How Life Insurance Payout Works: From Claim to Beneficiary Payment

Life Insurance Payout Explained

Content

Your uncle passes away, and his attorney mentions you're the beneficiary on a $250,000 policy. Now what? You've never done this before. The policy document is eight pages of dense text, and you're not even sure which company issued it.

Here's what actually happens between that initial phone call and money hitting your bank account—and the choices you'll make that determine whether you see that cash in three weeks or three months.

The typical beneficiary waits 30-60 days for payment after submitting everything correctly. But "correctly" carries more weight than you'd think. Miss one signature, send a photocopy instead of a certified document, or select the wrong payout structure, and you've just added weeks to an already stressful situation.

Your decisions here ripple forward. Choose lump sum or monthly checks? Leave it with the insurance company temporarily or move it immediately? These aren't just administrative checkboxes—they reshape your financial life.

What Happens When a Policyholder Dies

Life insurers don't track deaths. No algorithm scans obituaries. No department monitors public records. They wait for you to tell them.

The Initial Notification Process

Three ways to start: call their 1-800 number, email the agent whose business card is stapled to the policy, or log into the insurer's website and click "File a Claim." Most companies answer within two rings—they've staffed up their death claims units since COVID showed them what happens during a mortality surge.

That first call takes about 15 minutes. They'll want the deceased's full legal name (including middle name—John Smith won't cut it if the policy says John Robert Smith), Social Security number, birthdate, death date, and policy number if you've got it. Missing the policy number? They'll find it anyway using the SSN.

Within 48 hours, you'll receive a claims packet. Some insurers email a PDF immediately. Others mail a physical packet that arrives in 3-5 days. This packet contains the official claim form—usually 3-4 pages—and a document checklist. A few companies now skip the packet entirely and let you upload everything through a secure portal, cutting a week off the process.

Progressive companies like Haven Life and Ladder email you a personalized link where you can track your claim status in real-time, similar to tracking a FedEx package. Traditional insurers still make you call for updates.

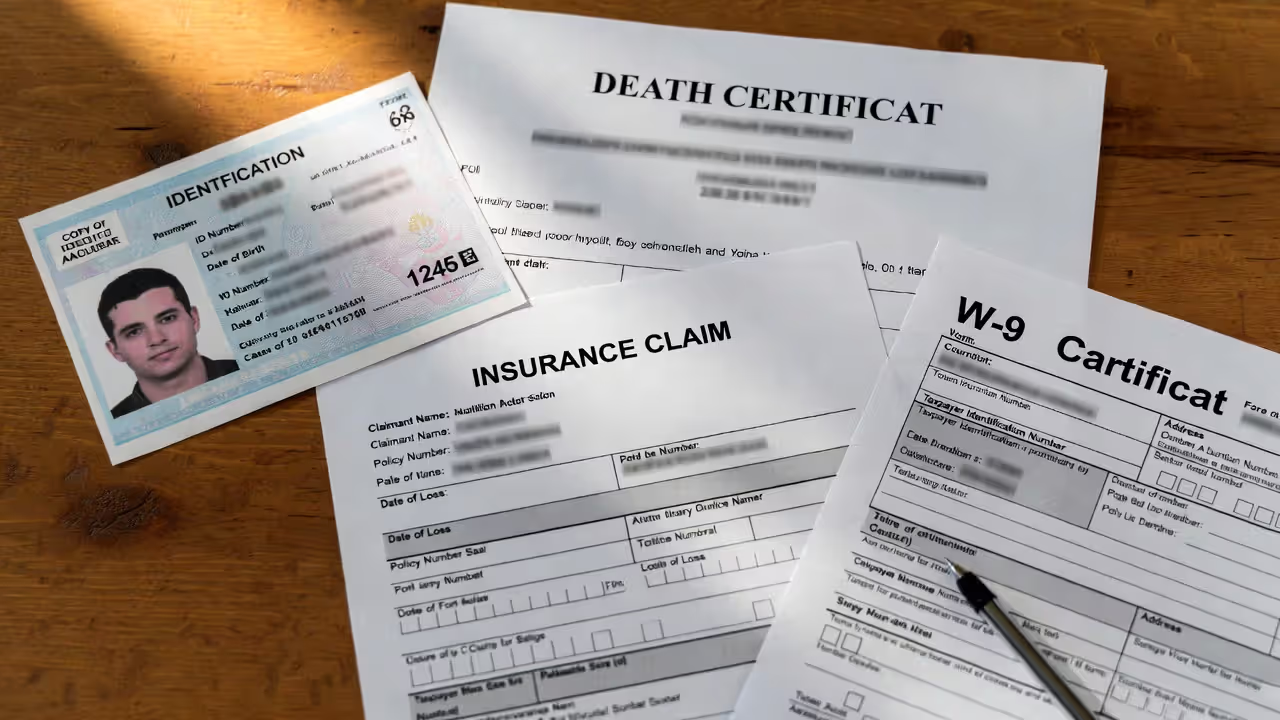

Documents Required to Start a Claim

Author: Olivia Ramsey;

Source: everymuslim.net

You need a certified death certificate with the raised seal. Not a photocopy. Not a faxed version. Not a photo you took with your phone. The actual certificate from the county recorder's office or funeral home, with that embossed stamp you can feel when you run your finger across it.

Order six copies when you're at the funeral home. You'll need them for banks, investment accounts, Social Security, and other insurance policies. Each copy costs $15-30 depending on your state. California charges $21. Texas charges $20. New York? That'll be $30 per copy.

Beyond the death certificate, gather:

- The completed claim form with every field filled in—blank spaces delay processing

- Your driver's license or passport proving you're actually the person named as beneficiary

- A W-9 form so the IRS knows who received the money

- The original policy if you can find it (though they'll process without it)

Policies issued within the past 24 months trigger extra scrutiny. Insurers call this the contestability window. They'll request medical records from every doctor the deceased visited in the past five years. They'll check prescription databases. They'll compare the application against what they find. Did your father check "no" for diabetes when he'd been taking Metformin for three years? Expect a delay while they investigate.

Accidental deaths require police reports. Overseas deaths need translated documents authenticated by the U.S. embassy. Suicides within two years? They'll want the coroner's report and full autopsy results.

How Insurance Companies Calculate Your Payout

That $500,000 face value on page one? It's a starting point, not a guarantee.

Face Value vs. Actual Payout Amount

The face value represents the baseline. A $500,000 term policy with paid-up premiums and no loans pays exactly $500,000 to beneficiaries. Simple math.

But riders change the calculation. An accidental death and dismemberment rider doubles the payout if death resulted from a covered accident—but "covered accident" excludes skydiving, motorcycle racing, and deaths during commission of a felony. Your brother's $300,000 policy might pay $600,000 if he died in a car crash, but only $300,000 if he crashed while street racing.

Author: Olivia Ramsey;

Source: everymuslim.net

Whole life policies add accumulated cash value to the death benefit, depending on the option selected at purchase. Option A (level death benefit) pays face amount plus cash value. Your mother's $200,000 whole life policy with $75,000 cash value pays $275,000. Option B (level amount at risk) pays just the $200,000 face value because cash value was already counted.

Return-of-premium term policies refund every dollar paid in premiums if the insured outlives the term. These policies cost 30-50% more than regular term, but beneficiaries get nothing extra if death occurs during the term—they're paying for that potential refund.

Policy Loans and Outstanding Premiums

Outstanding loans get subtracted first. Your sister borrowed $40,000 against her $250,000 whole life policy three years ago. She never repaid it. Interest accrued at 6% annually, adding about $7,200. Beneficiaries receive $202,800, not $250,000.

Unpaid premiums also come out of the death benefit. Universal life policies deduct monthly cost-of-insurance charges from the cash value automatically. If that cash value dropped to zero because premiums weren't paid, the policy might have lapsed without anyone noticing. The insurer sends annual statements showing the cash value balance, but most policyholders don't read them until it's too late.

Grace periods give you 30-31 days after the premium due date to catch up without losing coverage. Die during the grace period? Coverage still applies, but they'll subtract those unpaid premiums plus grace period interest from your death benefit.

Dividend accumulations increase the payout. Mutual insurance companies like Northwestern Mutual, MassMutual, and New York Life pay annual dividends that many policyholders leave on deposit with the insurer. These accumulations earn 4-6% interest and get added to the death benefit. A $300,000 policy might actually pay $340,000 after 20 years of accumulated dividends.

Death Benefit Payment Options: Choosing How You'll Receive Money

Lump sum isn't your only choice, though 87% of beneficiaries take it. The other five options create dramatically different financial outcomes.

Lump Sum Payment: Pros and Cons

One check. The full amount. In your account within 5-10 business days after approval.

You gain total control. Pay off your $180,000 mortgage immediately and save $95,000 in future interest. Invest with your own advisor who charges 0.75% instead of the insurance company's built-in fees. Buy that rental property you've been eyeing. Fund your daughter's medical school tuition without loans.

But here's what happens in real life: Northwestern University researchers tracked 300 lottery winners who received lump sums averaging $50,000. Within five years, 44% had spent everything and carried more debt than before they won. Life insurance beneficiaries follow similar patterns. That $400,000 feels infinite until your nephew asks for $15,000 to start a business, your daughter needs $35,000 for a wedding, and suddenly you're at $220,000 wondering where three years went.

The discipline problem hits hardest between ages 25-45. Younger beneficiaries lack experience managing large sums. They underestimate inflation. They overestimate investment returns. They say yes when they should say no.

Tax reporting starts immediately. The death benefit itself—$500,000 in this example—generates no income tax. But interest earned between the date of death (March 15) and the payment date (May 3) shows up as taxable income on Form 1099-INT. That might be $2,000-4,000 depending on the amount and delay. Once you invest that lump sum, every dividend, interest payment, and capital gain faces normal taxation.

Means-tested government benefits disappear when you suddenly have $300,000 in your checking account. Supplemental Security Income cuts off at $2,000 in countable assets for individuals. Medicaid has similar limits varying by state. Special needs trusts solve this problem, but you must establish them before receiving the money—not after.

Annuity and Installment Options

Instead of one payment, convert the death benefit into monthly income stretching across years or decades.

Fixed-period installments divide the money across a timeline you choose—usually 5, 10, 15, or 20 years. Select 10 years on a $300,000 benefit, and you'll receive roughly $2,800 monthly ($336,000 total when you include interest at current 4% rates). The insurer guarantees these payments regardless of market performance.

Life annuities convert the death benefit into income lasting your entire life, however long that is. A 55-year-old woman might receive $1,400 monthly from a $300,000 benefit. Live to 95? You'll collect $672,000 total—more than double the original death benefit. Die at 60? The insurance company keeps the remaining balance unless you selected a period-certain or refund option.

Fixed-amount installments let you specify the monthly payment. Request $3,500 monthly from a $400,000 benefit, and payments continue for approximately 10 years depending on interest rates. When the money runs out, payments stop.

These structured approaches force financial discipline. You can't blow $200,000 on a boat if you're only receiving $2,000 monthly. They also protect against predatory relatives, bad investments, and your own impulses. The insurance company credits interest on the unpaid balance—currently 3-5% annually, comparable to money market rates.

The downside? Reduced control and potentially lower returns. If stocks return 10% annually over the next decade but your annuity pays 4%, you've sacrificed significant growth. Emergency access becomes complicated. Need $50,000 for unexpected medical bills? Too bad—you're locked into your monthly payment schedule. Some insurers allow structure changes, but many don't.

Interest-Bearing Accounts (Retained Asset Accounts)

Picture a checking account holding your death benefit. You get a checkbook or debit card. Write checks whenever you want. The balance earns interest while you decide what to do long-term.

Author: Olivia Ramsey;

Source: everymuslim.net

Retained asset accounts (RAAs) give you breathing room. Instead of having $400,000 deposited into your regular checking account on Tuesday, the insurer holds it in an FDIC-insured account while you meet with financial advisors, research investment options, and make thoughtful decisions. You're not paralyzed by the money sitting there, because you can access it anytime with a check.

The controversy? Some insurers made RAAs the default option without clearly explaining that beneficiaries could simply request a direct deposit instead. Consumer advocates discovered that insurers were earning a spread—paying beneficiaries 1.5% interest on RAAs while investing that money at 4-5% themselves. The insurers kept the difference.

Check the interest rate before accepting an RAA. Is it competitive with high-yield savings accounts currently paying 4-5%? If they're offering 1.5%, decline it and request direct deposit to your own bank where you'll earn more.

Taking 60-90 days before making major financial decisions with inherited money typically leads to better outcomes than acting within the first two weeks. Grief impairs judgment. The exhaustion of settling an estate clouds thinking. A retained asset account can provide helpful space between receiving the money and deploying it—but only if the interest rate isn't penalizing you for that patience. Compare what they're offering to what you'd earn in a money market fund. Don't give the insurance company free use of your money.

— Jennifer Fong, CFP®, Fidelity Financial Planning

Comparison of Life Insurance Payout Methods

| Payment Method | How It Works | Tax Treatment | Best For |

| Lump Sum | Full death benefit deposited via direct transfer or mailed check | Death benefit: no tax; interest from death date to payout date: taxable | People facing immediate large expenses, those with strong financial discipline, beneficiaries wanting control over investments |

| Fixed-Period Annuity | Predetermined equal monthly payments across chosen timeframe (typically 5-20 years) | Death benefit portion: no tax; interest earned on each payment: ordinary income tax | Recipients wanting automatic spending discipline and predictable income for specific years |

| Life Annuity | Monthly payments continuing until beneficiary's death, regardless of longevity | Initially tax-free based on exclusion ratio; later payments become partially or fully taxable | Older beneficiaries (60+) worried about depleting resources during long retirement |

| Interest-Only | Principal stays with insurer; beneficiary receives only interest payments | Interest received: fully taxable as ordinary income | Temporary option for beneficiaries needing time to finalize decisions while preserving principal |

| Retained Asset Account | Death benefit deposited in interest-earning account with check-writing access | Death benefit deposit: no tax; interest accumulation: taxable income | Those wanting flexibility and transition time before committing to long-term strategy |

Life Insurance Claim Settlement Timeline: What to Expect

Three weeks? Three months? Six months? The timeline depends on factors you control and factors you don't.

Average Processing Times by Claim Type

Straightforward claims—policies older than two years, clear cause of death, complete documentation—settle in 30-45 days from when the insurer receives everything. Some companies process simple claims in 10-14 days when documents arrive electronically through their portal. MetLife and Prudential have accelerated their fastest claims to under two weeks.

But that clock starts when they receive complete documentation. Mail them the claim form on Monday but forget to include your W-9? The clock doesn't start until the W-9 arrives the following week. Submit a death certificate with a clerk's signature instead of the required raised seal? Clock resets when you mail the correct version.

Claims during the contestability period (first 24 months after policy issue) automatically take 60-90 days minimum. The insurer investigates whether the application contained material misrepresentations. They'll order medical records from every doctor listed. They'll check the Medical Information Bureau database. They'll compare prescription histories against what was disclosed. This isn't suspicion directed at you personally—it's standard practice on every recent policy regardless of circumstances.

Accidental death claims require investigation confirming the death meets the policy's definition of "accident." Was it truly accidental, or did reckless behavior contribute? Drug overdoses sit in a gray area. Motorcycle deaths require determining whether speed or safety equipment played a role. Budget 60-120 days for accidental death claims even when everything appears straightforward.

Deaths under investigation by law enforcement can take six months or longer. Homicides require waiting for police conclusions. Suspicious circumstances need resolution before insurers will pay. If a beneficiary is suspected of involvement in causing the death, expect the insurer to delay indefinitely until legal proceedings conclude.

What Delays Your Payout

Missing documents cause 60% of claim delays according to LIMRA research. The death certificate has the middle name wrong. The claim form is missing your signature on page three. You uploaded photos of documents instead of PDFs. The death certificate is a photocopy instead of a certified original.

Check every field twice before submitting. Read the document checklist three times. Confirm signatures appear everywhere they're required.

Outdated beneficiary designations create nightmares. The designated beneficiary is your ex-wife from 15 years ago because you never filed a change form after the divorce. The named beneficiary died three years before the policyholder. The beneficiary is now incapacitated and can't legally receive payment. Each scenario adds weeks while the insurer determines the proper recipient under policy language and state law.

Disputes among beneficiaries halt everything. When multiple people claim entitlement—ex-spouse versus current spouse, children from first marriage versus children from second marriage—insurers typically file an interpleader action. They deposit the death benefit with the court and withdraw from the dispute, letting a judge decide distribution. This process commonly takes 12-18 months.

Policy lapse questions require investigation. The deceased thought the policy was active, but premium payments stopped eight months ago. Was the grace period still active at death? Had the policy converted to reduced paid-up insurance? Did automatic premium loan provisions keep it in force? The insurer must reconstruct the payment history and apply policy provisions chronologically.

International deaths require additional documentation. A death in Mexico needs a translated death certificate authenticated by the Mexican government and the U.S. consulate. A death in Thailand might need an apostille. Each country has different procedures. Factor in 30-60 extra days for foreign deaths.

Typical Life Insurance Claim Timeline

| Stage | Timeframe | What Happens |

| Claim Filing | Day 1 | Beneficiary reaches out to insurance company and receives claim forms; gathers death certificate and required documents |

| Initial Review | Days 2-7 | Assigned examiner confirms policy active status, validates beneficiary designation, checks documentation completeness |

| Investigation (if any) | Days 8-60 | Contestable policies: examiner orders medical records, reviews application accuracy, sometimes conducts beneficiary interviews; accidental death: investigates circumstances and cause determination |

| Approval | Days 30-45 (straightforward) or 60-90+ (complicated) | Examiner validates all policy conditions satisfied and calculates final payout after any adjustments |

| Payment Processing | Days 31-50 | Beneficiary chooses payout structure; company processes via selected method (direct deposit, physical check, or retained asset account) |

Author: Olivia Ramsey;

Source: everymuslim.net

Common Mistakes That Delay or Reduce Your Payout

Beneficiaries accidentally sabotage their own claims more often than you'd think. These errors cost time and money.

Life changes happen, but beneficiary forms stay the same unless you actively update them. Divorce doesn't automatically remove an ex-spouse as beneficiary. Remarriage doesn't add your new spouse. Having children doesn't include them. That form you signed when you bought the policy 15 years ago still controls who gets paid, regardless of what your will says or what your family assumes you intended.

Your will can't override a beneficiary designation. Life insurance passes by contract, not by will. Even if your will explicitly states "I leave all my assets including life insurance to my current wife Sarah," the insurance company pays whoever is named on their beneficiary form. If that's your ex-wife Jennifer, Jennifer gets the money and Sarah gets nothing from the life insurance.

Naming minor children directly as beneficiaries guarantees delays. Insurers won't hand $200,000 to a 12-year-old. State law requires appointing a guardian or conservator through court proceedings to manage those funds until the child reaches legal age. This process adds 3-6 months and costs $3,000-8,000 in legal fees. Better alternatives: name a trust established for the child's benefit, or designate a custodian under the Uniform Transfers to Minors Act (UTMA).

Invisible policies cause money to sit unclaimed forever. Your father bought a $100,000 policy in 1995. He filed the policy document somewhere and forgot about it. He dies in 2024. You don't know the policy exists, so you never file a claim. The National Association of Insurance Commissioners estimates $1 billion in life insurance benefits goes unclaimed annually because beneficiaries don't know policies exist.

Tell your beneficiaries where you keep policy documents. Give them the insurer's name and policy number. Store this information with your will and power of attorney. Update them when you buy new coverage. The NAIC runs a Life Insurance Policy Locator Service searching participating insurers' databases, but it only covers companies that opted into the system.

Filing years after death complicates matters. Most states don't impose strict deadlines for death claims, but long delays require explaining why you waited. More problematically, unclaimed policies eventually escheat to state unclaimed property divisions after periods ranging from 3-7 years depending on state law. Once escheated, you must claim funds from the state comptroller's office instead of the insurer—a more bureaucratic process.

Beneficiaries often assume death benefits count toward the deceased's taxable estate for federal estate tax purposes. They don't—if properly structured. Life insurance paid to named beneficiaries bypasses probate entirely and escapes estate taxation unless the deceased maintained "incidents of ownership" over the policy. Policies owned by irrevocable life insurance trusts avoid estate taxation completely, but this arrangement must be established at least three years before death.

The death benefit itself isn't income tax, but surrounding elements are taxable. Interest earned between death date and payout date is ordinary income. Interest from installment or annuity payment options is ordinary income. Growth in the policy's cash value gets taxed upon distribution in certain situations. Beneficiaries choosing structured payouts receive Form 1099-INT annually reporting the taxable interest portion.

Forgetting about supplemental coverage leaves money on the table. Your employer provided $50,000 group life insurance automatically. You also bought a $25,000 accidental death policy through your credit union. Your mortgage included credit life insurance. Your auto policy had $10,000 accidental death coverage. File claims on everything, even small policies. That extra $85,000 shouldn't go unclaimed because you focused only on the main policy.

How Multiple Beneficiaries Split a Life Insurance Payout

Naming three children as equal beneficiaries sounds straightforward until one of them dies before you do. Now what?

Most policies state percentage allocations explicitly: "50% to Jane Doe, 25% to John Doe, 25% to Jim Doe." The math is simple. A $600,000 death benefit pays Jane $300,000, John $150,000, and Jim $150,000.

But what if Jane died two years before you did? If you never updated the beneficiary designation and didn't name a contingent beneficiary for Jane's share, policy language determines what happens next. Some policies redistribute proportionally among survivors—John and Jim would each receive $300,000 (50% each of the $600,000). Other policies pay Jane's share to her estate, where it flows through probate to whoever inherits under her will.

Per stirpes designation (Latin for "by branch" or "by representation") means if a beneficiary predeceases you, that beneficiary's share passes to their descendants. You name your three children equally per stirpes on a $600,000 policy. Your daughter Jane dies before you do, leaving behind two children (your grandchildren). At your death, John receives $200,000, Jim receives $200,000, and Jane's two children split her $200,000 share, receiving $100,000 each.

Per capita designation (Latin for "by head") divides the death benefit equally among all living named beneficiaries at the time of your death. Using the same example, if Jane has died, John and Jim each receive $300,000 (50% each). Jane's children receive nothing. The money stays within the generation named, not passing down to the next generation.

The distinction matters enormously in blended families. Second marriages with children from previous marriages create scenarios where per stirpes versus per capita designations produce wildly different outcomes. A $500,000 policy naming "all my children" per capita pays only living children equally. The same policy with per stirpes designation includes grandchildren representing deceased children.

Contingent (secondary) beneficiaries receive payment only if all primary beneficiaries died before the insured. This safety net prevents the death benefit from passing to your estate and through probate. Always name contingent beneficiaries, even if it seems unlikely your primary beneficiaries will predecease you. Car accidents, unexpected illnesses, and other tragedies happen.

Disputes occasionally erupt, especially in blended families or when designations are decades old. The policy names your first wife, but you've been married to your second wife for 20 years and simply forgot to update the form. Your second wife believes she's entitled to the money. Your first wife is legally entitled according to the beneficiary form. If disagreement arises and multiple parties make competing claims, insurers file interpleader actions—depositing the death benefit with the court and withdrawing from the dispute.

Wills don't override beneficiary designations. This bears repeating because families frequently misunderstand it. Your will might state "I leave all assets to my son Michael," but if your life insurance policy names your daughter Jennifer as beneficiary, Jennifer receives the life insurance proceeds regardless of what the will says.

Class designations like "my children" or "my descendants" create interpretation questions. Does "my children" include adopted children? Stepchildren? Children born after the policy issue date? Children from your first marriage but not your second? State law and specific policy language determine the answer. Avoid ambiguity by naming beneficiaries individually with full legal names and relationships: "Jane Marie Smith, daughter; John Robert Smith, son; Jennifer Lynn Smith, daughter."

Frequently Asked Questions About Life Insurance Payouts

Making the Payout Process Work for You

A $300,000 death benefit represents serious money requiring serious decisions. The structure you choose reverberates for years.

Before selecting how you'll receive payment, honestly assess your financial literacy, self-discipline, immediate cash requirements, and long-term income needs. Uncertain? Request a retained asset account or interest-only arrangement preserving your options while you consult a fee-only financial advisor. Most insurers allow changing your election within 30-60 days of the initial decision.

Submit complete, accurate documentation immediately after obtaining the death certificate. Request six certified copies from the funeral home. Fill out every field on the claim form. Include all required supporting documents. Follow up with the assigned claims examiner if you haven't received an update within 15 days.

Review your own life insurance beneficiary designations right now—not next month. Update them after marriages, divorces, births, deaths, and significant changes in relationships or financial circumstances. Verify designations match your current intentions and that beneficiary contact information is accurate.

The claims process, though sometimes bureaucratic, protects both insurance companies and legitimate beneficiaries from fraud. Understanding the mechanics removes uncertainty and positions you to receive your full benefit as quickly as possible. The death benefit represents the insured's final financial gift to you. Claim it properly. Deploy it wisely.