightforward question: How many years of your income does your family need to replace? If you earn $80,000 annually and want to replace 20 years of earnings, that's $1.6 million. But inflation and investment returns complicate this simple math.

Author: Christopher Baldwin;

Source: everymuslim.net

Here's the step-by-step process:

- Step 1: Determine how many years your family needs your income. This typically extends until your youngest child finishes college or your spouse reaches retirement age, whichever scenario fits your situation.

- Step 2: Calculate your annual after-tax income. If you earn $90,000 but take home $68,000 after taxes, use the lower number—that's what your family actually depends on.

- Step 3: Adjust for inflation. Money 15 years from now won't buy what it does today. At 3% annual inflation, $60,000 in today's dollars equals roughly $93,000 in 15 years.

- Step 4: Factor in investment returns. Your death benefit won't sit idle—your family will invest it. If the insurance payout earns 5% annually while inflation runs at 3%, the real return is about 2%. This means you need less coverage than a straight multiplication would suggest.

Using a financial calculator or spreadsheet, you can determine the lump sum needed to generate your annual income for the specified period, accounting for both factors. For example, replacing $70,000 annually for 20 years with a 2% real return requires approximately $1.15 million, not the $1.4 million you'd get from simple multiplication.

When this method works best: You're the primary or sole earner, your family's living expenses closely match your take-home pay, and you want straightforward coverage calculation methods that focus on maintaining current lifestyle.

Adjusting for Dual-Income Households

When both spouses work, you need coverage for each person. But the calculations aren't always symmetrical. Consider a household where one spouse earns $100,000 and the other earns $45,000. The higher earner's death would create a larger income gap, but the lower earner's death might force the surviving spouse to pay for childcare, reducing their effective income.

Calculate each person's coverage separately by asking: What expenses would increase or what income would decrease if this person died? The parent who handles school drop-offs and pickups provides economic value beyond their paycheck. If they died, the surviving parent might need to reduce work hours, hire help, or pay for after-school programs.

A practical approach: Calculate income replacement for both spouses, then add $50,000-$100,000 to the lower earner's coverage to account for the services they provide. This ensures the surviving spouse can maintain work commitments without burning out.

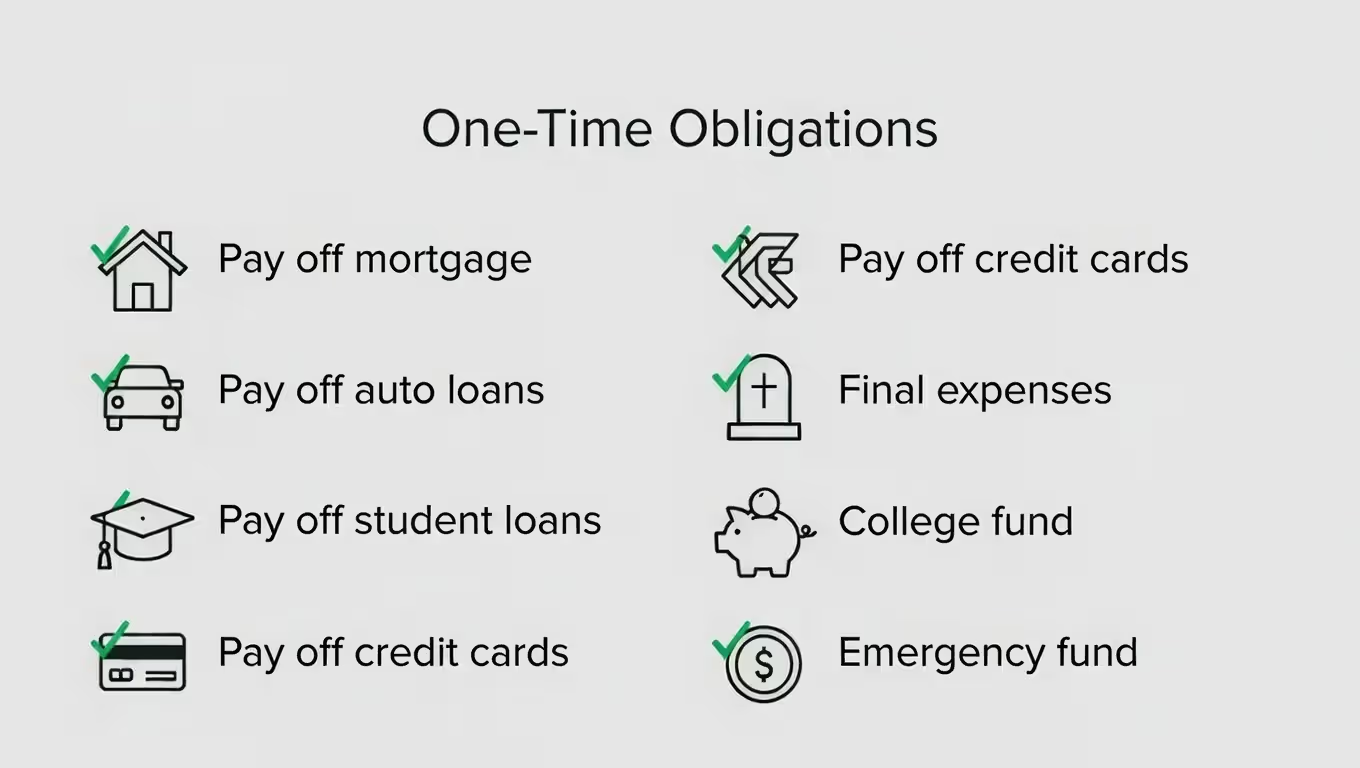

Debt and Expense Coverage: What Your Policy Must Pay Off

Author: Christopher Baldwin;

Source: everymuslim.net

Your life insurance should eliminate debts that would otherwise burden your family. Debt coverage planning means identifying every obligation that wouldn't disappear with you—and most of them won't.

Mortgage lenders don't forgive balances when borrowers die. Neither do student loan servicers (except for federal loans), auto finance companies, or credit card issuers. Your family inherits these obligations unless your policy pays them off.

Beyond debt, consider expenses that arise from your death: funeral and burial costs average $7,000-$12,000, and estate settlement can add several thousand more. If you have young children, college expenses loom 10-15 years ahead. Current estimates suggest $100,000-$150,000 per child for four years at a public university, more for private schools.

Here's a comprehensive breakdown of what to include in family expense analysis:

| Expense Type | Typical Amount Range | Priority Level | Calculation Notes |

| Mortgage balance | $150,000-$400,000 | High | Use current payoff amount, not monthly payment |

| Auto loans | $15,000-$45,000 | High | Total remaining balance on all vehicles |

| Student debt | $20,000-$100,000+ | High | Federal loans may be discharged; private loans typically aren't |

| Credit cards | $5,000-$20,000 | Medium | Average household carries $6,000-$8,000 |

| Child education (per child) | $50,000-$150,000 | Medium-High | Depends on public vs. private, in-state vs. out-of-state |

| Final/burial expenses | $7,000-$15,000 | High | Can be higher with religious or cultural requirements |

| Emergency fund replacement | $15,000-$50,000 | Medium | 6-12 months of expenses for transition period |

Add these categories together for your baseline debt coverage. A family with a $280,000 mortgage, $35,000 in auto and student loans, $8,000 in credit cards, two children they want to send to college ($200,000 total), and $10,000 for final expenses needs roughly $533,000 just to clear obligations and fund education.

This number doesn't include ongoing living expenses—it's purely the one-time costs and debts your policy should eliminate. You'll add income replacement on top of this figure.

One commonly overlooked item: If you own a home with a surviving spouse, should the policy pay off the mortgage or just cover payments for a period? Paying it off provides security and reduces monthly obligations. Keeping the mortgage and investing the insurance proceeds might generate better returns. The choice depends on your spouse's financial sophistication and emotional comfort with investment risk during grief.

The DIME Formula vs. Human Life Value: Comparing Popular Calculation Methods

Different coverage calculation methods emphasize different aspects of your financial life. Understanding the trade-offs helps you choose the right approach—or combine elements from several.

DIME Formula stands for Debt, Income, Mortgage, and Education. You add your total debt, multiply your annual income by the years you want to replace it, include your mortgage balance (yes, it's counted twice for emphasis), and add estimated education costs for all children. If you have $50,000 in debt, earn $80,000 (want 15 years = $1.2 million), have a $250,000 mortgage, and need $150,000 for two kids' college, your DIME total is $1.65 million.

Human Life Value takes a different angle: What's the present value of your future earnings? If you're 35, earn $90,000, and plan to work until 65, that's 30 years of income. Accounting for salary increases, inflation, and discounting future earnings to present value, you might calculate $1.8 million. This method treats your earning power as an asset your family loses.

Income Replacement Rule focuses purely on replacing your take-home pay for a specific period, as discussed earlier. It's simpler than Human Life Value because it doesn't project your entire career.

Needs Analysis is the most comprehensive approach. You itemize every expense, debt, and goal, then calculate the lump sum required to fund all of them. This is what financial planners typically use because it's customized to your situation.

Simple Multiplier (like 10x salary) requires no calculation beyond multiplication. Its advantage is speed; its limitation is accuracy.

Here's how these methods compare:

| Method | Best For | Complexity | Typical Result Range | Key Advantage | Main Limitation |

| Income Replacement Rule | Single-income families | Low-Medium | $500K-$2M | Easy to understand and calculate | Doesn't explicitly address debts |

| DIME Formula | Families with mortgages and kids | Low | $750K-$2.5M | Covers major expense categories | Double-counts mortgage, may overestimate |

| Human Life Value | High earners, young families | Medium-High | $1M-$4M+ | Captures full earning potential | Can produce very high numbers |

| Needs Analysis | Complex financial situations | High | Varies widely | Most accurate and personalized | Time-consuming, requires detailed info |

| Simple Multiplier | Quick estimates only | Very Low | $400K-$1.5M | Fast and easy | Ignores personal circumstances |

Most people benefit from running two or three calculations and comparing results. If DIME gives you $1.5 million and income replacement suggests $1.3 million, you're in the right ballpark. If one method says $800,000 and another says $2.2 million, dig deeper to understand why they diverge.

The right answer for your policy sizing guide lies somewhere in this range, adjusted for factors these formulas don't fully capture.

7 Personal Factors That Change Your Coverage Needs

Author: Christopher Baldwin;

Source: everymuslim.net

Generic formulas provide a foundation, but these variables can significantly increase or decrease your actual needs based insurance requirements:

1. Number and Age of Dependents

Three children under age 10 need 15+ years of support. One teenager needs 5-8 years. Each child adds $100,000-$200,000 to your coverage needs when you factor in basic expenses, activities, and education. The gap between children matters too—if your youngest is born when your oldest is 15, you're supporting dependents for 7 more years than a family with closely-spaced children.

2. Spouse's Income and Career Stability

A spouse earning $85,000 in a secure profession needs less insurance on you than a spouse earning $30,000 in an unstable field. But also consider: Could your spouse maintain their current career without you? If you handle childcare that enables their work schedule, your death might force them to reduce hours or switch jobs. This hidden economic contribution should increase your coverage.

3. Existing Savings and Investments

Every dollar in savings is a dollar less insurance you need. If you've accumulated $400,000 in retirement accounts, investment portfolios, and emergency funds, you can reduce your coverage by that amount (though some planners suggest keeping those funds separate for their intended purpose). Just remember: retirement accounts may face penalties or taxes if accessed early, reducing their effective value for immediate needs.

4. Health Conditions and Family Medical History

Chronic conditions in your family might mean higher future healthcare costs your spouse would face alone. If your employer-provided health insurance is significantly better than what your spouse could get independently, add $50,000-$100,000 to cover the gap until they can find comparable coverage. This factor affects family expense analysis more than most people realize.

5. Business Ownership or Partnership Agreements

Business owners face unique considerations. Do you have a buy-sell agreement? Your policy might need to fund a business buyout so your family receives fair value for your ownership stake. Partnership agreements often require specific coverage amounts. If your business depends heavily on your personal expertise or relationships, your family might receive little value from it—you'll need more insurance to compensate.

6. Lifestyle and Standard of Living Goals

Some families want to maintain their exact current lifestyle; others accept that the surviving spouse might downsize or adjust. There's no wrong answer, but be honest about expectations. Maintaining a $120,000 annual lifestyle requires substantially more coverage than adjusting to $80,000. Your policy should reflect the actual standard of living you want to protect, not an idealized or minimized version.

7. State of Residence and Cost of Living

$1 million in coverage means something different in rural Mississippi than in San Francisco. If your family might relocate after your death—say, moving closer to extended family—consider the cost of living in that location. Conversely, if your mortgage is the main expense keeping you in a high-cost area, your family might move somewhere cheaper, reducing their needs.

Run your calculations with these factors in mind. A family with young children, single income, significant debt, and high cost of living might need 20x the coverage of a dual-income couple with no kids, substantial savings, and low fixed expenses—even if both families have the same household income.

How to Calculate Your Number: A Step-by-Step Worksheet

Author: Christopher Baldwin;

Source: everymuslim.net

Now you'll put these concepts into practice with a systematic approach that produces a reliable coverage figure.

Step 1: Gather Your Financial Documents

You need current statements for: mortgage, auto loans, student loans, credit cards, investment accounts, retirement accounts, bank accounts, and recent pay stubs for all working household members. Also note your children's ages and your expected retirement age. This takes 20-30 minutes but ensures accuracy.

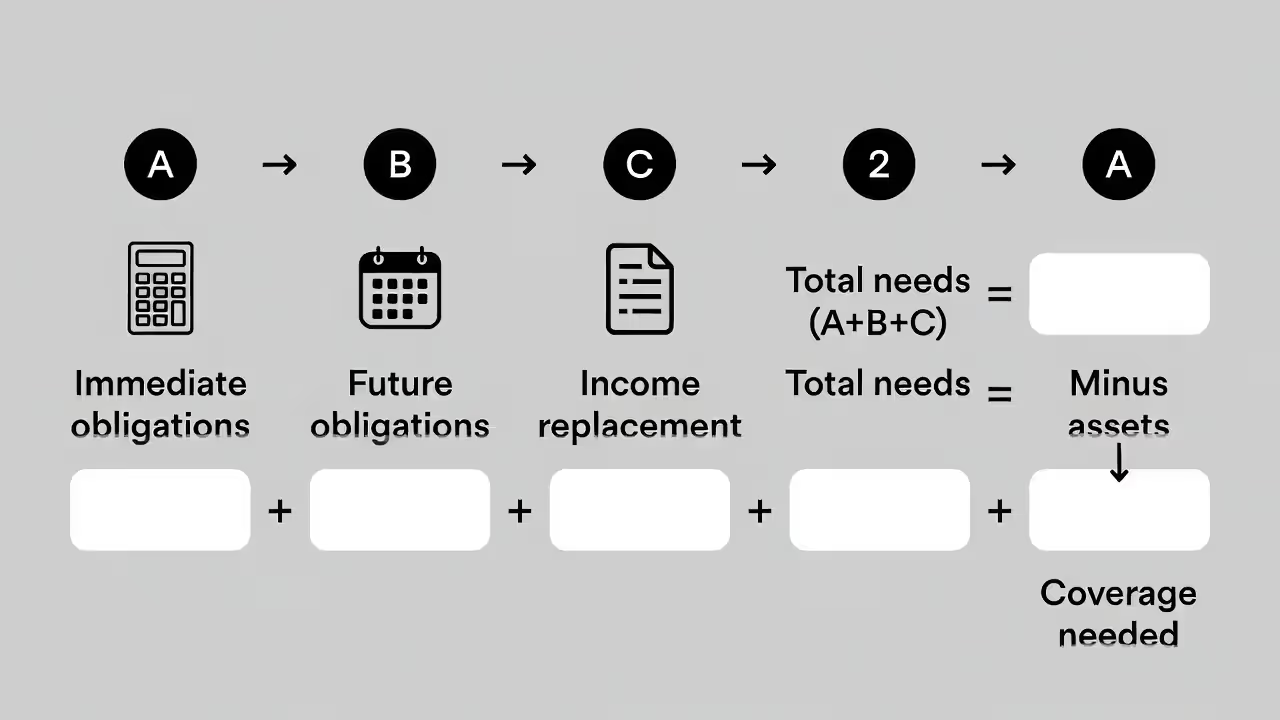

Step 2: Calculate Immediate Obligations

Add up debts you want paid off immediately: - Mortgage payoff: $_ - Auto loans: $_ - Student loans: $_ - Credit cards/personal loans: $_ - Final expenses: $_ (estimate $10,000 if unsure) - Subtotal A: $_

Step 3: Calculate Future Obligations

Estimate costs that arise later: - College funding ($ per child × number of children): $_ - Emergency fund (6 months of expenses): $_ - Subtotal B: $_

Step 4: Calculate Income Replacement

- Annual after-tax income to replace: $_

- Number of years to replace: _

- Multiply these: $_

- Adjust for investment returns: Multiply by 0.85 if you expect 2% real returns, or 0.90 for 1% real returns

- Subtotal C: $_

Step 5: Add Subtotals and Subtract Assets

- Total needs (A + B + C): $_

- Existing life insurance: $_

- Liquid savings/investments: $_

- Total assets: $_

- Your coverage gap: Total needs minus total assets

Real Example:

The Martinez family has a $310,000 mortgage, $28,000 in auto/student loans, $6,000 in credit cards, and two children ages 6 and 9. They estimate $120,000 per child for college and $10,000 for final expenses. Maria earns $95,000 (takes home $71,000) and wants to replace 18 years of income. They have $85,000 in retirement accounts and $20,000 in savings.

- Immediate obligations: $310,000 + $28,000 + $6,000 + $10,000 = $354,000

- Future obligations: $240,000 (college) + $35,000 (emergency fund) = $275,000

- Income replacement: $71,000 × 18 × 0.85 = $1,086,300

- Total needs: $1,715,300

- Existing assets: $105,000

- Coverage needed: $1,610,000

Maria would likely purchase a $1.5 million or $1.75 million policy, rounding to standard coverage increments.

Common Mistakes That Lead to Under-Insurance:

- Using gross income instead of take-home pay (overestimates what you need)

- Forgetting to subtract existing assets (overestimates)

- Not accounting for the services a non-working or lower-earning spouse provides (underestimates)

- Assuming Social Security survivor benefits will cover more than they actually do (underestimates)

- Failing to update calculations after major life changes (underestimates over time)

When to Round Up vs. Exact Figures:

If your calculation produces $1,340,000, should you buy $1.25 million, $1.5 million, or $1.75 million? Consider these factors:

Round up if: You have young children, expect income growth, anticipate major expenses not yet in your calculation, or want extra cushion for unexpected costs.

Round to exact increments if: Your calculation already includes conservative estimates, you're balancing coverage with affordability, or you plan to supplement with additional policies later.

Most term life insurance policies come in $250,000 increments. The premium difference between $1.25 million and $1.5 million might be $20-$40 monthly—often worth the extra protection.

Frequently Asked Questions About Life Insurance Coverage Amounts

Calculating life insurance needs isn't about finding a perfect number—it's about understanding the financial gap your death would create and filling it adequately. The methods outlined here give you multiple ways to estimate that gap, each highlighting different aspects of your financial life.

Start with the approach that fits your situation best. Families with straightforward finances might find the DIME formula sufficient. Those with complex situations benefit from detailed needs analysis. Running multiple calculations provides a reality check—if three methods cluster around $1.2-$1.5 million, you've found your range.

Remember that your coverage needs change over time. The $2 million policy that's essential when you have a new baby and a fresh mortgage becomes less critical 25 years later when your kids are independent and your house is paid off. Term insurance aligns well with this reality, providing maximum coverage during maximum-need years without lifetime premium commitments.

The worst outcome isn't buying slightly too much or too little insurance—it's buying none at all or so little that your family faces financial hardship. If your calculation suggests $1.3 million but you can only afford $1 million right now, buy the $1 million. You can always add coverage later as your income increases.

Work through the step-by-step worksheet, plug in your actual numbers, and you'll have a defensible coverage amount based on your real obligations and goals. That's infinitely better than guessing or relying on a one-size-fits-all rule that fits almost no one.