Compare your cash-access options before you decide.

Accelerated Death Benefit Rider Guide

Content

An accelerated death benefit rider allows life insurance policyholders to access a portion of their death benefit while still alive when diagnosed with a qualifying serious illness. Instead of waiting until death for beneficiaries to receive the payout, this rider provides funds during a medical crisis—often when financial resources are most desperately needed.

Most major insurers now include this rider at no additional charge on term and permanent life insurance policies. The rider essentially advances money that would otherwise go to beneficiaries after death, reducing the final death benefit by the amount withdrawn plus any applicable fees or interest.

Understanding how this rider functions, what qualifies you for access, and how it compares to other funding options can help you make informed decisions during one of life's most challenging periods.

When You Can Access Your Life Insurance Early

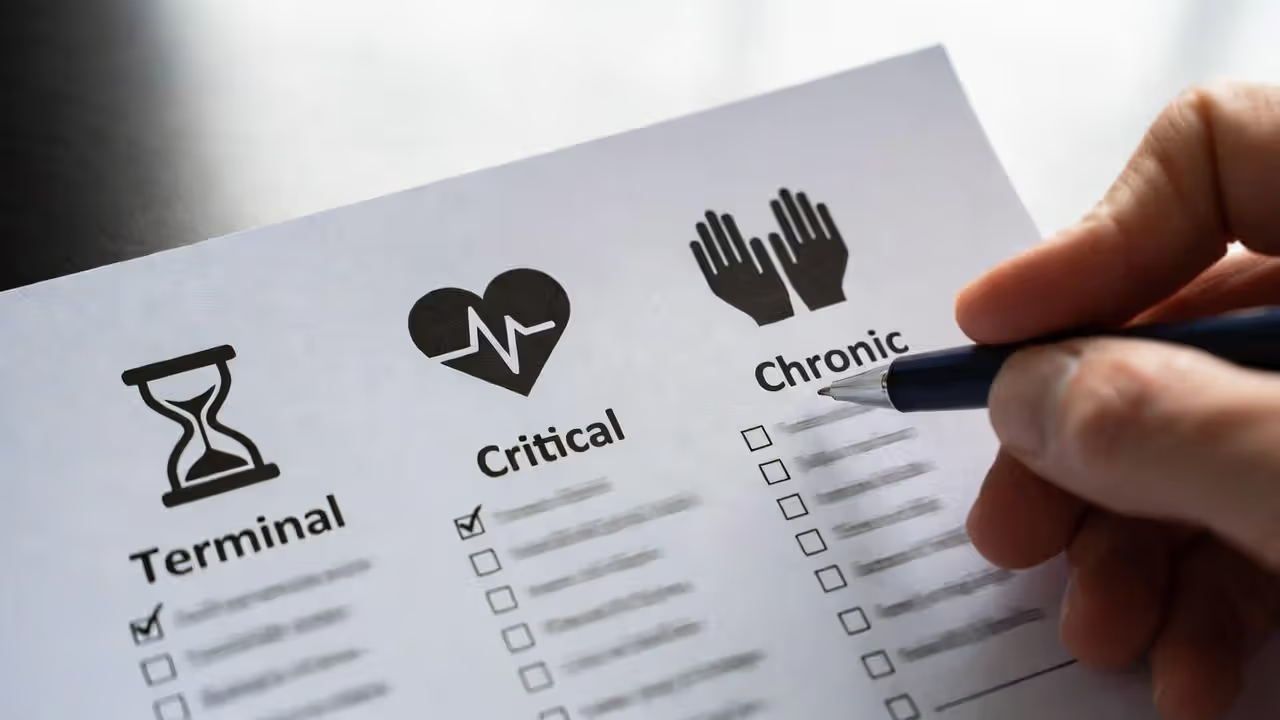

Accelerated death benefit riders typically activate under three main medical scenarios: terminal illness, chronic illness, and critical illness. Each category has distinct qualification requirements that vary by insurer and state regulation.

Terminal illness qualifications

Terminal illness provisions form the most common trigger for accelerated death benefits. Most policies define terminal illness as a condition certified by a physician that will likely result in death within 12 to 24 months. Some insurers use a 12-month threshold, while others extend to 24 months.

To qualify, you'll need written certification from your attending physician, often supported by medical records, test results, and sometimes a second medical opinion. The physician must document the diagnosis, prognosis, and expected life expectancy. Conditions that commonly qualify include advanced-stage cancers, end-stage organ failure, progressive neurological diseases like ALS, and advanced AIDS.

The certification requirement protects insurers from premature claims while ensuring legitimate cases receive prompt attention. Most carriers process terminal illness claims faster than other categories because the prognosis is more definitive.

Author: Michael Stanton;

Source: everymuslim.net

Chronic and critical illness triggers

Chronic illness qualifications focus on functional impairment rather than life expectancy. You typically qualify when unable to perform at least two activities of daily living (ADLs) for a minimum of 90 consecutive days. ADLs include bathing, dressing, eating, toileting, transferring (moving from bed to chair), and continence.

Alternatively, severe cognitive impairment requiring substantial supervision—such as advanced Alzheimer's or dementia—can trigger chronic illness benefits. A licensed healthcare practitioner must certify the condition and create a plan of care.

Critical illness provisions cover specific diagnoses regardless of life expectancy or functional status. Qualifying events often include heart attack, stroke, major organ transplant, kidney failure requiring dialysis, paralysis, and blindness. Some riders cover additional conditions like severe burns, coma, or loss of limbs.

Not all accelerated death benefit riders include chronic and critical illness triggers. Some policies limit access to terminal illness only, while others require purchasing a separate critical illness rider. Review your specific policy language or application carefully to understand which conditions qualify.

Author: Michael Stanton;

Source: everymuslim.net

How Much Money Can You Actually Receive?

The amount you can access through an accelerated death benefit rider depends on several factors: your policy's face value, the insurer's percentage limits, minimum and maximum payout thresholds, and the type of qualifying condition.

Most insurers allow you to access between 25% and 95% of your death benefit, with 50% to 75% being most common. Terminal illness claims typically permit higher percentages—often up to 95%—while chronic illness claims may cap at 50% or require monthly installments rather than lump sums.

Minimum payout amounts usually start at $5,000 to $10,000, preventing administrative costs from exceeding the benefit value. Maximum payouts often range from $250,000 to $500,000, though some policies impose no cap beyond the death benefit amount itself.

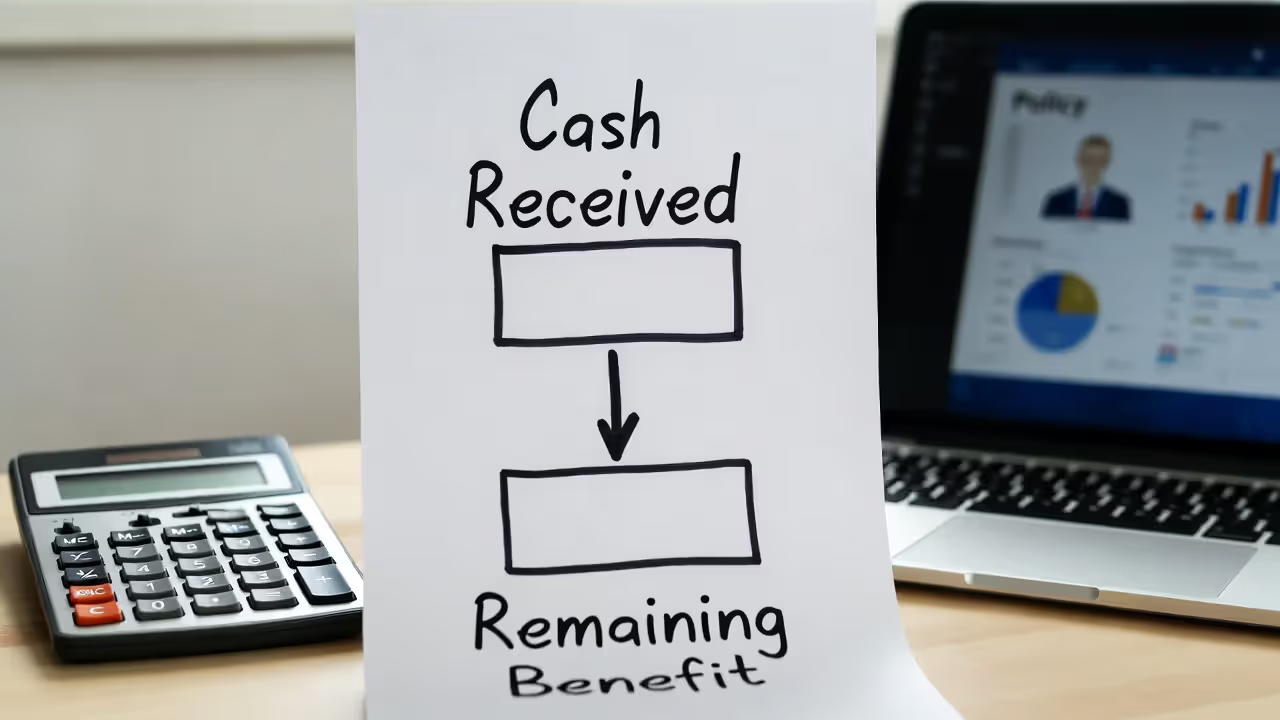

When you receive an accelerated payment, your remaining death benefit reduces by more than just the amount you receive. Insurers typically deduct the payout plus an administrative fee (often $250 to $500) and may charge interest or a discount rate to account for the time value of money. This discount reflects that the insurer is paying now rather than later, and it can range from 4% to 8% annually.

For example, if you have a $200,000 policy and request a $100,000 acceleration, you might receive $95,000 after a $500 administrative fee and a $4,500 discount. Your remaining death benefit would then be $100,000, not $105,000, because the full $100,000 face value was used.

Author: Michael Stanton;

Source: everymuslim.net

Tax treatment of accelerated death benefits generally favors policyholders. Under the Health Insurance Portability and Accountability Act (HIPAA), payments for terminal or chronic illness are typically tax-free if they meet specific requirements. Terminal illness payments are tax-free when life expectancy is 24 months or less. Chronic illness payments are tax-free up to $420 per day (2024 limit) when used for qualified long-term care expenses or paid under a per diem arrangement.

Critical illness payments may be taxable unless they meet chronic or terminal illness definitions. Consult a tax professional before filing claims, especially if your condition doesn't clearly fall into terminal or chronic categories.

Cost Breakdown: What You'll Pay for This Rider

One of the most attractive features of accelerated death benefit riders is that many insurers include them at no additional premium cost. This "free" rider has become an industry standard, particularly on policies issued in the last 15 years.

Author: Michael Stanton;

Source: everymuslim.net

When the rider is free, you pay nothing extra at policy purchase or during the life of the policy. Costs only arise when you activate the benefit. At that point, insurers typically charge an administrative processing fee ranging from $250 to $500, plus the present-value discount that reduces your payout.

Some insurers—particularly for chronic or critical illness provisions—do charge an additional premium. This cost varies based on your age, health class, policy type, and coverage amount. Expect to pay an extra $50 to $200 annually per $100,000 of coverage when a premium applies.

Comparing costs across major insurers reveals significant variation. State Farm, Northwestern Mutual, and New York Life typically include terminal illness acceleration at no charge. MassMutual and Guardian offer comprehensive living benefits packages that include chronic and critical illness triggers, sometimes with small additional premiums. Transamerica and Prudential often provide tiered options—basic terminal illness riders at no cost, with enhanced riders available for additional premium.

The real cost comes from the death benefit reduction. If you accelerate $100,000 from a $300,000 policy, your beneficiaries lose that $100,000 plus any growth it would have experienced in a permanent policy's cash value. This opportunity cost can be substantial, especially if you live longer than expected after receiving benefits.

Comparing Accelerated Death Benefits to Other Options

When facing a serious illness and needing funds, several alternatives to accelerated death benefits exist. Each option carries different trade-offs in speed, cost, tax treatment, and impact on your beneficiaries.

| Option | Access Speed | Costs/Fees | Tax Treatment | Impact on Beneficiaries | Best For |

| ADB Rider | 2-4 weeks after approval | $250-$500 admin fee; 4-8% discount | Tax-free for terminal/chronic illness | Death benefit reduced by amount taken plus fees | Terminal illness with short life expectancy |

| Viatical Settlement | 4-8 weeks | 20-40% commission to broker/buyer | Tax-free up to cost basis; gains may be taxable | Beneficiaries receive nothing | Need maximum cash now; no family dependents |

| Policy Loan | 1-2 weeks | 5-8% annual interest | Tax-free if policy remains in force | Death benefit reduced by loan balance plus interest | Temporary need; expect to repay |

| Long-Term Care Rider | 2-3 weeks after care begins | Higher premiums at purchase | Tax-free up to per diem limits | Reduces death benefit as benefits are paid | Chronic illness requiring extended care |

| Medical Expenses Direct Payment | Immediate to 30 days | Varies by program | Depends on source (charity, Medicaid, etc.) | No impact | Low income; qualify for assistance programs |

Viatical settlements involve selling your policy to a third party for a lump sum—typically 50% to 80% of the death benefit depending on life expectancy. While they provide more cash than accelerated benefits in some cases, the high commissions and complete loss of death benefit make them less attractive unless you have no dependents and need maximum funds immediately.

Policy loans offer flexibility because you can repay them if your situation improves. However, the accumulating interest can quickly erode your death benefit, and if the policy lapses due to unpaid loans, you may face a significant tax bill on gains.

Long-term care riders work well for chronic conditions requiring extended care services. They typically pay monthly benefits rather than lump sums, making them ideal for nursing home or home health care costs but less useful for one-time medical expenses.

Common Mistakes When Choosing or Using This Rider

Many policyholders make avoidable errors when selecting or activating accelerated death benefit riders. Understanding these pitfalls can save you and your beneficiaries significant money and frustration.

Assuming all policies automatically include the rider. While most modern policies include an accelerated death benefit rider, older policies—particularly those issued before 2000—often don't. Review your policy documents or contact your insurer to confirm the rider exists and understand what conditions qualify. Don't wait until you're diagnosed to discover you lack coverage.

Overlooking state-specific regulations. Some states mandate that insurers offer accelerated death benefit riders, while others leave it optional. State laws also govern minimum payout amounts, maximum fees, and disclosure requirements. California, for instance, requires insurers to provide detailed disclosures about how accelerations affect death benefits and cash values. New York limits the fees insurers can charge. Understanding your state's rules helps you evaluate whether your insurer is offering competitive terms.

Not understanding how payouts reduce death benefits. Many people assume that taking a $50,000 acceleration from a $200,000 policy leaves $150,000 for beneficiaries. In reality, administrative fees, discount rates, and lost cash value growth can reduce the remaining benefit to $140,000 or less. Ask your insurer for a specific illustration showing the exact remaining death benefit after your proposed acceleration.

Waiting too long to file claims. Some policyholders delay filing until their condition severely deteriorates, leaving less time to use the funds meaningfully. Once you receive a qualifying diagnosis, contact your insurer immediately to understand the process and timeline. Early filing also allows time to appeal if initially denied.

Ignoring the impact on government benefits. Receiving a large lump sum from an accelerated death benefit can temporarily disqualify you from means-tested programs like Medicaid or Supplemental Security Income. If you rely on these benefits, consult an elder law attorney or benefits specialist before filing a claim. Structured settlements or smaller periodic payments may preserve eligibility.

Failing to consider alternatives first. Accelerated death benefits make sense in many situations, but not all. If you have substantial savings, a policy loan might preserve more death benefit. If you qualify for pharmaceutical assistance programs or charity care, you might not need to tap life insurance at all. Exhaust other options before irreversibly reducing your beneficiaries' inheritance.

How to Add or Activate Your Accelerated Death Benefit

The process for obtaining accelerated death benefits differs depending on whether you're adding the rider to a new policy or activating an existing rider.

Author: Michael Stanton;

Source: everymuslim.net

Adding at policy purchase: When applying for new life insurance, your agent or the application will list available riders. The accelerated death benefit rider typically appears as a standard inclusion or an optional add-on with a checkbox. If it's not automatically included, specifically request it. The underwriting process doesn't change—you're not subject to additional health questions or exams for this rider. Review the policy illustration to confirm the rider appears and understand which qualifying conditions it covers.

Adding to an existing policy: Many insurers allow you to add an accelerated death benefit rider to policies that didn't originally include one. Contact your insurer or agent to request an amendment. Some companies add the rider without additional underwriting, while others may require a health questionnaire or even a medical exam if significant time has passed since policy issue. Expect a processing time of two to six weeks for the amendment to take effect.

Activating the rider—step-by-step:

- Contact your insurer: Call the customer service number on your policy or contact your agent. Request the accelerated death benefit claim forms and ask about specific documentation requirements.

- Complete the claim application: You'll fill out forms providing personal information, policy details, and the amount you're requesting. Specify whether you want a lump sum or periodic payments if your policy offers that option.

- Obtain physician certification: Your doctor must complete a certification form detailing your diagnosis, prognosis, and how you meet the rider's qualifying conditions. For chronic illness claims, the physician must also certify which ADLs you cannot perform and create a plan of care.

- Submit medical records: Most insurers require recent medical records supporting the diagnosis. Hospital discharge summaries, pathology reports, imaging studies, and specialist consultations strengthen your claim.

- Wait for review: Insurers typically review claims within 10 to 30 days. Terminal illness claims with clear documentation often process faster than chronic or critical illness claims. The insurer may request additional records or a second medical opinion.

- Receive approval and funds: Once approved, most insurers issue payment within five to seven business days. Funds arrive via check or direct deposit, depending on your preference.

- Sign acknowledgment forms: You'll sign documents acknowledging that you understand how the acceleration affects your death benefit and that you've been informed of tax implications and alternatives.

Typical approval timeline: From initial contact to receiving funds, expect four to six weeks for straightforward terminal illness claims. Chronic and critical illness claims may take six to eight weeks due to more complex qualification criteria. If your claim is denied, you have the right to appeal, which can add another 30 to 60 days.

Accelerated death benefit riders represent one of the most underutilized features in life insurance. We see clients who could have significantly eased their financial burden during treatment but didn't realize they had this option until it was too late. The key is understanding your policy's specific provisions before you need them and filing claims promptly once you qualify. Remember that taking benefits early isn't 'giving up'—it's using a tool you've paid for to maintain dignity and reduce stress during an already difficult time.

— Michael Chen, CFP®, ChFC, Principal, Horizon Financial Planning Group

Frequently Asked Questions About Accelerated Death Benefits

Accelerated death benefit riders provide valuable financial flexibility when you face a serious medical diagnosis. By allowing early access to life insurance proceeds, these riders can cover medical expenses, replace lost income, fund experimental treatments, or simply reduce financial stress during a difficult period.

The riders typically come at no additional cost for terminal illness provisions, with straightforward qualification criteria and tax-free benefits. Understanding the specific terms of your policy—including which conditions qualify, how much you can access, and how payouts affect your death benefit—empowers you to make informed decisions when circumstances require.

Before activating your rider, compare alternatives like policy loans or long-term care benefits to ensure you're choosing the best option for your situation. Consider the impact on beneficiaries, government benefits, and taxes. Most importantly, don't wait until you're severely ill to understand your coverage—review your policy now, ask questions, and ensure you have the documentation needed to file claims efficiently if the need arises.