Decreasing Term Life Insurance: A Complete Guide for Debt-Focused Buyers

Decreasing Term Life Insurance Guide

Content

When life insurance gets designed specifically to match shrinking debt, you get a policy where payouts drop year after year—but your monthly bill stays identical. That's the core concept behind this specialized coverage.

Unlike standard term policies maintaining one fixed payout through their entire lifespan, these products follow a preset reduction schedule. The benefit might decrease every year, every month, or match your actual loan amortization. Eventually it hits zero when the term expires.

Why would anyone want insurance that becomes less valuable over time? Because most debt works exactly that way. Borrowed $350,000 for your house? That balance shrinks with every mortgage payment you make. Your coverage can shrink alongside it, which significantly reduces what you'll pay versus keeping a static benefit amount.

Common policy lengths include 10, 15, 20, or 30-year terms. Take a 30-year version starting at $400,000. Year one ends, your death benefit might sit at $380,000. Year two finishes, maybe you're at $360,000. The reduction continues automatically. Some policies drop the same dollar amount annually (linear reduction). Others follow mortgage-style amortization where benefits decline faster initially.

Your premium never changes. Month one costs the same as month 348, despite dramatically different coverage amounts. Buyers on fixed budgets appreciate this predictability, though you'll eventually pay equal prices for substantially less protection.

The Mechanics Behind Declining Coverage

Author: Christopher Baldwin;

Source: everymuslim.net

You pick an initial benefit amount and how many years you need coverage. The insurance company runs your age, health status, and coverage amount through their pricing models. That calculated premium gets locked in.

Your policy contract spells out exactly how benefits decline. Die during year five of a 20-year policy that started at $250,000 with linear reduction? Your beneficiaries might collect $187,500. Make it to year 15, that figure could sink to $62,500. Exact amounts depend on whether your contract uses equal annual reductions or follows an amortization schedule (which frontloads the decreases).

These policies run on autopilot—you don't trigger the benefit reductions. No notifications arrive when your coverage drops another notch. Some insurance companies mail annual statements showing current death benefits, but many skip this unless you specifically ask.

Term lengths typically mirror common borrowing periods. The 15 and 30-year options align perfectly with standard mortgages. A 10-year term works if you're covering auto loans or shorter business debts. Twenty-year terms fit buyers who made substantial down payments or refinanced.

Because the death benefit continuously shrinks, premiums run 15–40% below comparable level term policies. A healthy 35-year-old might spend $28 monthly for 20-year coverage starting at $200,000. That same person buying level term with identical starting coverage could pay $38–$42.

Practical Applications: Mortgages and Other Declining Debts

Matching Insurance to Your Home Loan

New homeowners make up the biggest customer segment for this insurance type. Sign a 30-year mortgage for $350,000, and your remaining balance drops with each payment made. A policy that mirrors this reduction protects your family's ability to pay off the house completely, without overpaying for unnecessary coverage.

The alignment works beautifully with fixed-rate mortgages. Currently owe $280,000? In three years you'll owe approximately $240,000. Insurance declining at the same rate delivers appropriate protection. Your survivors get enough money to eliminate mortgage debt entirely, letting them stay in the home without monthly payments.

Adjustable-rate mortgages mess up this clean math. Interest rates spike, your balance reduction slows down, but insurance keeps declining on the original schedule. A policy built around 4% interest assumptions won't track properly when you're actually paying 6.5%.

Refinancing causes similar problems. You bought a policy in 2020 aligned with a $300,000 mortgage. Four years later, you refinance for better rates, which resets your amortization schedule. Your insurance continues following the original decline schedule while your actual mortgage balance now exceeds what the policy anticipated.

Author: Christopher Baldwin;

Source: everymuslim.net

Other Borrowing Situations Where This Works

Business loans often follow predictable repayment schedules that suit this coverage style. A $150,000 SBA loan with a seven-year term decreases monthly. The right policy protects your business partner or family from inheriting that obligation if you die before it's repaid.

Co-signed student loans create lasting obligation for parents or relatives. When the primary borrower dies, the co-signer becomes responsible for the balance. A 10-year policy starting at $75,000 covers private student loans that don't automatically discharge upon death.

Car loans and personal loans theoretically work, but the small amounts rarely justify separate insurance policies. A $30,000 auto loan paid across five years costs less to cover through emergency savings than through premiums, fees, and underwriting processes.

HELOCs (home equity lines of credit) don't fit this model. You might borrow $50,000, pay down to $20,000, then borrow another $40,000. That unpredictable balance makes aligning insurance coverage impossible.

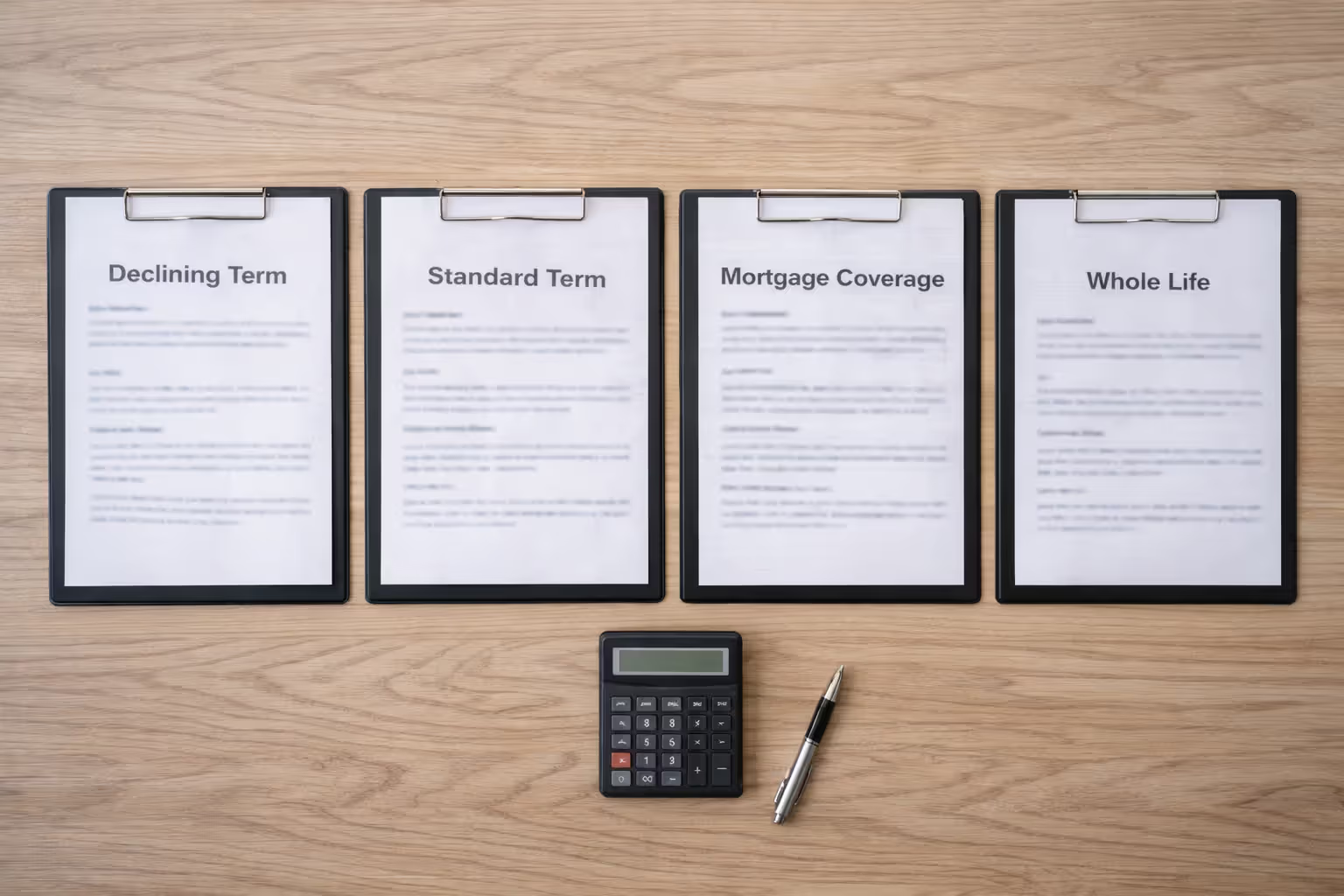

Premium Costs: Four Policy Types Compared Side-by-Side

| Product Category | How Benefits Change | Typical Monthly Cost* | Who Controls the Money | Adjustment Options Available |

| Declining Term | Shrinks yearly following predetermined schedule | $24–$32 | Beneficiary decides how to spend it | Zero—reductions happen automatically, can't be stopped |

| Standard Term | Stays at original amount for entire term | $35–$45 | Beneficiary decides how to spend it | May reduce coverage; certain policies permit increases after re-underwriting |

| Lender-Sold Mortgage Coverage | Tracks exact mortgage balance | $40–$55 | Zero—money goes straight to mortgage company | Zero—exclusively covers that specific mortgage |

| Permanent Whole Life | Grows over time while building cash reserves | $285–$350 | Beneficiary controls death benefit; policyholder can access cash value | Can modify premiums and death benefit; take loans against accumulated cash |

*Estimates for $250,000 starting coverage, healthy 30-year-old non-smoker, 20-year term

Author: Christopher Baldwin;

Source: everymuslim.net

Premium differences shrink as applicants get older. A 50-year-old might pay $78 monthly for declining coverage versus $92 for level term—a smaller percentage gap because mortality risk climbs with age, making the reducing benefit less valuable to insurers.

Standard term policies deliver more versatility. Pay off your mortgage early through an inheritance or windfall? You still own a policy with substantial remaining value. You can maintain it, convert it to permanent insurance, or potentially sell it through the life settlement market if the benefit is large enough.

Mortgage life insurance—sold by lenders or their affiliated companies—costs more than either term option while offering less control. Death benefits get paid directly to your mortgage company, not to your beneficiaries. If your home is worth $450,000 and you owe $180,000, the insurance pays that $180,000 to the lender while your family figures out their housing situation. A declining term policy puts $180,000 cash in your beneficiaries' hands to use however they want—paying the mortgage, relocating to a smaller place, or investing the difference.

Five Critical Errors When Selecting Declining Coverage

Aligning the reduction schedule with the wrong debt. Buyers assume their policy should mirror their mortgage balance, then select a linear decline schedule. But most mortgages use amortization tables where early payments mostly cover interest. Your balance drops slowly initially, then accelerates later. A linear insurance decline leaves you underinsured during early years and overinsured later on.

Forgetting about other financial obligations. Your mortgage isn't your only debt. When you die, your family still faces final expenses, credit card balances, car payments, and daily living costs. A policy that exactly matches your mortgage leaves nothing for these expenses. Smarter to start with coverage 20–30% above your mortgage balance, accepting slight overinsurance as the loan matures.

Purchasing from your mortgage lender. Lenders offer convenience—sign up during your home closing—but their policies cost 30–60% more than identical coverage from independent insurers. The application might be simpler, but you'll spend thousands extra across 20 or 30 years. Invest two hours getting quotes from three independent insurers instead.

Assuming you can't qualify for better coverage. Maybe you've got high blood pressure or family history of heart disease. You figure declining coverage is your only affordable choice. Many applicants with health issues qualify for standard term at reasonable rates, especially when conditions are well-managed. Get quotes for both policy types before deciding cost forces you into declining coverage.

Not accounting for inflation. Your $250,000 policy might cover your mortgage perfectly today. Fifteen years from now, $250,000 won't buy what it does today. Your family might pay off the house but struggle affording property taxes, insurance, and maintenance on diminished purchasing power. This isn't a dealbreaker for declining term, but it is a reason to consider slightly higher initial coverage.

Ideal Candidates (and Who Should Look Elsewhere)

Young homeowners with tight budgets benefit most. A 28-year-old couple buying their first home needs life insurance but operates on minimal discretionary income. Declining term delivers meaningful protection at rock-bottom prices, guaranteeing the surviving spouse can keep the house if tragedy strikes.

Single-income families face concentrated financial risk. When one spouse generates all or most household income, their death creates instant financial crisis. The surviving spouse must cover the mortgage, childcare, and daily expenses without that income stream. A policy aligned with the mortgage eliminates the largest fixed expense, buying time to adjust financially.

Business partners carrying loans benefit from this loan aligned insurance when one partner's death could stick the survivor with the full debt. A $200,000 business loan taken jointly becomes one person's problem if the co-borrower dies. Coverage declining with the loan balance protects the surviving partner without paying for unnecessary insurance.

Older buyers purchasing smaller homes might prefer this strategy. A 55-year-old downsizing to a $180,000 condo with a 15-year mortgage doesn't need permanent coverage. A declining policy covers the debt at minimal cost, expiring right when the mortgage does.

Who should skip this coverage? Anyone needing insurance beyond simple debt protection. Want to leave an inheritance, fund your children's education, or provide long-term income replacement for your spouse? Level term or permanent insurance makes more sense. This affordable term option only works when your primary goal centers on debt elimination.

People with irregular income streams—freelancers, commission-based salespeople, small business owners—face unpredictable debt payoff timelines. You might make extra mortgage payments some years and minimum payments others. Your insurance declines on schedule regardless of your actual balance, creating potential coverage gaps.

Those planning to relocate shouldn't tie insurance to a specific mortgage. If you'll likely sell your home within five to seven years, you need flexible coverage that moves with you. Standard term policies provide that flexibility; declining coverage becomes worthless once you no longer carry the debt it was designed to cover.

This insurance type makes sense for exactly one scenario: you carry a specific, predictable debt that declines over time, and your primary insurance goal centers on eliminating that debt if you die. The moment your situation involves any other financial objective—income replacement, wealth transfer, education funding—you need a different tool. Too many buyers choose it purely because it's cheap, then realize ten years later they needed actual financial protection, not just debt coverage.

— Jennifer Hartmann, CFP®, Hartmann Financial Planning

The Purchase Process: Applications Through Approval

Start by calculating your actual coverage requirement. Pull your most recent mortgage statement and note your principal balance. Add 20–25% to cover final expenses and short-term family needs. That's your starting death benefit.

Select a term length matching your debt timeline. Got 23 years remaining on your mortgage? Buy a 25-year policy. Those extra two years cost little and prevent coverage from expiring before your loan does.

Collect quotes from at least three insurance companies. Premiums vary dramatically—sometimes 40% or more for identical coverage. Online quote tools provide rough estimates within minutes. Independent insurance agents can pull quotes from multiple carriers simultaneously.

Applications request information about your health history, lifestyle habits, and family medical background. Answer honestly. Misrepresenting your smoking status, health conditions, or risky hobbies can void your policy. Insurance companies verify information during underwriting and can contest claims when they discover misrepresentations.

Most applicants undergo a medical exam. A paramedical professional visits your home or office, collects blood and urine samples, records your height, weight, and blood pressure, then asks additional health questions. The appointment requires 20–30 minutes. Results get sent to the insurer's underwriting department.

Underwriting takes two to six weeks for straightforward cases. Healthy applicants with no red flags get approved quickly. Complicated medical histories, unclear test results, or incomplete applications extend the timeline. Some insurers offer accelerated underwriting for low-risk applicants, providing approval within 48–72 hours without medical exams.

Approval arrives with a rating class—preferred plus, preferred, standard plus, standard, or substandard. Your class determines your premium. A preferred plus rating might cost $26 monthly while standard costs $38 for identical coverage. You can accept the offer, negotiate if you disagree with the rating, or decline and try another insurer.

Author: Christopher Baldwin;

Source: everymuslim.net

Once approved, you'll receive policy documents. Read them carefully. Verify the death benefit, decline schedule, term length, and premium amount match what you applied for. You typically have 30 days to review the policy and cancel for a full refund if it's not what you expected.

Set up automatic payments. Missing premium payments can lapse your policy, and reinstating coverage requires new underwriting. Automatic bank drafts or credit card charges prevent accidental cancellation.

Common Questions About Declining Term Coverage

This coverage solves one specific problem exceptionally well: protecting your family from inheriting debt when you die. It accomplishes this efficiently and affordably, making it ideal for homeowners whose main concern centers on ensuring their mortgage gets paid off.

The trade-offs are real, though. You sacrifice flexibility, your coverage becomes worth less annually while premiums stay flat, and you can't adapt the policy when circumstances change. For some buyers, these limitations barely matter. For others, they're dealbreakers making standard term insurance worth the extra monthly cost.

Calculate what you actually need. If debt elimination truly represents your primary goal and you're confident your financial situation won't require adjustments, declining term delivers excellent value. Need versatile coverage serving multiple purposes over time? Spend slightly more for a policy that won't shrink when you might need it most.