Survivorship Life Insurance: How Second-to-Die Policies Work for Estate Planning

Survivorship Life Insurance

Content

Got a sizable estate and wondering how your kids will handle the tax bill? Here's the thing: if you and your spouse have built up serious wealth—real estate, retirement accounts, maybe a business—Uncle Sam wants his cut when you're both gone. Right now, federal exemptions sit at $13.61 million per person ($27.22 million total for couples), but that drops to around $7 million in 2026. Unless lawmakers step in, millions of families will suddenly owe estate taxes.

Second-to-die life insurance tackles this problem differently than regular policies. Instead of paying out when the first spouse dies, it waits until both of you have passed. Why does this matter? Because married couples typically don't face estate taxes at the first death—assets roll over tax-free to the surviving spouse. The tax man shows up after the second funeral, and that's exactly when this coverage kicks in.

Sounds straightforward, but here's where it gets interesting. These policies cost 30-40% less than buying two separate policies because insurers bet on two people living, not one. The catch? You're locked in together, which creates some weird situations (divorce, anyone?). Before you sign up, you need to figure out if your specific situation—your assets, your state's tax rules, your family dynamics—actually benefits from this approach.

What Makes Survivorship Life Insurance Different from Traditional Policies

Standard life insurance pays when one person dies. Survivorship insurance covers two people—usually a married couple—but the check doesn't arrive until the second person passes away. That's it. That's the core difference, and everything else flows from this timing shift.

Think about how married couples handle estate taxes. When your spouse dies, federal law lets you inherit everything without paying a dime in estate taxes (the unlimited marital deduction). Taxes only bite after both of you are gone. Joint life coverage lines up perfectly with this timeline—it delivers cash precisely when your heirs need to write that check to the IRS.

Here's why these policies cost less: insurance companies deal with extended timelines. If both spouses are 60, they might collect premiums for 25 or 30 years before paying any claims. That's a lot of time to invest your premium payments. Compare that to insuring one 60-year-old, where the payout might come in 15-20 years. Longer collection periods mean lower annual costs—sometimes you'll pay 35% less than buying two individual policies with the same total death benefit.

Author: Olivia Ramsey;

Source: everymuslim.net

Underwriting gets interesting when two people are involved. Let's say you're healthy as a horse but your spouse has diabetes. With separate policies, your spouse would get hammered with high premiums or might not qualify at all. But with joint coverage, insurers blend both health profiles together. Your good health offsets your spouse's condition, and you both get covered at reasonable rates. It's risk-averaging in action.

Most survivorship policies come as permanent insurance—whole life or universal life—rather than term coverage. Why? Because you can't predict when that second death happens. It might be 15 years from now, might be 40. You need coverage that lasts as long as you both do, which means paying for permanent protection. These policies also build cash value over time, letting you borrow against them if needed (though tapping that money reduces what your heirs eventually receive).

Who Benefits Most from a Second-to-Die Policy

Wealthy couples staring down estate taxes are the obvious candidates. If your combined net worth pushes past federal or state exemption limits, you're facing a 40% federal tax rate (plus whatever your state charges). That's a massive bill. Life insurance proceeds give your executor immediate cash to pay those taxes without selling the family cabin, liquidating the stock portfolio at a bad time, or forcing a fire sale of the business.

Parents of special needs kids find these policies invaluable. I'm talking about families with a child who'll need lifetime care and support. Both parents worry constantly: what happens when we're both gone? A second-to-die policy can fund a special needs trust that provides for your child indefinitely. The coverage activates right when both caregivers are no longer around—perfect timing. Plus, if structured correctly, the money doesn't disqualify your child from SSI or Medicaid benefits.

Family businesses create another compelling use case. Say you've built a successful manufacturing company and want your daughter to run it, but you've got two other kids who aren't involved in the business. How do you treat everyone fairly? One approach: leave the business to your daughter and use life insurance proceeds to give your other children equivalent cash inheritances. Nobody has to sell the company to split things up, and your daughter can keep operating without partners who don't want to be there.

Blended families deal with unique inheritance tensions. You've got kids from your first marriage, your spouse has kids from theirs. Who gets what? When does the surviving spouse control everything? A second-to-die policy with all the kids named as equal beneficiaries cuts through this mess. The insurance money gets divided exactly how you specify, avoiding arguments over who deserves what from the estate.

Charitable giving strategies also use these policies. Maybe you want to donate $2 million to your university but don't want to shortchange your children. Buy a survivorship policy with a $2 million death benefit naming your kids as beneficiaries. Make your charitable gift during life or through your estate, and the insurance proceeds replace that wealth for your children. Everyone wins—the charity gets funded, your kids get their inheritance.

How Joint Life Coverage Reduces Estate Tax Liability

Author: Olivia Ramsey;

Source: everymuslim.net

Federal estate tax starts at 40% once you exceed the exemption amount. Do the math on a $30 million estate when exemptions drop to $7 million per person in 2026: you're looking at $6.4 million owed to the IRS. Where does that money come from? If your wealth is tied up in real estate, business interests, or investment portfolios, your executor faces an ugly choice: sell assets quickly (usually at terrible prices) or negotiate payment plans with the government.

Life insurance death benefits solve the liquidity crunch. The check arrives 30-60 days after filing the claim. Your executor can pay estate taxes, cover final expenses, and settle the estate without touching illiquid assets. This matters especially for families whose wealth isn't sitting in cash—think farmers with valuable land but tight operating budgets, or business owners whose net worth is trapped in company equity.

Don't sleep on state estate taxes. Twelve states plus D.C. impose their own estate taxes, often with much lower exemption thresholds than federal rules. Oregon hits you at $1 million. Massachusetts at $2 million. If you live in Portland with a $3.5 million estate, you'll owe Oregon estate tax even though you're nowhere near federal limits. Middle-class families in these states get blindsided by tax bills they never saw coming.

Using ILITs to Maximize Tax Benefits

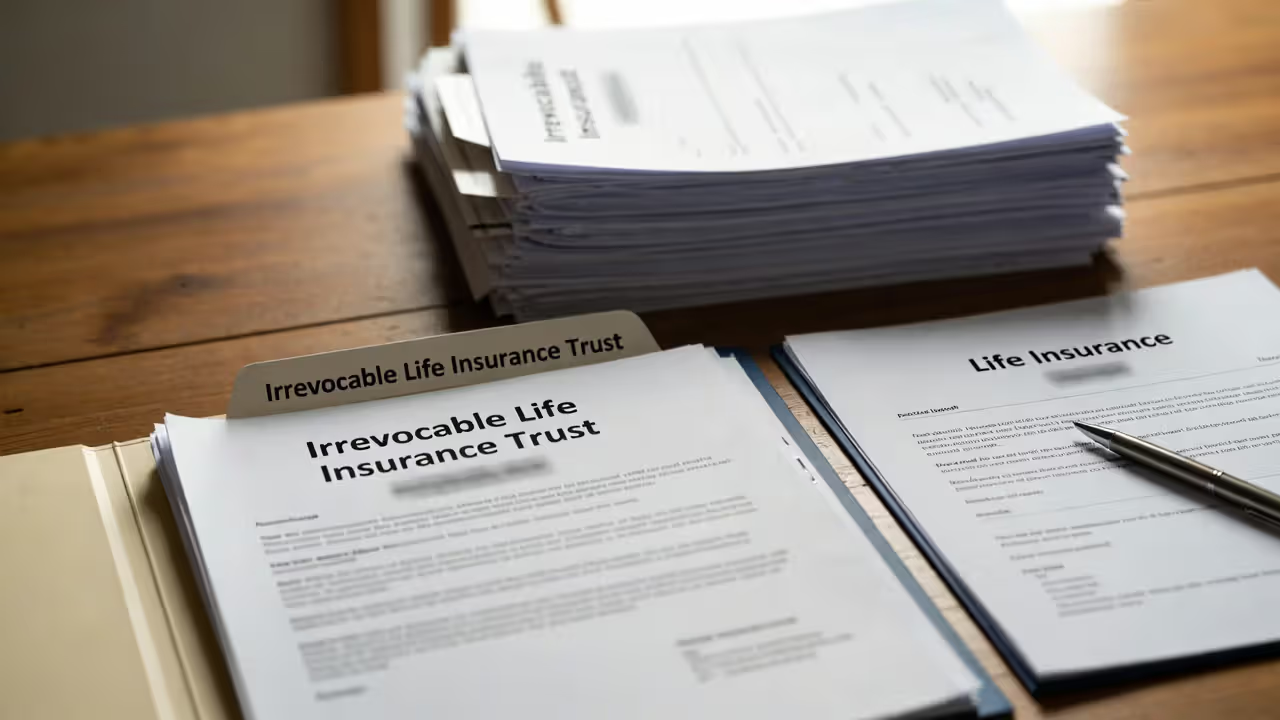

Here's a trap people fall into: they buy a survivorship policy to pay estate taxes, but they own the policy themselves. Guess what? The IRS counts that death benefit as part of your taxable estate, which increases the very tax bill you're trying to pay. Circular problem.

The fix is an irrevocable life insurance trust, or ILIT. This trust—not you—purchases and owns the survivorship policy. You transfer money into the trust each year to cover premiums (using annual gift exclusions of $18,000 per beneficiary in 2024). The trust owns everything, pays the premiums, and collects the death benefit when you're both gone. Since neither spouse owns the policy at death, the IRS can't include those proceeds in your taxable estate.

The downside? You lose control permanently. "Irrevocable" means you can't change your mind, reclaim the policy, or redirect the money later. You'll also need to handle administrative requirements—specifically, Crummey notices that give beneficiaries temporary withdrawal rights each time you gift premium money. It's paperwork and process, but that's the price for keeping life insurance proceeds outside your estate.

Author: Olivia Ramsey;

Source: everymuslim.net

State Estate Tax Thresholds to Consider

Seventeen jurisdictions charge their own estate or inheritance taxes. Here's what you're dealing with: Connecticut taxes estates above $13.61 million. Hawaii starts at $5.49 million. Illinois hits you at $4 million. Maine's threshold sits at $6.41 million, Maryland at $5 million. Massachusetts and Oregon have the lowest exemptions—$2 million and $1 million respectively.

Minnesota taxes estates exceeding $3 million. New York's exemption is $6.94 million. Rhode Island starts at $1.73 million. Vermont at $5 million. Washington state charges tax above $2.193 million, and D.C.'s threshold is $4 million. Each state uses different tax rates and calculation methods, so you can't just apply federal planning strategies and expect them to work.

Portability—the ability to transfer one spouse's unused exemption to the other—varies by state. Massachusetts doesn't allow it, meaning a married couple gets $2 million in exemptions total, not $4 million. Without proper planning, you could lose one spouse's exemption entirely. Survivorship insurance provides funds to cover state taxes regardless of these technical rules.

Cost Factors: What Determines Your Premium

Age matters most. Buy at 50 and you might pay $8,000 yearly for $2 million in coverage. Wait until 70 and that same coverage costs $32,000 annually. Why the massive difference? Insurance companies expect to collect premiums much longer from younger couples. A 50-year-old couple might pay in for 30+ years before the second death occurs, while a 70-year-old couple gives the insurer maybe 15-20 years.

Health underwriting considers both lives as a package deal. If one of you is exceptionally healthy and the other has some manageable conditions (high blood pressure, elevated cholesterol), the combined risk assessment usually produces better rates than the less healthy spouse could get individually. But if both of you have serious health issues—heart disease, cancer history, diabetes with complications—the combined risk might make coverage unaffordable or get your application declined outright.

Whole life versus universal life creates different cost structures. Whole life charges fixed premiums that never change and guarantees the death benefit as long as you pay. You know exactly what you'll pay every year forever. Universal life offers flexibility—you can adjust premiums and death benefits—but that flexibility comes with risk. If the policy's cash value doesn't grow as projected (because interest rates dropped or the insurer's performance lagged), you might face surprise premium increases or even policy lapse. Guaranteed universal life splits the difference: lower premiums than whole life, with guarantees that your coverage won't lapse if you pay the contractually required minimum.

Death benefit size scales premiums proportionally, but not exactly linearly. Double your coverage from $1 million to $2 million and your premium might increase by 90-95%, not a full 100%. Insurers spread fixed administrative costs across the policy, so larger death benefits become slightly more efficient per dollar of coverage.

Cost Comparison: Joint vs. Separate Policies

| Couple's Age | Joint Policy $1M Death Benefit | Two Separate $500K Policies | You Save Annually |

| Both age 50 | $8,200 | $11,800 | $3,600 (31% less) |

| Both age 60 | $15,400 | $23,200 | $7,800 (34% less) |

| Both age 70 | $32,100 | $49,500 | $17,400 (35% less) |

These figures assume non-smoking couples in good health seeking permanent coverage; your actual quotes will vary based on insurer, underwriting class, and policy type.

Author: Olivia Ramsey;

Source: everymuslim.net

Common Mistakes When Buying Estate Planning Insurance

Most couples calculate their death benefit based on what their estate is worth today, completely forgetting that assets grow. Your $5 million estate will likely hit $10-12 million over the next 20-30 years from appreciation, especially if you own real estate or equities. That future growth creates a bigger tax bill than you're planning for. Smart move? Buy 25-30% more coverage than your current estate tax calculation suggests you need.

Ownership structure errors wreck the entire strategy. If you own the policy in your own name, maintain control over beneficiary changes, or keep any "incidents of ownership," the IRS includes the death benefit in your taxable estate. You just increased the problem you're trying to solve. Setting up an ILIT from day one prevents this, but many people buy coverage first and try to fix ownership later—which triggers a three-year lookback rule where the IRS counts the death benefit in your estate if you die within three years of transferring the policy out of your name.

Death benefit calculations often focus narrowly on estate tax while ignoring everything else your executor needs to pay. Estate settlement isn't just about taxes. There are executor fees (typically 2-5% of the estate), attorney costs, accounting expenses, court fees, outstanding debts, and final medical bills. A $2 million death benefit might cover your estate tax liability, but what about the other $300,000 in settlement costs? Now your heirs are scrambling for cash anyway.

Nobody reviews their policies after purchase. You bought coverage 15 years ago—great. But has your estate grown? Have tax laws changed? Did you move to a state with different estate tax rules? Is your universal life policy's cash value growing as projected, or do you need to increase premium payments? Reviewing every 3-5 years catches these problems before they become crises. Universal life policies especially require monitoring since poor investment performance can cause premium hikes or even lapse the policy entirely.

Your survivorship policy needs to work alongside trusts, gifting strategies, business succession plans, and charitable giving—not operate in isolation. I've seen situations where someone's life insurance beneficiaries contradict their trust provisions, or where the death benefit pays into an estate that's already liquid enough, missing opportunities to fund charitable bequests instead. Have an estate attorney review how insurance proceeds flow through your overall plan to make sure everything coordinates properly.

How to Evaluate If Inheritance Planning with Life Insurance Makes Sense

Start by calculating what you'll actually owe. Add up your house, retirement accounts, brokerage accounts, business interests, and any existing life insurance. Subtract the applicable exemption ($13.61 million federal currently, but check what your state allows—might be only $2 million). Multiply what's left over by the tax rate (40% federal, plus your state's rate). That's your estate tax bill. If that number makes you wince and you don't have enough liquid assets to cover it, survivorship insurance deserves serious consideration.

Compare this against other wealth transfer strategies. You could gift $18,000 per person annually ($36,000 per couple) to each of your children using annual gift tax exclusions. A couple with four kids can move $144,000 out of their estate every year tax-free. Do that for 20 years and you've transferred $2.88 million. But you need 20 years, the discipline to gift consistently, and you have to live long enough to complete the strategy. Die early and you haven't moved enough assets.

Charitable remainder trusts let you donate appreciated stock, receive income for life, and reduce estate taxes—but the principal goes to charity, not your kids. Family limited partnerships can create valuation discounts that reduce estate taxes on business interests or real estate, but they're expensive to set up ($15,000-30,000 in legal fees), require ongoing maintenance, and the IRS scrutinizes them heavily. Survivorship insurance offers simplicity: you pay premiums, you get a guaranteed death benefit, done.

Think about liquidity even if you don't owe estate taxes. Say your estate is worth $4 million, mostly tied up in a family farm. No federal estate tax, but settling your estate still requires cash—property taxes, operating expenses for 12-18 months during probate, maintenance costs, maybe buying out one sibling who doesn't want to farm. Where does that $200,000-300,000 come from without selling land? Life insurance provides cash that doesn't force asset sales.

Run a cost-benefit analysis. If you're 60 years old paying $15,000 yearly for 25 years, you'll spend $375,000 in premiums to deliver a $2 million death benefit. That's a 5.3x return. If you die sooner, the ratio improves dramatically. If you live to 100, you'll pay premiums for 40 years ($600,000 total), which lowers your return but still delivers $2 million guaranteed. Compare that certainty against investing the same $15,000 annually in the market at various assumed returns—and remember investment returns aren't guaranteed while the death benefit is.

These policies work best for clients who check three boxes: they face potential estate taxes, their wealth is tied up in illiquid assets, and they want to keep those assets intact for the next generation. This isn't an investment play—you're solving a specific problem at the lowest possible cost. When you place ownership in an irrevocable trust, you've created one of the few tools that delivers tax-free liquidity exactly when families need it most.

— Jennifer Martinez, CFP®, Martinez Wealth Advisors

Comparing Wealth Transfer Strategies

| Approach | Cash Created | Tax Reduction | Setup Difficulty | Can You Change It? | Works Best For |

| Survivorship Policy | Immediate lump sum | Pays tax bills (indirect) | Moderate (trust needed) | No (permanent) | Estates heavy in real estate or business, guaranteed liquidity |

| Annual Gifts | Reduces estate over time | Removes growing assets | Simple | Yes (adjust yearly) | Long planning horizons, liquid portfolios |

| Charitable Trust | Income during life | Asset removal plus deduction | Complex (attorneys, admin) | No (locked in) | Philanthropic goals, appreciated securities |

| Family Partnership | Assets stay in family | Valuation discounts | Very complex (formation, upkeep, IRS risk) | Somewhat | Operating businesses, rental properties |

Frequently Asked Questions About Survivorship Life Insurance

Survivorship life insurance fills a specific role in estate planning: it creates guaranteed cash to pay estate taxes and settlement expenses without forcing your heirs to dump assets at fire-sale prices. For couples with taxable estates, wealth tied up in illiquid assets, or children needing special support, second-to-die policies offer efficient coverage at substantially lower costs than separate policies. The death benefit shows up precisely when needed—after both spouses have died—and when properly placed in an ILIT, the proceeds avoid adding to your taxable estate.

These policies aren't right for everyone. If your estate falls comfortably below exemption limits, you've got plenty of liquid assets already, or you need first-to-die coverage to replace lost income for a surviving spouse, regular life insurance makes more sense. Survivorship coverage works when your main concern is transferring wealth to the next generation and handling the estate tax bill, not supporting a surviving partner.

Before buying, calculate your real tax exposure, evaluate alternative strategies, and make sure the coverage integrates with your complete estate plan. Work with professionals who can model different scenarios and get the ownership structure right from the start. A well-designed survivorship policy, properly maintained, gives you confidence that your wealth will pass to heirs smoothly regardless of future tax law changes or market volatility.