The right policy type turns coverage into estate liquidity.

Estate Planning with Life Insurance Guide

Content

Life insurance serves a dual purpose most people overlook: it replaces income when you die and solves critical estate settlement problems your heirs will face within weeks of your death. While a will divides your property and a trust manages distributions, life insurance creates immediate cash—tax-free in most cases—to pay bills, taxes, and expenses without forcing your family to liquidate the beach house or sell shares of the business at a loss.

Estate planning with life insurance addresses three pain points simultaneously: it covers estate tax bills that come due nine months after death, replaces wealth transferred to charity or spent down in long-term care, and equalizes inheritances when one child gets the farm and another gets a check. The strategy works for estates worth $500,000 and estates worth $50 million, though the policy types and structures differ sharply.

Why Life Insurance Belongs in Your Estate Plan

Federal estate tax exemption sits at $13.61 million per person in 2024, but that figure sunsets in 2026 unless Congress acts. Even if your estate falls below federal thresholds, twelve states impose their own estate or inheritance taxes with exemptions as low as $1 million in Oregon and Massachusetts. Life insurance proceeds paid to a named beneficiary bypass probate entirely, arriving via check or wire transfer within two to four weeks—long before an executor can access bank accounts frozen pending court approval.

Immediate liquidity matters because estate expenses pile up fast. Funeral and burial costs average $8,000 to $12,000. If you own a business, someone must cover payroll and vendor invoices while ownership transfers. Real estate taxes, insurance premiums, and maintenance continue regardless of probate delays. Without cash on hand, your executor may need court permission to sell assets quickly, often at discounted prices, or take out loans against estate property at unfavorable rates.

Inheritance planning through life insurance also solves the "unequal asset" problem. Suppose your estate includes a $2 million vacation property and $2 million in retirement accounts, but you have three children. One child has managed the property for years and wants to keep it; the others expect equal inheritances. A $2 million policy lets you leave the property to one child and split the death benefit between the other two, avoiding forced sales or resentment.

Policies also replace wealth you donate during life or spend on care. If you gift $500,000 to a donor-advised fund or deplete savings paying for memory care, a life insurance policy can restore that amount to your heirs' inheritance—often for pennies on the dollar if you're healthy when you buy coverage.

Author: Christopher Baldwin;

Source: everymuslim.net

Types of Life Insurance Policies for Estate Planning

Not all life insurance works the same way in estate plans. Coverage duration, cash value accumulation, premium flexibility, and cost vary widely, and choosing the wrong type can leave your family with a lapsed policy or unnecessarily high costs.

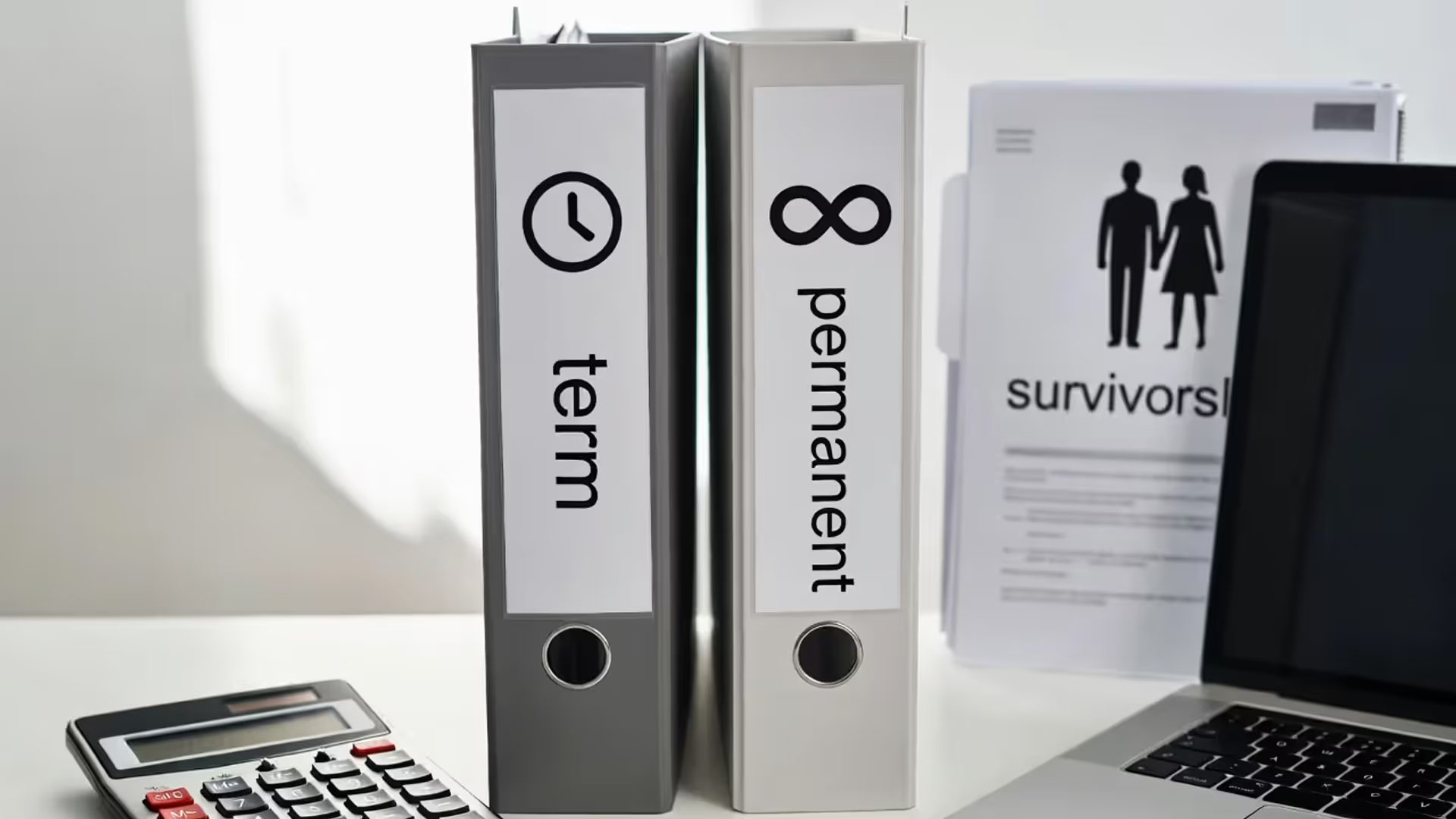

Term vs. Permanent Life Insurance: Which Fits Your Goals?

Term life insurance covers you for a set period—typically 10, 20, or 30 years—then expires. Premiums stay level during the term, and coverage amounts run from $100,000 into the tens of millions. A healthy 50-year-old might pay $150 per month for $1 million in 20-year term coverage. Term works well if your estate tax exposure is temporary—say, you own a business you plan to sell in 15 years, or your estate will drop below taxable thresholds once you spend down assets in retirement.

Permanent life insurance—whole life, universal life, and variants—covers you until death as long as premiums are paid. These policies build cash value you can borrow against or withdraw, and premiums typically run five to ten times higher than term for the same death benefit. A 50-year-old might pay $800 per month for $1 million in whole life coverage. Permanent insurance makes sense when estate tax liability is permanent, when you want to guarantee a specific inheritance amount regardless of how long you live, or when you need the cash value for premium financing or emergency liquidity.

Second-to-Die Policies for Married Couples

Survivorship life insurance (also called second-to-die) insures two people—usually spouses—and pays the death benefit only after both die. Because the policy doesn't pay until the second death, premiums cost 30% to 50% less than insuring each spouse separately. This structure aligns perfectly with estate tax planning: married couples can pass unlimited assets to each other tax-free through the unlimited marital deduction, so estate tax doesn't hit until the surviving spouse dies. A second-to-die policy funds that tax bill at the lowest possible premium cost.

One spouse's poor health doesn't necessarily disqualify the couple; underwriters average the risk. If one spouse has diabetes and the other is healthy, the joint policy may still get standard rates.

| Policy Type | Coverage Duration | Cash Value? | Estate Tax Planning Use | Typical Premium Range (per $1M coverage, age 50) |

| Term Life | 10–30 years, then expires | No | Temporary estate tax exposure; business transition periods | $100–$250/month |

| Whole Life | Lifetime (if premiums paid) | Yes, guaranteed growth | Permanent estate tax liability; guaranteed inheritance | $700–$1,200/month |

| Universal Life | Lifetime (flexible premiums) | Yes, variable growth | Flexible estate planning with changing premium budgets | $400–$900/month |

| Survivorship Life | Until second spouse dies | Optional | Married couples with estate tax due at second death | $300–$600/month (both insured) |

Using Life Insurance to Cover Estate Taxes and Immediate Expenses

Author: Christopher Baldwin;

Source: everymuslim.net

Liquidity planning separates functional estates from chaotic ones. The IRS requires estate tax payment within nine months of death—no installment plans unless the estate consists mostly of a closely held business and meets strict tests. State estate taxes often come due even sooner. If your estate holds $5 million in real estate, $3 million in a family LLC, and $1 million in retirement accounts, but faces a $1.2 million combined federal and state tax bill, your executor must find cash fast.

Selling assets under pressure rarely yields full value. A commercial property that might fetch $2 million with proper marketing could sell for $1.6 million in a forced 90-day sale. Liquidating a brokerage account in a down market locks in losses. Withdrawing from IRAs to pay estate taxes triggers income tax on top of estate tax, a double hit that can consume 60% to 70% of the withdrawal.

Life insurance solves this by delivering cash exactly when needed. A $1.5 million policy pays the tax bill and covers funeral costs, legal fees, and six months of property carrying costs while the executor marshals assets and files returns. The death benefit is income-tax-free to beneficiaries under IRC Section 101(a)(1), and if structured properly—more on this shortly—it's also excluded from your taxable estate.

Even estates below taxable thresholds benefit. Final medical bills, credit card debt, and mortgage balances don't disappear at death. If your spouse or children inherit a home with a $300,000 mortgage and lack income to cover payments, they face foreclosure or forced sale. A life insurance policy sized to pay off the mortgage preserves the asset and the family's housing stability.

Wealth Transfer Strategies with Life Insurance Trusts (ILITs)

Author: Christopher Baldwin;

Source: everymuslim.net

Here's the catch with life insurance: if you own the policy on your life, the IRS includes the death benefit in your gross estate under IRC Section 2042. Own a $3 million policy, and your taxable estate jumps by $3 million—potentially triggering hundreds of thousands in estate tax on a policy meant to pay estate tax. The solution is an irrevocable life insurance trust, or ILIT.

An ILIT is a trust you create and fund, which then owns the life insurance policy on your life. You name a trustee—often an adult child, trusted friend, or professional fiduciary—who holds legal title to the policy. Because you don't own the policy and can't change the trust terms (that's what "irrevocable" means), the IRS excludes the death benefit from your taxable estate. The trust document specifies how the trustee distributes the death benefit: outright to beneficiaries, in installments, or held in further trust for asset protection.

Setting up an ILIT requires precision. If you transfer an existing policy into the trust and die within three years, the IRS pulls the death benefit back into your estate under the three-year clawback rule in IRC Section 2035. The safer approach: create the ILIT first, then have the trustee apply for a new policy on your life as the owner and beneficiary from day one.

How an ILIT Protects Policy Proceeds from Estate Tax

When the ILIT owns the policy, the death benefit passes outside your estate. The trustee receives the insurance payout, then uses it according to the trust instructions—often loaning funds to your estate to pay taxes (with a promissory note) or buying illiquid assets from the estate at fair market value, injecting cash for the executor to pay bills. This keeps the life insurance money estate-tax-free while still making it available to solve estate liquidity problems.

ILITs also shield the death benefit from your beneficiaries' creditors and divorcing spouses. If you leave $2 million outright to your daughter and she's sued or divorces, that money is at risk. If the ILIT holds the $2 million and distributes it over time or keeps it in trust for her benefit, creditors generally can't reach it.

The trade-off: you lose control. You can't borrow against the policy's cash value, can't change beneficiaries, and can't dissolve the trust. You also must fund premium payments carefully. You can't pay premiums directly—that's an ownership red flag. Instead, you gift money to the trust each year (up to the annual gift tax exclusion, $18,000 per beneficiary in 2024), and the trustee pays the premium. Beneficiaries receive "Crummey notices" giving them a temporary right to withdraw the gift, which qualifies it for the annual exclusion; they typically don't withdraw, allowing the trustee to pay the premium.

Common Mistakes That Undermine Life Insurance in Estate Plans

Author: Christopher Baldwin;

Source: everymuslim.net

The most frequent error is naming your estate as beneficiary—or failing to name anyone, which defaults to your estate. Either way, the death benefit flows through probate, delaying payment for months and exposing it to creditors and administrative costs. Always name individual beneficiaries or a trust.

Outdated beneficiaries rank second. You bought the policy 20 years ago and named your ex-spouse, who's now remarried; or you named your children as minors, and insurance companies won't pay minors directly, forcing a court-supervised guardianship. Review beneficiary designations every three to five years and after major life events—marriage, divorce, births, deaths.

Ownership confusion creates tax problems. You own a policy on your spouse's life, they die, and you receive the death benefit tax-free—but now that cash is in your estate, increasing your future estate tax. Better structure: cross-owned policies (you own a policy on your spouse, they own one on you) or an ILIT owns both.

Insufficient coverage is harder to spot until it's too late. You bought a $1 million policy in 2010 when your estate was worth $3 million. Today it's worth $8 million, your state enacted a $2 million estate tax exemption, and your $1 million policy won't cover the $1.5 million tax bill. Inflation, asset appreciation, and law changes erode coverage; recalculate every five years.

Policy lapses destroy plans. Universal life policies with flexible premiums can lapse if cash value dwindles and you miss payments. Whole life policies can lapse if you borrow too much against cash value. Set up automatic premium payments from a checking account or, in an ILIT, calendar annual funding reminders.

Failing to coordinate with wills and trusts creates confusion. Your will leaves everything to your revocable living trust, but your life insurance names your children directly. Now your executor lacks cash (it went to the kids) while your trust holds illiquid assets and unpaid bills. Align beneficiary designations with your overall estate plan, or name the trust as beneficiary if you want the policy proceeds managed under trust terms.

Life insurance is the most cost-effective way to create instant liquidity in an estate—especially when illiquid assets like real estate or a family business make up the bulk of your wealth. I've seen families avoid fire-sale losses and keep businesses intact simply because a well-structured policy delivered cash within 30 days of death.

— Rebecca Thornton, Certified Financial Planner & Estate Planning Specialist

How to Calculate the Right Coverage for Inheritance Planning

Start with your estate tax liability. Add up everything you own—real estate, retirement accounts, business interests, investment accounts, personal property—and subtract debts. Apply the federal exemption ($13.61 million in 2024, but assume $7 million post-2026 if you're planning conservatively) and your state exemption if applicable. Multiply the excess by the estate tax rate: 40% federal, plus state rates ranging from 10% to 20%. That's your baseline tax bill.

Next, add immediate liquidity needs. Estimate $10,000 to $15,000 for funeral and burial, $20,000 to $50,000 for legal and accounting fees during estate administration, and six to twelve months of carrying costs for real estate and business expenses. If you have a mortgage or business debt your family should pay off, include that.

Now subtract liquid assets your executor can access quickly: checking and savings accounts, money market funds, publicly traded stocks and bonds (assuming no forced sale in a down market). The gap between your tax and expense total and your liquid assets is your insurance target.

Finally, factor in income replacement if you have dependents. If your spouse relies on your $150,000 salary and needs 20 years of support, that's a present-value calculation—roughly $2 million at a 4% discount rate—on top of estate settlement needs. Inheritance planning for minor children may require additional coverage to fund education, weddings, and home down payments.

Author: Christopher Baldwin;

Source: everymuslim.net

Example: Your estate is worth $10 million (federal exemption $7 million post-2026, state exemption $2 million). Federal tax on $3 million excess: $1.2 million. State tax on $8 million excess: $640,000 at 8%. Total tax: $1.84 million. Add $100,000 in settlement costs and $300,000 to pay off a business loan. Total need: $2.24 million. You have $500,000 in liquid accounts. Coverage target: $1.75 million, rounded to $2 million for cushion.

If premiums for $2 million exceed your budget, consider a blend: $1 million permanent policy for core estate tax liability plus $1 million in 20-year term to cover temporary business debt and income replacement while children finish college.

Frequently Asked Questions About Estate Planning with Life Insurance

Estate planning with life insurance transforms an abstract financial product into a concrete legacy tool. It turns a monthly premium into guaranteed liquidity when your family faces the worst financial timing of their lives—grief, probate delays, and looming tax deadlines. The right policy type and structure depend on your estate's size, composition, and your family's needs, but the core principle holds across all wealth levels: life insurance creates certainty in an uncertain process. Review your coverage now, coordinate it with your wills and trusts, and ensure ownership and beneficiaries align with your goals. The policy you set up correctly today becomes the cash your executor desperately needs tomorrow.