What Is a Suicide Clause in Life Insurance and How Does It Affect Your Coverage?

What Is a Suicide Clause in Life Insurance?

Content

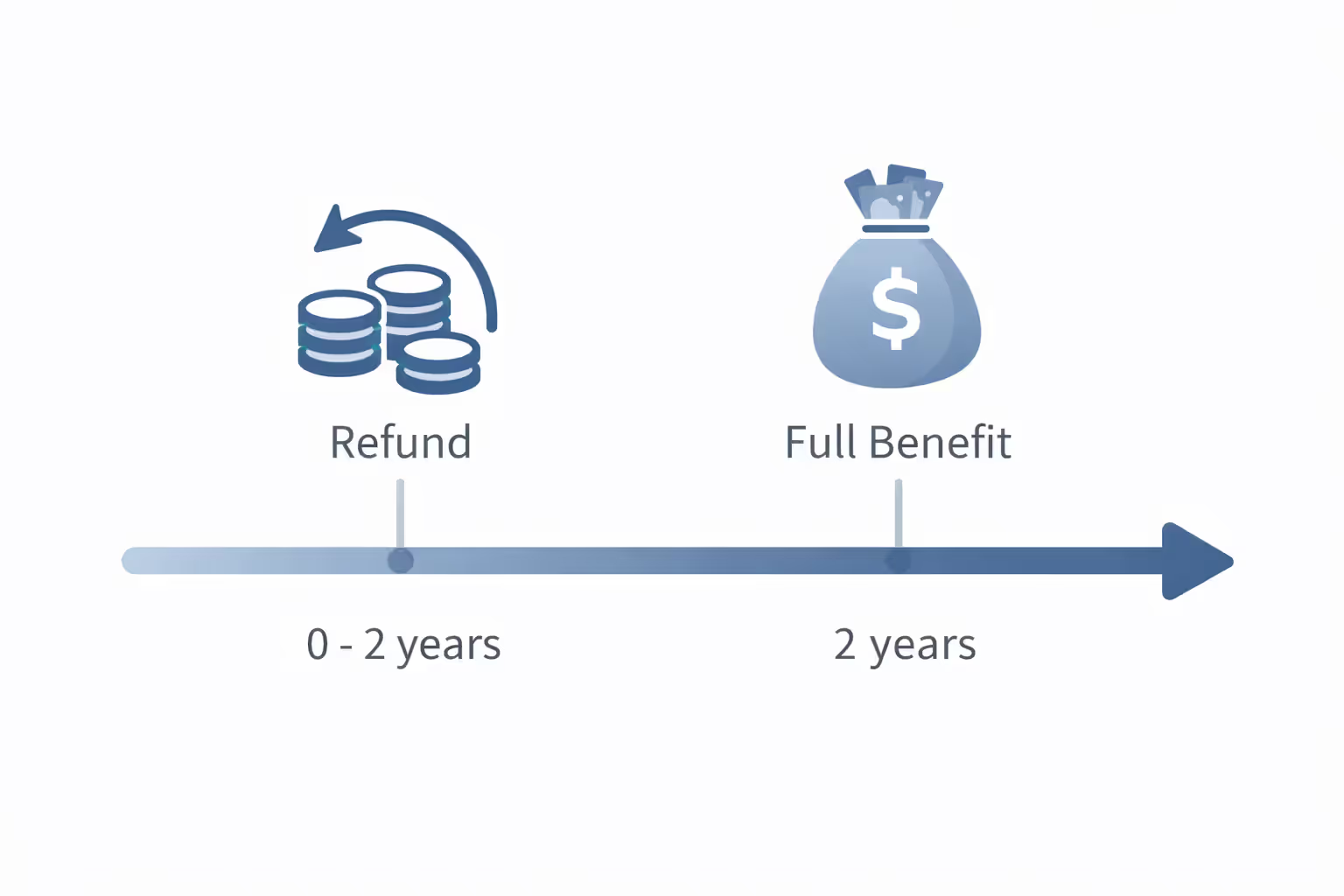

Nearly every life insurance policy sold in America contains a suicide clause—a provision that temporarily restricts when your beneficiaries can collect the full death benefit if you die by suicide. Think of it as a waiting period, usually one or two years, during which the insurance company won't pay out the complete benefit for this specific cause of death.

Here's what actually happens: If you buy a $500,000 policy and die by suicide seven months later, your family won't receive that half-million dollars. Instead, they'll get back the premiums you paid—maybe $2,500 or $3,000. But if you maintain that same policy for 25 months and then die by suicide, your beneficiaries receive the full $500,000, exactly like they would for any other covered death.

This provision sits at a complicated crossroads. Insurance companies need protection against people buying policies while actively planning self-harm. Families need real financial security. State regulators try balancing both interests. The result? A time-limited restriction that affects relatively few claims but carries enormous weight when it does apply.

Most people never think about this clause until they're comparing policies or, tragically, dealing with a claim. Understanding how it works—and more importantly, when it stops applying—matters whether you're shopping for new coverage or evaluating a policy you've held for years.

How the Suicide Clause Works in Life Insurance Policies

The mechanics are simpler than the emotions surrounding them. Your policy's suicide clause insurance provision creates a blackout window. During this period—typically 12 or 24 months from your policy's start date—the insurer can deny the full death benefit if you die by suicide.

Author: Danielle Harper;

Source: everymuslim.net

Let's walk through a real example. Sarah buys a $750,000 term life policy on March 15, 2024, in a state with a two-year exclusion. She pays $85 monthly. If Sarah dies by suicide on January 10, 2026, her beneficiaries receive only the premiums she paid (roughly $1,615 total). But if she dies by suicide on March 16, 2026—just two months later—her family gets the full $750,000 benefit. That's how sharply the exclusion period cuts off.

The clock starts ticking from your policy's effective date, not from when you applied or got approved. Your effective date usually matches either when you paid your first premium or when the company formally approved your application. Check your policy declarations page—that's where you'll find this critical date.

Premium refunds work differently depending on what type of coverage you own. Term policies simply return the premiums you've paid. Permanent insurance policies (whole life, universal life, variable universal) return either your premiums or your policy's cash value, whichever is higher. This distinction matters more as time passes. A permanent policy held for 23 months might have accumulated $4,500 in cash value even if you only paid $3,200 in premiums. Your beneficiaries would get the $4,500.

After the exclusion window closes, suicide becomes just another covered cause of death. The policy doesn't care whether you die from cancer, a car accident, or suicide—your beneficiaries get the full benefit, period. The clause doesn't reduce your benefit or add conditions. It simply stops existing once you've held the policy past the exclusion deadline.

Author: Danielle Harper;

Source: everymuslim.net

One detail trips people up constantly: some policies state the exclusion in months (24 months) while others use years (2 years). A two-year clause might mean your second policy anniversary, which could be 730 or 731 days depending on leap years. Read your specific contract language carefully, or better yet, call your insurer and ask them to confirm the exact date when your suicide coverage begins. Get that confirmation in writing.

Why Insurance Companies Include Suicide Exclusion Periods

Insurance companies face a genuine financial risk without these clauses. Someone experiencing a suicidal crisis could theoretically buy a massive policy, wait the required few weeks for coverage to begin, and then create an immediate claim. This isn't speculation—it's happened enough historically that every major insurer now includes protection against it.

The industry term for this problem is "adverse selection." It means people with higher risks buy more insurance than people with lower risks. Imagine if life insurance paid out immediately for suicide with no waiting period. Anyone planning self-harm could purchase multiple million-dollar policies across different companies. Insurance only works when the risk pool contains mostly healthy people subsidizing claims from the few who die unexpectedly. Immediate suicide coverage would flip that model upside down.

But there's a timing element that makes the one-to-two-year window work. Research shows that acute suicidal crises typically don't extend beyond several months. Someone experiencing a crisis in March usually isn't still executing the same plan 18 months later. Either the crisis resolves, they receive treatment, or tragically, they act during the acute phase. The exclusion period extends beyond typical crisis durations while remaining short enough that most policyholders reach full coverage relatively quickly.

State insurance departments set the maximum exclusion length—usually two years. Insurers can choose shorter periods (and some do), but they can't go longer. This regulatory ceiling attempts balancing insurer protection with consumer rights. After all, someone who pays premiums for 25 months has demonstrated they're a standard risk, not someone who bought coverage for nefarious reasons.

Here's where it gets interesting: insurers don't actually want to deny claims. Every denied claim costs them money in investigations, administrative work, and potential litigation. They'd much prefer collecting premiums for 30 years and paying death benefits for natural causes. The suicide clause exists to prevent a specific exploitation scenario, not to avoid paying legitimate claims.

Premium pricing reflects this protection. Without suicide clauses, insurers would need to increase everyone's rates to cover the additional risk. The clause lets them offer lower premiums by eliminating one specific unpredictable risk during the first year or two. You're essentially getting a price discount in exchange for accepting the temporary limitation.

Three states—Colorado, Missouri, and North Dakota—decided two years was too long and capped exclusions at one year maximum. Their insurance departments concluded that 12 months provided sufficient protection against adverse selection while giving consumers faster access to complete coverage. Other states considered similar rules but ultimately stayed with two-year maximums. This state-by-state variation creates real differences in how quickly your coverage matures.

When Does Your Life Insurance Coverage Actually Start for Suicide?

You've got two different start dates to track. Your general coverage begins immediately (or after a short waiting period). But suicide-specific coverage doesn't kick in until the exclusion period runs out. This creates a split-level protection system that confuses many policyholders.

Here's a concrete example: Mark buys a policy with an effective date of June 1, 2024, in Texas (a two-year state). Starting June 1, 2024, he's covered for heart disease, cancer, accidents, and virtually every other cause of death. But suicide coverage doesn't begin until June 1, 2026. His policy simultaneously provides full coverage for 99% of death causes while excluding one specific cause for the first two years.

The contestability period adds another wrinkle. During the first two years (in most states), your insurance company can investigate your application and potentially cancel your entire policy if they discover you lied about something important. Someone who claimed they never smoked but actually has a pack-a-day habit could lose their coverage entirely if they die within two years and the insurer investigates.

Notice how these periods usually overlap? Both the suicide clause and contestability period typically run for two years from your effective date. They expire simultaneously, which means after 24 months, your insurer can't deny claims based on suicide AND can't investigate your application for misrepresentations. You've reached full, uncontestable coverage.

Policy reinstatements reset everything, and this catches people off guard constantly. Let's say you bought coverage in 2020 but stopped paying premiums in 2023. The policy lapses. Then in 2024, you reinstate it by paying the back premiums and passing any required health questions. Your new exclusion period starts from the 2024 reinstatement date, not your original 2020 purchase. You're basically starting over as if you'd just bought the policy yesterday.

Why would insurers restart the clock? Because your lapse might indicate changed circumstances. Maybe you stopped paying because you're facing a crisis. Maybe your health deteriorated. The reinstatement essentially represents a new underwriting decision, and the insurer wants the same protection they'd get with any new policy.

Group-to-individual conversions get messy. Your employer probably offers life insurance—maybe one or two times your salary. That group policy has its own suicide clause that started when you enrolled. If you leave that job, you can usually convert your group coverage to an individual policy without a medical exam. But does your time under the group plan count toward the new individual policy's exclusion period?

Sometimes yes, sometimes no. It depends on your state's laws and the specific insurance carrier's rules. Some states require insurers to credit your group coverage time toward the individual policy's exclusion. Others don't. Some insurers voluntarily credit that time as a competitive advantage. You absolutely need written confirmation about this before converting. Don't assume. A benefits administrator at your old job might say "your coverage continues," but that doesn't tell you whether you're starting a fresh suicide exclusion period.

I've seen people maintain employer coverage for 18 months, convert to individual policies, then assume they only have six months left on their suicide exclusion. Turned out the conversion started a completely new two-year clock. Their beneficiaries discovered this the hard way. Get it in writing, specifically addressing whether your prior group coverage time counts toward the exclusion period.

State-Specific Rules and Exceptions to Standard Suicide Clauses

Three states buck the national two-year standard. If you live in Colorado, Missouri, or North Dakota, your maximum suicide exclusion period is one year, regardless of what the insurance company might prefer. An insurer can't enforce a 24-month exclusion in these states even if that's their standard policy language everywhere else. State law overrides the contract.

Why did these three states choose 12 months? Each had slightly different reasoning, but the core logic was similar: 12 months provides adequate protection against adverse selection without unnecessarily extending the restriction. Their insurance departments concluded the second year of exclusion didn't add much protection but delayed meaningful coverage for residents.

Forty-seven other states allow the full two-year exclusion. Some states considered shortening the period but decided against it after insurance industry lobbying. The two-year standard has existed for decades, and most state insurance codes explicitly permit it.

Military service members sometimes get additional protections, though these vary wildly by state. Federal law (the Servicemembers' Civil Relief Act, or SCRA) provides various financial protections for active-duty personnel, but it doesn't specifically address suicide clauses. Some states created their own protections, like prohibiting suicide clause enforcement for deaths occurring during active deployment. Other states offer no special treatment beyond general consumer protections.

Group coverage through employers operates under its own logic. Your company's group policy typically includes a suicide clause, but it often works differently than individual coverage. Many group plans provide immediate coverage (no suicide exclusion) if you enroll during your initial eligibility window—usually your first 31 days of employment. Add coverage later or increase your coverage amount outside that window? You might face a new exclusion period for the additional coverage amount.

Here's how this plays out: Jennifer starts a new job and enrolls in the group life insurance during her first month, electing $200,000 of coverage. No suicide exclusion applies to that $200,000 because she enrolled during the initial eligibility period. Three years later, she gets promoted and wants to increase her coverage to $400,000. The additional $200,000 might be subject to a new suicide exclusion period starting from when she adds it. Her original $200,000 remains fully covered, but the new increment operates under fresh restrictions.

| Your State | Maximum Exclusion (Individual) | Typical Group Policy Terms | What Makes It Different |

| Colorado | 12 months (state maximum) | 12 months maximum | State law prevents longer exclusions |

| Missouri | 12 months (state maximum) | 12 months maximum | Among nation's shortest restrictions |

| North Dakota | 12 months (state maximum) | 12 months maximum | Consumer protection regulations |

| California | 24 months (standard) | Often waived at initial enrollment | No state restrictions on length |

| Texas | 24 months (standard) | 24 months typical | Follows national norms |

| New York | 24 months (standard) | 24 months typical | Requires clear disclosure in policy |

| Florida | 24 months (standard) | 24 months typical | Standard provisions apply |

| Active Military | State-dependent | State-dependent | Some states ban enforcement during deployment |

Your location at the time you apply determines which rules apply. Someone living in Missouri who moves to Texas after buying their policy still operates under Missouri's one-year maximum for that specific policy. But if they buy a new policy after moving to Texas, that new policy can have a two-year exclusion.

Author: Danielle Harper;

Source: everymuslim.net

What Happens When a Claim Is Filed During the Exclusion Period

Death claims trigger investigations regardless of the cause, but suspected suicides during the exclusion period get intense scrutiny. The insurance company's claims department will request the death certificate (obviously), but they'll also pull medical records, police reports, autopsy results, toxicology screens, and witness statements. They might interview family members, review the deceased's medical history going back years, and examine the circumstances surrounding the death.

This investigation isn't malicious—it's necessary. The company needs to determine whether the suicide clause applies, and they need evidence to support whatever decision they make. Families find this process intrusive during an already horrific time, but insurers face liability if they pay claims that shouldn't be paid or deny claims that should be paid.

Author: Danielle Harper;

Source: everymuslim.net

Documentation requirements exceed typical claims by a significant margin. For a heart attack death, the insurer usually needs just a death certificate and maybe the attending physician's statement. For a potential suicide during the exclusion period, expect requests for:

- Death certificate (certified copy)

- Autopsy report including toxicology

- Police investigation reports and incident reports

- Medical records from the past 2-5 years

- Mental health treatment records

- Prescription history

- Witness statements

- Coroner's determination documents

Gathering these documents takes time, especially medical records which can require weeks to obtain. The claims process that normally takes 30-45 days can stretch to four or five months when suicide clause questions arise.

If the insurer determines the clause applies, they'll issue a check for premiums paid (or cash value for permanent policies). This usually comes with a letter explaining the determination and your appeal rights. The premium refund includes interest in some states but not others—another variable in an already complicated situation.

Beneficiaries can challenge the determination, and many do successfully. The burden of proof sits with the insurance company. They must demonstrate by "preponderance of evidence" (more likely than not) that death resulted from intentional self-harm. When circumstances look ambiguous, that's a tough standard to meet.

Consider a single-vehicle accident where someone drove off the road into a tree. Suicide? Maybe. But also maybe they had a medical emergency, got distracted by their phone, swerved to avoid an animal, or fell asleep at the wheel. Without a suicide note or clear evidence of intent, the insurer struggles to prove suicide more likely than these alternatives.

Sarah Martinez, who's represented beneficiaries in contested life insurance claims for 18 years, put it this way:

Insurance companies sometimes see suicide when they should see ambiguity. I've handled cases where someone died from a drug overdose and the insurer immediately classified it as suicide because the deceased had a history of depression. But having depression doesn't make every overdose intentional. Many were clearly accidental—mixing medications, not understanding dosing, or taking drugs without knowing their potency. When we pushed back with evidence showing these were accidents, we recovered full benefits in about 60% of these cases.

— Sarah Martinez

Appeals start internally with the insurance company's reconsideration process. You submit additional evidence or arguments explaining why the determination was wrong. If internal appeals fail, you can file complaints with your state insurance department. Most states have consumer assistance divisions that will investigate and sometimes pressure insurers to reconsider. Final option: litigation, which makes sense for larger policies where legal fees won't consume the potential recovery.

The timeline for disputed claims can extend six months to over a year. Families facing this situation often need legal help, particularly if the policy amount justifies the attorney fees. Some insurance lawyers work on contingency (taking a percentage of recovery rather than hourly fees), making representation accessible even without upfront money.

Common Mistakes Policyholders Make About Suicide Clauses

Assuming your policy matches the general rules ranks as the most common error. You might read that "most policies have two-year suicide clauses" and assume yours does too. But your specific policy might have a one-year clause, or different reinstatement rules, or unique state-specific provisions. Read your actual contract—specifically the "exclusions" or "limitations" section. If the language confuses you (it probably will), call the insurer and ask them to explain your specific terms.

Hiding mental health history creates problems that go beyond suicide clauses. During the contestability period, insurers can rescind your entire policy if they discover material misrepresentations. "Material" means something that would have affected their underwriting decision or pricing. Undisclosed depression, anxiety medications, psychiatric hospitalizations, or previous suicide attempts definitely qualify as material.

People hide this information thinking it'll help them get coverage or avoid higher premiums. Short-term, maybe it does. But if you die within two years for any reason, the insurer will investigate your application. They'll request medical records going back 5-10 years. They'll discover the undisclosed history. And they might rescind the policy entirely, leaving your beneficiaries with nothing—not even the premium refund they'd get under a suicide clause denial.

Here's a better approach: disclose everything accurately. Yes, mental health history might increase your premiums slightly or result in some insurers declining coverage. But many companies will still issue policies, and once you get past the contestability period, your coverage becomes rock-solid. A slightly higher premium beats a worthless policy.

Confusion about policy anniversary dates versus calendar calculations causes timing errors. Your policy effective date is December 12, 2023. You're in a two-year exclusion state. When does your suicide coverage begin? December 12, 2025—exactly two years from the effective date. Not December 1, 2025. Not December 31, 2025. Not January 1, 2026. The specific date matters if death occurs near the end of the exclusion period.

Some people track this by policy anniversaries: "My second policy anniversary is when coverage starts." That works fine if you understand a policy anniversary means the exact day, not just the month or year. Your second anniversary is December 12, 2025, not "sometime in December 2025."

Letting coverage lapse and restarting the exclusion clock is probably the costliest mistake on this list. Life gets complicated. You change jobs, face financial pressure, lose track of bills, or assume employer coverage is sufficient. You stop paying premiums. The policy lapses after a grace period (usually 30-31 days).

Six months later, you realize you need that coverage. You contact the insurer about reinstating the policy. They might allow it, but you'll typically need to pay back premiums, possibly answer new health questions, and—here's the kicker—you start a brand new suicide exclusion period from the reinstatement date.

That policy you originally bought three years ago? You just reset its suicide clause to day one. If you had eight months left on your original exclusion, you've now got 24 more months. This stuns people who didn't read the fine print on reinstatement applications.

The smarter move: if you're facing financial difficulties, contact your insurer before the policy lapses. Many companies offer options like grace extensions, reduced face amounts (lower death benefit with lower premiums), or conversion to paid-up insurance that requires no future premiums. Any of these options preserves your original effective date and doesn't restart your suicide clause.

Replacing policies without considering the implications trips up people constantly. You've held a policy for 18 months. An agent approaches you with a "better deal"—lower premiums, more coverage, better terms. Sounds great, right?

But if you cancel your existing policy and buy the new one, you start a fresh suicide exclusion period. Those 18 months you already served? Gone. You're back to month zero on the new policy's clock. Unless the new policy offers dramatically better value, you're usually better off keeping existing coverage until the exclusion period expires, then shopping for replacements if you still want to.

Some agents know this and disclose it. Others focus on the sale and gloss over the suicide clause reset. Always ask explicitly: "If I switch to this new policy, will I face a new suicide exclusion period?" Get the answer in writing.

Frequently Asked Questions About Suicide Clauses in Life Insurance

Making Sure Your Family Gets the Protection You're Paying For

The suicide clause creates a temporary gap in coverage that closes relatively quickly for most people. Those first 12 or 24 months pass faster than you'd expect, and then you've got complete protection regardless of what happens.

Maintaining continuous coverage without letting policies lapse protects your timeline. That's the single most important action you can take. Set up automatic premium payments if your insurer offers them. Create calendar reminders for payment due dates. Treat your life insurance premium like your mortgage or rent—it gets paid first, not with whatever's left over.

When you're shopping for new coverage or evaluating existing policies, ask specific questions about your suicide clause. What's the exact exclusion period in your state? On what date does suicide coverage begin for your specific policy? What happens if you reinstate after a lapse? What if you convert from group coverage—does that time count? Get answers in writing through email or formal policy documents. Verbal assurances from agents don't help when claims get denied.

For anyone dealing with a claim during the exclusion period, remember the insurance company must prove its determination. You've got rights to appeal, contest findings, and demand proper investigation. Premium refunds provide some financial benefit even when the full death benefit doesn't apply. Don't accept initial denials without questioning whether the insurer truly met its burden of proof. State insurance departments provide free assistance, and attorneys handle many of these cases on contingency if the policy amount justifies it.

Life insurance accomplishes one fundamental goal: protecting the people who depend on you financially. The suicide clause represents a brief limitation on that protection, but the limitation expires. Understanding exactly when it expires for your specific situation, protecting that timeline by avoiding lapses, and reading your actual policy terms ensures your family receives what you intended to provide.